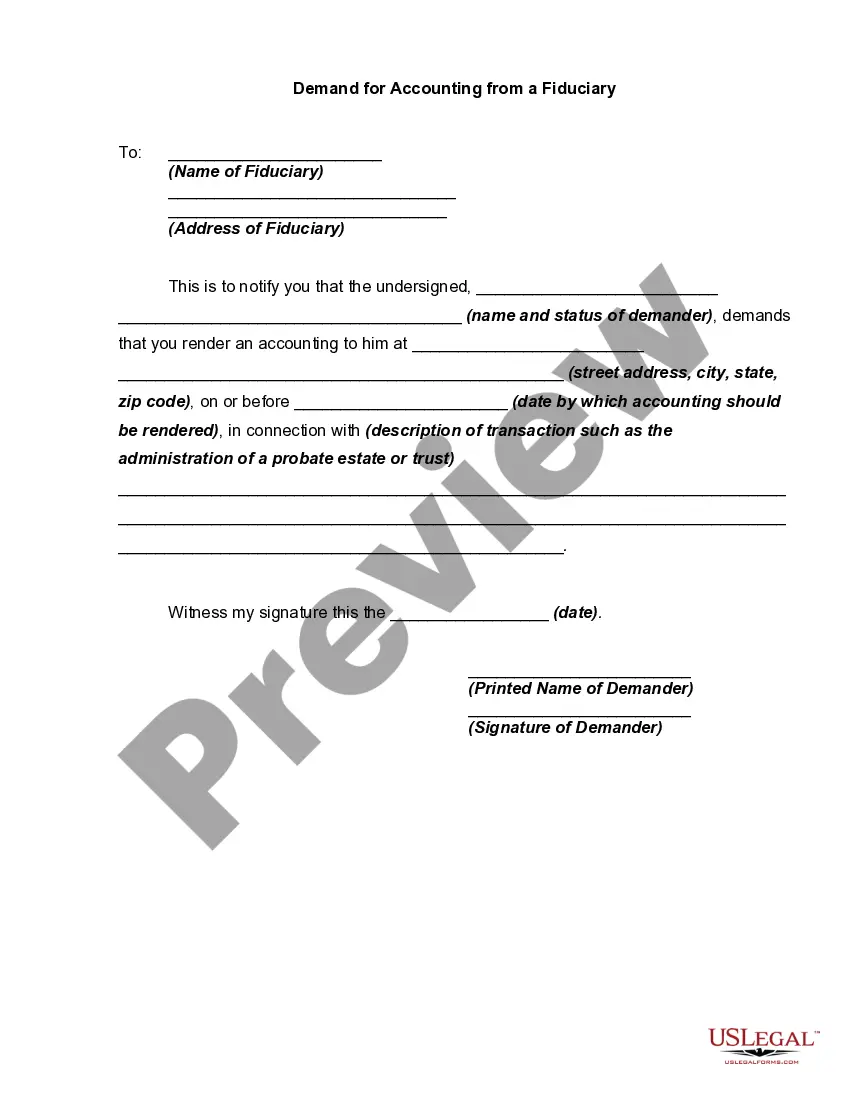

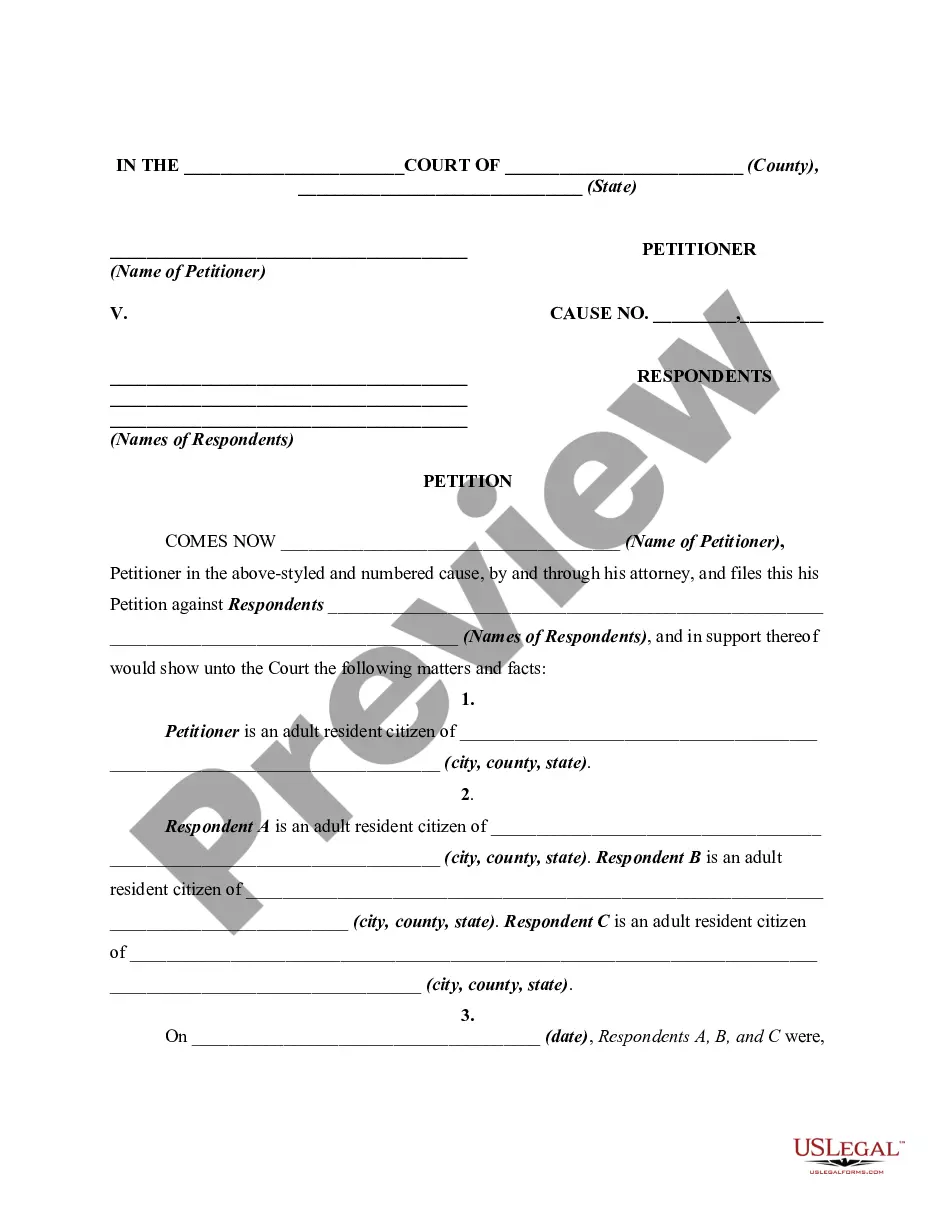

An accounting by a fiduciary usually involves an inventory of assets, debts, income, expenditures, and other items, which is submitted to a court. Such an accounting is used in various contexts, such as administration of a trust, estate, guardianship or conservatorship. Generally, a prior demand by an appropriate party for an accounting, and a refusal by the fiduciary to account, are conditions precedent to the bringing of an action for an accounting.

Oregon Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian

Instant download

Description

How to fill out Demand For Accounting From A Fiduciary Such As An Executor, Conservator, Trustee Or Legal Guardian?

You can spend hours online searching for the legal document template that meets the state and federal requirements you have.

US Legal Forms provides a vast array of legal forms that are vetted by professionals.

You can easily download or print the Oregon Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee, or Legal Guardian from their services.

If available, use the Review button to browse through the document template as well.

- If you already possess a US Legal Forms account, you can Log In and click the Obtain button.

- After that, you can complete, modify, print, or sign the Oregon Demand for Accounting from a Fiduciary including an Executor, Conservator, Trustee or Legal Guardian.

- Each legal document template you obtain is yours forever.

- To get another copy of any purchased form, go to the My documents tab and click the relevant button.

- If you are accessing the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure you have selected the correct document template for your county/city of choice.

- Check the form description to confirm you have chosen the appropriate document.

Form popularity

FAQ

A conservator is an individual appointed by the court to manage the personal affairs or finances of someone unable to do so themselves, often due to incapacity. This role comes with significant responsibility, as the conservator must act in the best interest of the individual. If you need assistance with concerns about a conservator's actions, leveraging the option of an Oregon Demand for Accounting from a Fiduciary can provide clarity.

Yes, an executor is generally required to show bank statements and other financial records as part of their duties. This transparency allows beneficiaries to understand the financial status of the estate being managed. If questions arise regarding the handling of funds, requesting an Oregon Demand for Accounting from a Fiduciary can be an appropriate step to ensure accountability.

Yes, a conservator is a type of fiduciary. While all conservators are fiduciaries, not all fiduciaries are conservators. A conservator specifically manages the affairs of someone who is unable to do so themselves, ensuring their needs are met. Understanding this relationship is crucial, especially when considering an Oregon Demand for Accounting from a Fiduciary.

