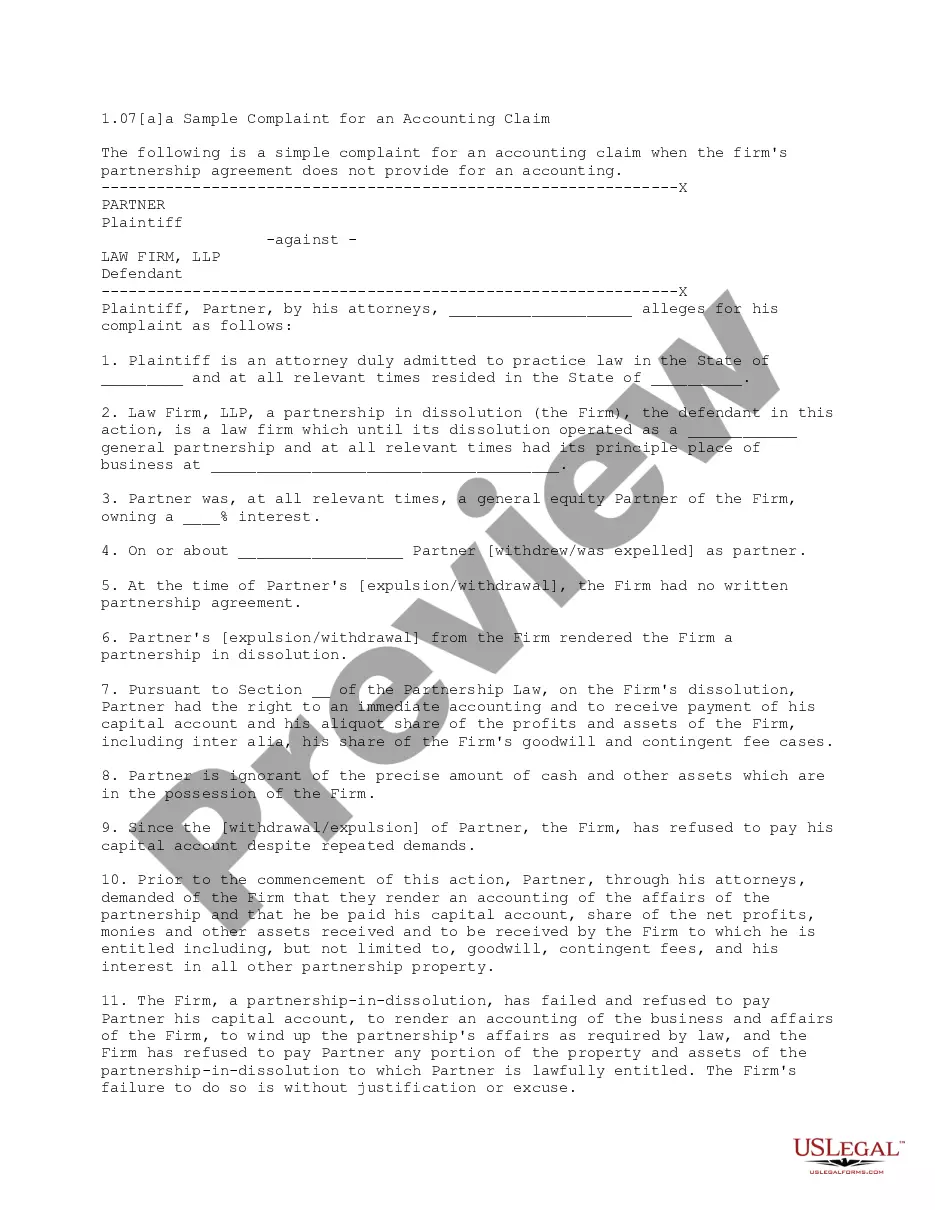

This complaint is for a plaintiff attorney who has been removed from the partnership of his former firm. The complaint requests an accounting of the former firm, stating that the plaintiff has been deprived of economic benefits rightfully due to him under the former partnership agreement, and also alleges egregious acts by his former partners.

Oklahoma Alternative Complaint for an Accounting which includes Egregious Acts

Category:

State:

Multi-State

Control #:

US-L0107A

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Alternative Complaint For An Accounting Which Includes Egregious Acts?

Choosing the best lawful papers design can be a struggle. Obviously, there are tons of templates accessible on the Internet, but how do you discover the lawful form you want? Use the US Legal Forms site. The services provides a large number of templates, for example the Oklahoma Alternative Complaint for an Accounting which includes Egregious Acts, that you can use for organization and private demands. Every one of the varieties are checked by specialists and meet up with federal and state specifications.

If you are previously signed up, log in in your accounts and click the Download option to find the Oklahoma Alternative Complaint for an Accounting which includes Egregious Acts. Make use of accounts to search with the lawful varieties you have purchased in the past. Proceed to the My Forms tab of your own accounts and acquire yet another backup from the papers you want.

If you are a whole new user of US Legal Forms, allow me to share simple directions for you to follow:

- Initially, make certain you have selected the correct form for your personal town/area. You may look through the form using the Preview option and look at the form outline to ensure this is the right one for you.

- If the form is not going to meet up with your needs, make use of the Seach discipline to discover the right form.

- Once you are certain that the form is suitable, click on the Get now option to find the form.

- Pick the prices program you want and enter the needed info. Build your accounts and buy an order making use of your PayPal accounts or credit card.

- Pick the file structure and acquire the lawful papers design in your system.

- Complete, revise and printing and indication the attained Oklahoma Alternative Complaint for an Accounting which includes Egregious Acts.

US Legal Forms is the biggest local library of lawful varieties in which you will find various papers templates. Use the service to acquire professionally-manufactured files that follow condition specifications.