This package contains essential forms to assist covered entities in complying with the requirements of the Fair and Accurate Credit Transactions Act, which is part of the federal Fair Credit Reporting Act. The forms included are designed to allow covered entities to meet their legal obligations and protect the rights of the parties involved.

Included in your package are the following forms:

1. How-To Guide for Fighting Fraud and Identity Theft With the FCRA sand FACTA Red Flags Rule

2. Guide to Complying with the Red Flags Rule under FCRA and FACTA

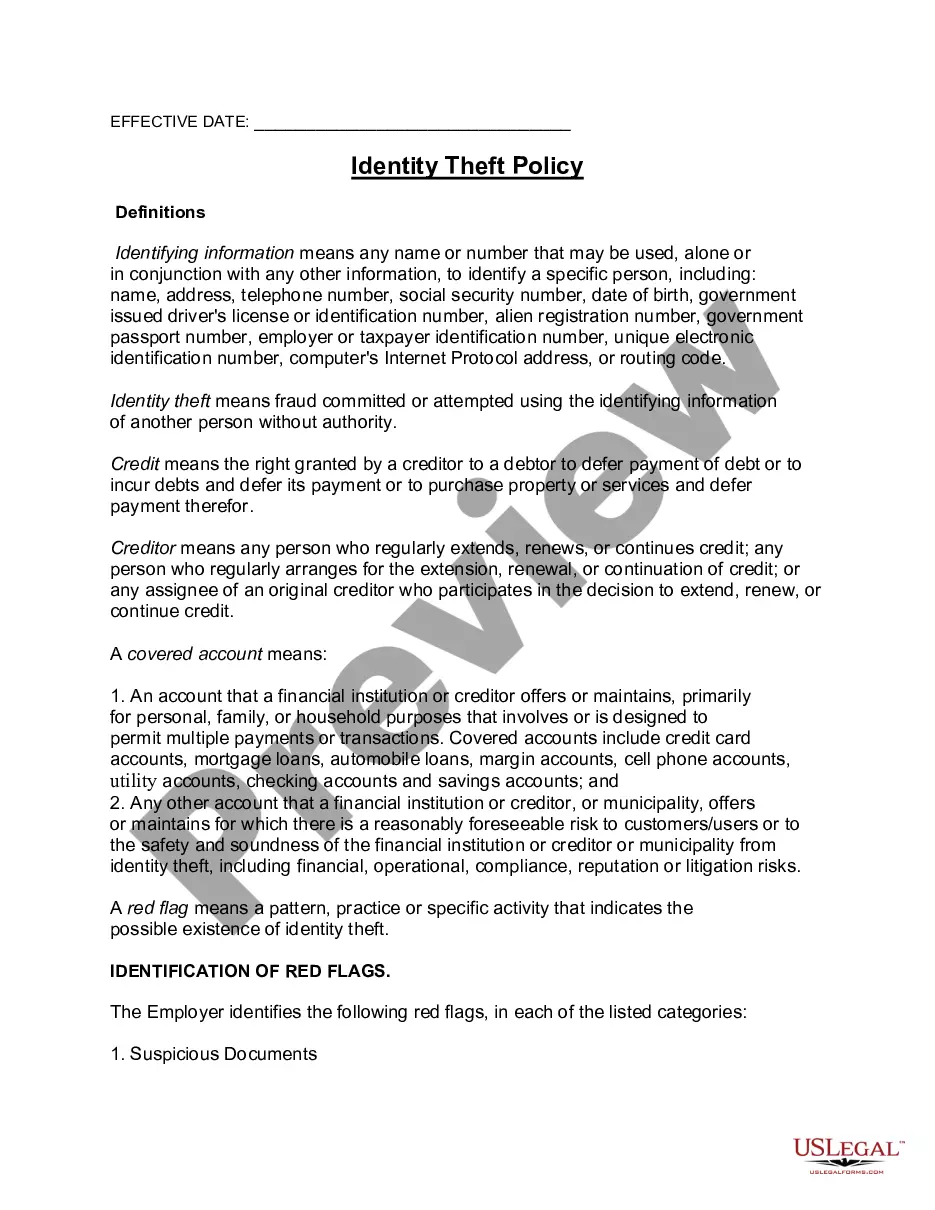

3. Sample Identity Theft Policy for FCRA and FACTA Compliance

4. Sample Pre-Adverse Action Letter Regarding Application for Employment