Yes, a beneficiary can demand an accounting from a fiduciary. This legal right allows beneficiaries to review how their interests are being managed. When beneficiaries have concerns about mismanagement or lack of transparency, they can request detailed accounting records. An Oregon Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian facilitates this process.

The Oregon Fiduciary Powers Act provides guidelines for individuals acting as fiduciaries in the state. This act defines the powers and duties of fiduciaries, ensuring they fulfill their obligations responsibly. By implementing these regulations, the act aims to protect the interests of those whom fiduciaries serve. If you feel that your fiduciary is not meeting legal standards, consider initiating an Oregon Demand for Accounting from a Fiduciary.

A fiduciary is a person or entity that has the legal and ethical responsibility to act in the best interest of another party. This can include roles such as executors, conservators, trustees, or legal guardians. Fiduciaries are held to high standards of loyalty and care, as they manage assets and make important decisions. If you have concerns about your fiduciary’s actions, an Oregon Demand for Accounting from a Fiduciary can help clarify their responsibilities.

One significant disadvantage of a conservatorship is the potential for loss of autonomy. The conservator has control over financial decisions, which may lead to frustration for the individual. Additionally, establishing a conservatorship can be a lengthy and costly process, requiring court involvement and ongoing oversight. This can trigger an Oregon Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian to ensure transparency.

In Oregon, the threshold for an estate to be required to go through probate typically needs to exceed $275,000 in net value. If an estate falls below this threshold, it may qualify for simplified probate procedures or avoidance altogether. Determining the estate's value is important, and consulting with a professional for an Oregon Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian can be beneficial.

In Oregon, assets that generally go through probate include solely-owned real estate, bank accounts not designated for transfer on death, and personal property not managed by a trust. These assets require careful management, and it is advisable to seek guidance regarding an Oregon Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian to navigate the process effectively.

Exempt assets in Oregon include things like bank accounts with payable-on-death designations, certain joint assets, and typically, assets held in living trusts. These exempt assets allow for a smoother transfer of wealth without undergoing the probate process. Understanding what qualifies as exempt can help you efficiently manage your estate, potentially reducing the need for an Oregon Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian.