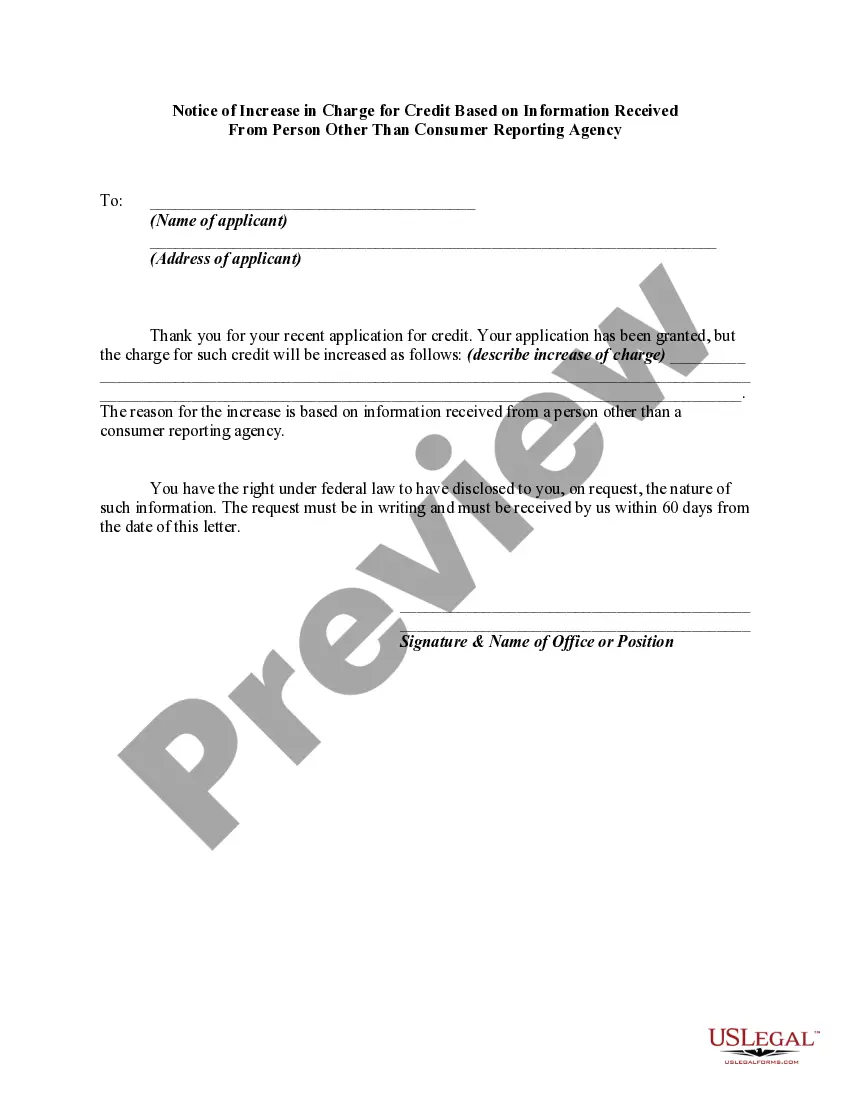

Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information. If such a request is made and is received within 60 days after the consumer learned of the adverse action, the user, within a reasonable period of time, must disclose to the consumer the nature of the information.

Keywords: Oregon, Notice of Increase in Charge, Credit, Information Received, Person Other Than Consumer Reporting Agency. Description: Oregon Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency is a legal document used by credit issuers in the state of Oregon to inform consumers about an upcoming increase in their credit charges. This notice is typically issued when a credit issuer obtains information about the consumer's creditworthiness from a source other than a consumer reporting agency. There are different types of Oregon Notice of Increase in charge of Credit, depending on the specific circumstances and the information received. These may include: 1. Employment-Based Increase: This type of notice is sent by credit issuers when they receive information about a change in the consumer's employment status, such as a promotion or a new job. If such information indicates an increase in the consumer's ability to handle additional debt, the credit issuer may decide to raise the charges on the consumer's credit. 2. Income-Based Increase: This notice is sent when credit issuers receive information indicating an increase in the consumer's income, such as a pay raise or a successful business venture. If the credit issuer believes that the consumer's enhanced income makes them more creditworthy, they may choose to raise the credit charges. 3. Asset-Based Increase: This type of notice is sent if credit issuers receive information about an increase in the consumer's assets, such as a significant inheritance or a substantial investment return. If the credit issuer determines that these newfound assets increase the consumer's ability to manage additional credit, they may decide to raise the charges. 4. Financial History-Based Increase: This notice is sent when credit issuers obtain information about a positive change in the consumer's financial history, such as the timely repayment of previous debts or an improved credit score. If the credit issuer believes that the consumer's improved financial behavior makes them a lower credit risk, they may decide to increase the credit charges. It is important for consumers to carefully review the Oregon Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency. This notice should clearly state the reasons behind the increase, the effective date of the change, and any additional terms and conditions associated with the credit account. Consumers have the right to dispute the increase if they believe the information provided or the decision made by the credit issuer is incorrect or unfair, as outlined by the relevant consumer protection laws in Oregon.Keywords: Oregon, Notice of Increase in Charge, Credit, Information Received, Person Other Than Consumer Reporting Agency. Description: Oregon Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency is a legal document used by credit issuers in the state of Oregon to inform consumers about an upcoming increase in their credit charges. This notice is typically issued when a credit issuer obtains information about the consumer's creditworthiness from a source other than a consumer reporting agency. There are different types of Oregon Notice of Increase in charge of Credit, depending on the specific circumstances and the information received. These may include: 1. Employment-Based Increase: This type of notice is sent by credit issuers when they receive information about a change in the consumer's employment status, such as a promotion or a new job. If such information indicates an increase in the consumer's ability to handle additional debt, the credit issuer may decide to raise the charges on the consumer's credit. 2. Income-Based Increase: This notice is sent when credit issuers receive information indicating an increase in the consumer's income, such as a pay raise or a successful business venture. If the credit issuer believes that the consumer's enhanced income makes them more creditworthy, they may choose to raise the credit charges. 3. Asset-Based Increase: This type of notice is sent if credit issuers receive information about an increase in the consumer's assets, such as a significant inheritance or a substantial investment return. If the credit issuer determines that these newfound assets increase the consumer's ability to manage additional credit, they may decide to raise the charges. 4. Financial History-Based Increase: This notice is sent when credit issuers obtain information about a positive change in the consumer's financial history, such as the timely repayment of previous debts or an improved credit score. If the credit issuer believes that the consumer's improved financial behavior makes them a lower credit risk, they may decide to increase the credit charges. It is important for consumers to carefully review the Oregon Notice of Increase in charge of Credit Based on Information Received From Person Other Than Consumer Reporting Agency. This notice should clearly state the reasons behind the increase, the effective date of the change, and any additional terms and conditions associated with the credit account. Consumers have the right to dispute the increase if they believe the information provided or the decision made by the credit issuer is incorrect or unfair, as outlined by the relevant consumer protection laws in Oregon.