5. Sample Post-Adverse Action Letter Regarding Application for Employment

6. Notice To Users Of Consumer Reports - Obligations Of Users Under The FCRA

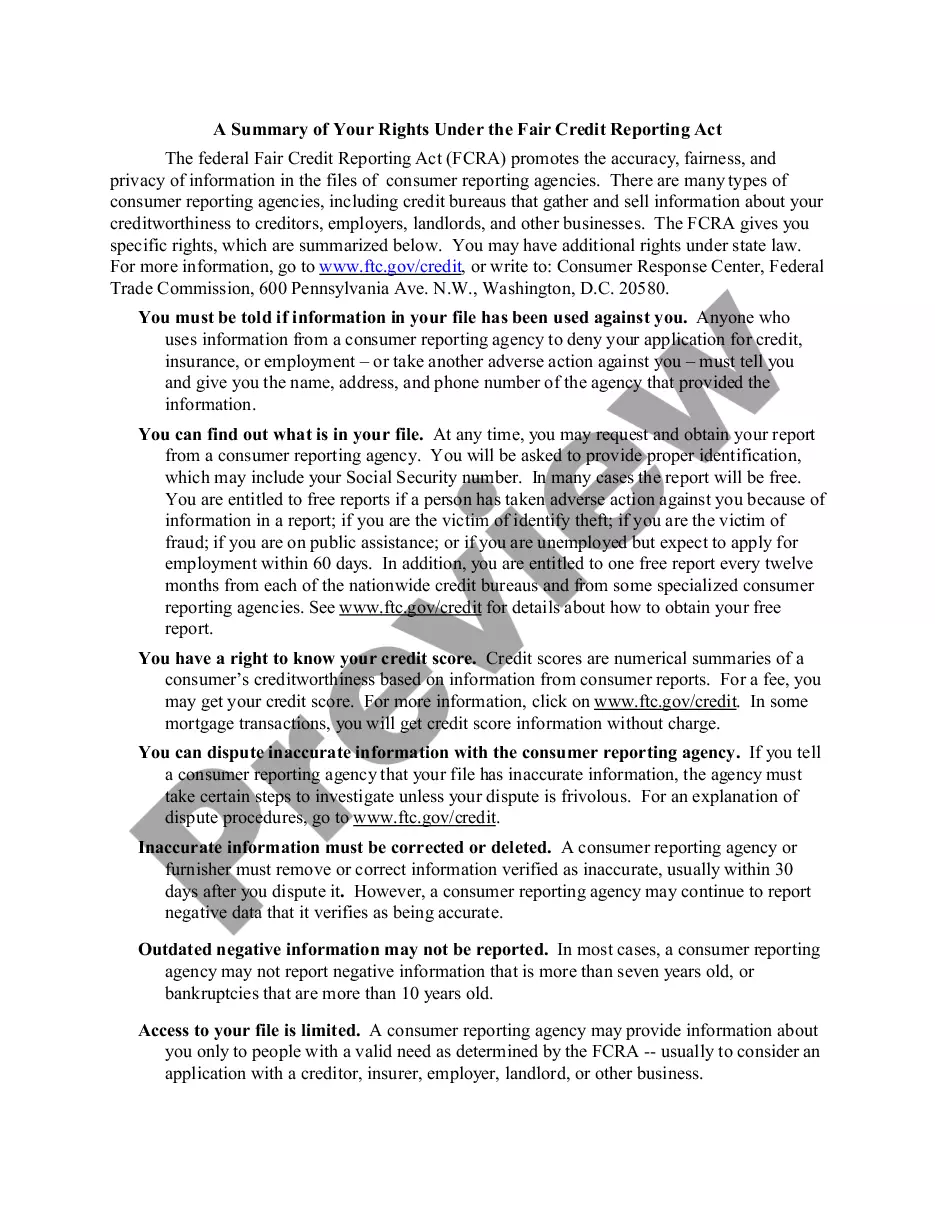

7. A Summary of Your Rights Under the Fair Credit Reporting Act

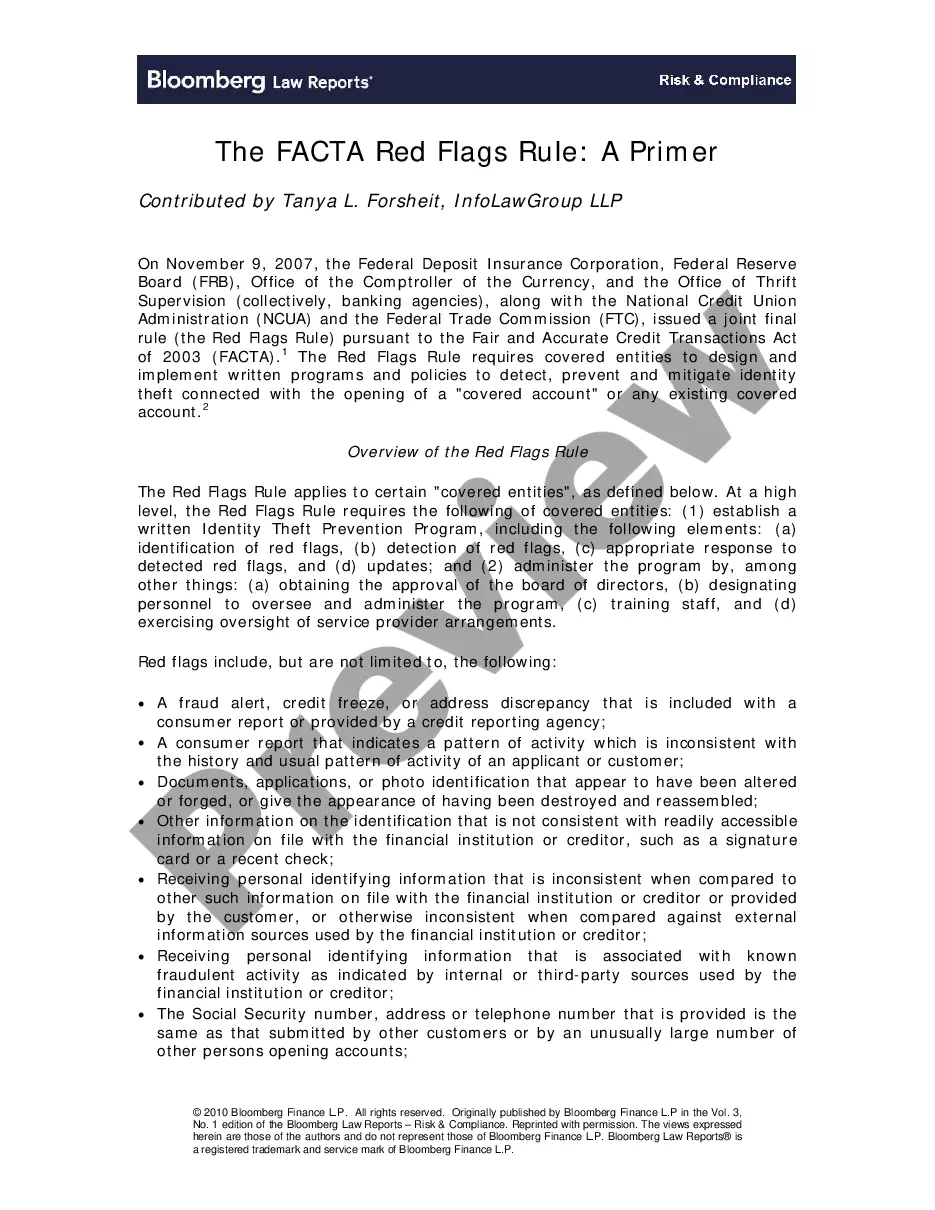

8. The FACTA Red Flags Rule: A Primer

9. Background Check Acknowledgment