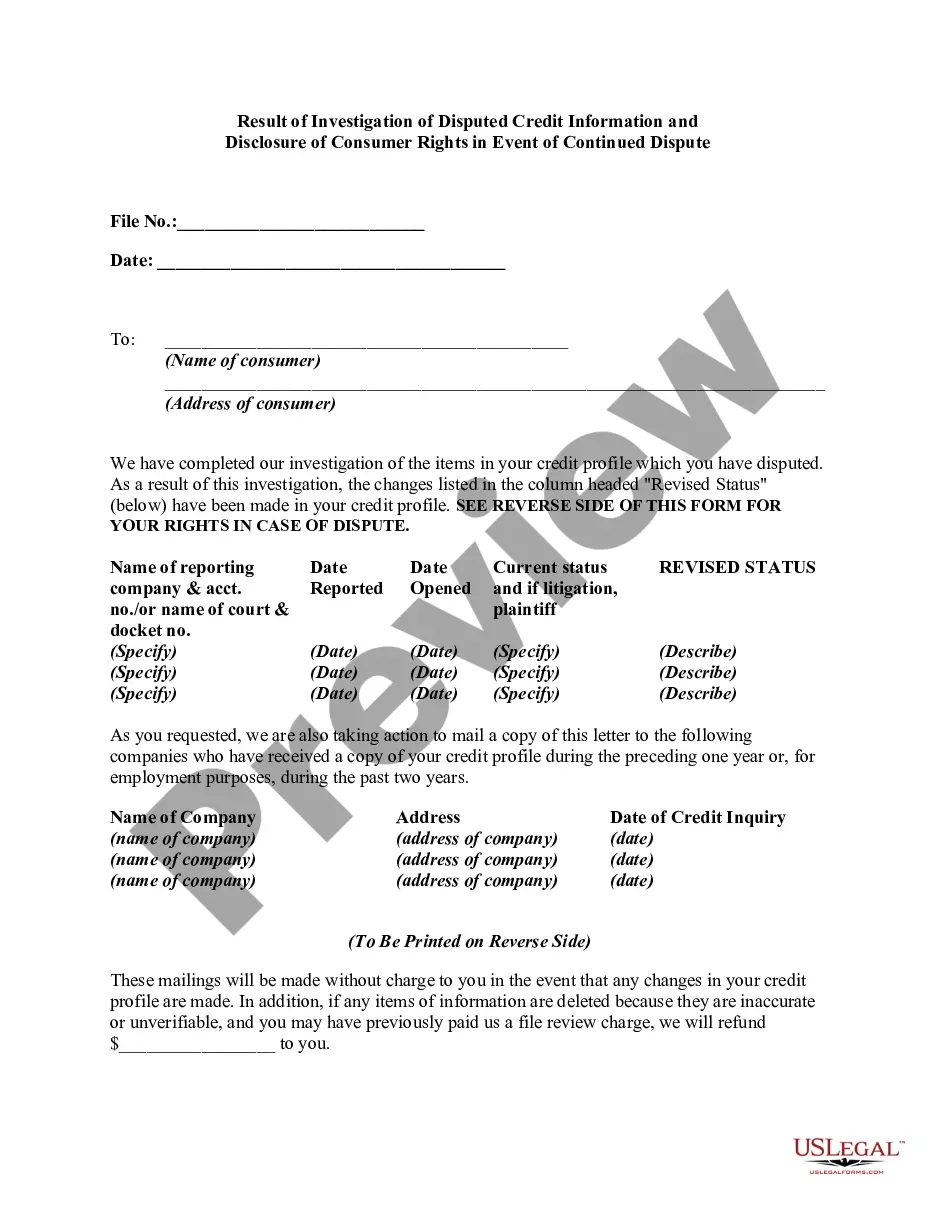

Under the Fair Credit Reporting Act, if a consumer disputes the completeness or accuracy of any item of information in the consumer's file, and the dispute is directly conveyed to the consumer reporting agency by the consumer, the reporting agency must, free of charge, conduct a reasonable reinvestigation to determine whether the disputed information is inaccurate, unless it has reasonable grounds to believe that the dispute is frivolous or irrelevant. If the information is erroneous, inaccurate, or can no longer be verified, the credit reporting agency must promptly correct or delete it and refrain from reporting the information in subsequent consumer reports.

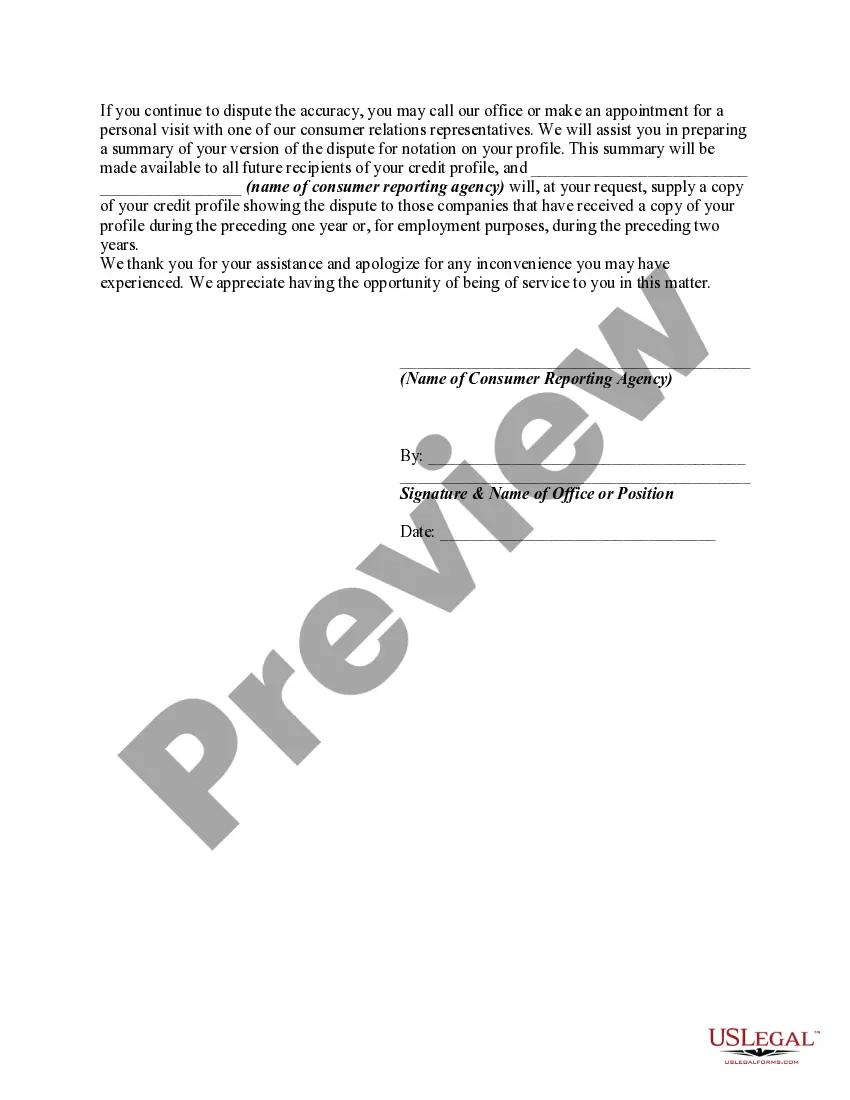

Following any deletion of information or notation as to disputed information, the agency, on request of the consumer, must furnish to certain persons either: (1) notification of the deletion; or (2) the consumer's statement of the dispute or the agency's summary of the statement. The consumer reporting agency must clearly and conspicuously disclose the consumer's rights to make such a request, such disclosure to be made at or prior to the time the information is deleted or the consumer's statement regarding the disputed information is received.

Title: Oregon Result of Investigation of Disputed Credit Information and Disclosure of Consumer Rights in Event of Continued Dispute Introduction: In Oregon, when consumers discover disputed credit information on their credit reports, it is crucial to understand the result of the investigation process and the disclosure of consumer rights if the dispute persists. This article will provide a detailed description of the steps involved in investigating disputed credit information, along with the consumer rights protections provided by the state of Oregon. 1. Investigation of Disputed Credit Information: When a consumer in Oregon initiates a dispute regarding inaccurate or incomplete credit information, different parties play a role in investigating and resolving the issue. These parties include: a. Credit Reporting Agencies (Crash): Crash are responsible for conducting a thorough investigation into the disputed credit information. They will review the consumer's complaint, communicate with relevant data furnishes, and make a determination based on the evidence presented. b. Data Furnishes: Data furnishes, such as banks or lenders, are obligated to provide accurate and verifiable information on the consumer's credit history. In the event of a dispute, they must work with the Crash to investigate the claim and provide supporting evidence. c. Consumer's Role: Consumers have a vital role in the investigation process. They must provide the Crash with detailed documentation supporting their dispute, such as receipts, statements, or other relevant evidence. 2. Result of Investigation: After conducting a thorough investigation, the Crash will deliver the result to the consumer. The possible outcomes of the investigation may include: a. Verified Information: If the investigation determines that the disputed credit information is accurate, it will remain on the consumer's credit report. The consumer will receive a notification explaining the reasons for the validation. b. Inaccurate Information: In cases where the investigation proves the disputed credit information to be incorrect or incomplete, the Crash are required to update or delete the disputed item from the consumer's credit report. The consumer should receive written notification of these changes. c. Continued Dispute: If the consumer remains unsatisfied with the investigation outcome, they have the right to continue disputing the credit information. Steps to exercise this right are outlined below. 3. Consumer Rights in Event of Continued Dispute: In Oregon, consumers enjoy certain rights to address the dispute if they are not satisfied with the investigation outcome. These rights include: a. Written Explanation: The Crash must provide the consumer with a written explanation of the investigation result, including the evidence relied upon and the reasons for the decision. This explanation enables the consumer to identify any potential errors or omissions. b. Reinvestigation Request: If the consumer believes the investigation was not adequately conducted or the decision was erroneous, they can request a reinvestigation. The Crash must perform a second investigation ensuring all relevant information is considered. c. Dispute Statement: If the results of the reinvestigation are not in the consumer's favor, they have the right to add a statement to their credit report explaining their dispute. This statement allows future lenders or creditors to consider the consumer's side of the story. Conclusion: Understanding the result of an investigation into disputed credit information and disclosure of consumer rights is essential for Oregon residents. By comprehending the investigation process and their rights in the event of continued dispute, consumers can protect and maintain accurate credit histories, essential for their financial well-being.