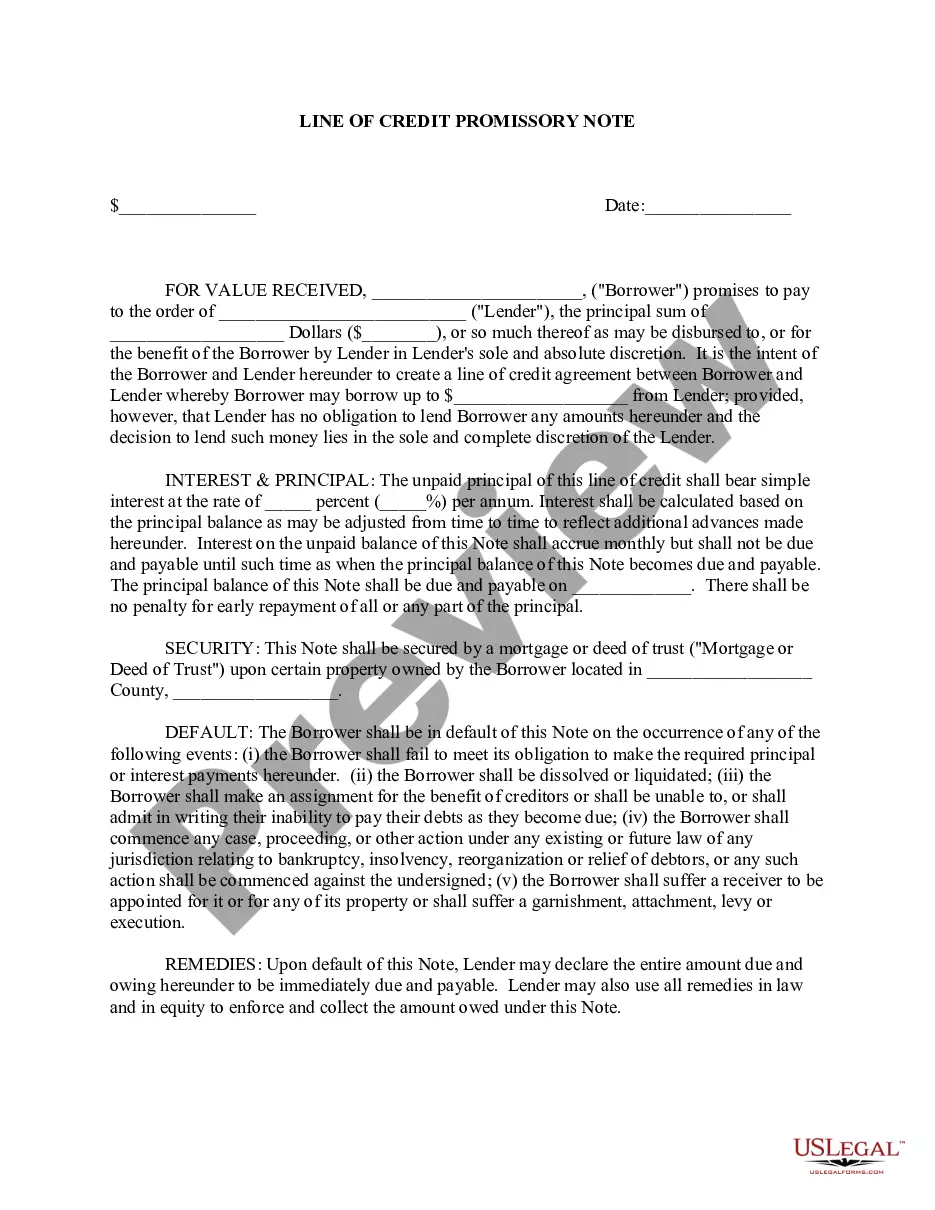

A Line of Credit Promissory Note is a legally binding document that outlines the terms and conditions of borrowing money through a line of credit in the state of Oregon. It is an agreement between the lender and the borrower that serves as evidence of the debt and specifies the repayment terms. In Oregon, there are several types of Line of Credit Promissory Notes, each tailored to different purposes and circumstances. Some common types of these notes include: 1. Personal Line of Credit Promissory Note: This type of promissory note is used when an individual borrows money for personal use, such as consolidating debts or covering unexpected expenses. 2. Business Line of Credit Promissory Note: In the realm of business, companies often utilize a line of credit to manage cash flow fluctuations or finance short-term operating expenses. This type of promissory note is designed specifically for businesses operating in Oregon. 3. Secured Line of Credit Promissory Note: This note is used when the borrower pledges collateral (such as real estate, inventory, or equipment) to secure the line of credit. This provides reassurance to the lender and often results in more favorable terms for the borrower, such as a lower interest rate. 4. Unsecured Line of Credit Promissory Note: Unlike the secured note, an unsecured promissory note does not involve any collateral. This makes it riskier for the lender, therefore often resulting in higher interest rates for the borrower. The Oregon Line of Credit Promissory Note typically includes essential details such as the names and contact information of both the lender and borrower, the principal amount borrowed, interest rate or method of calculation, repayment terms, late payment penalties, and any applicable fees. This document serves as a legal protection for both parties involved and ensures transparency in the borrowing process. It is important for borrowers in Oregon to carefully review and understand the terms outlined in the Line of Credit Promissory Note before signing it. Seeking legal advice or consulting with a financial professional may be advisable to ensure compliance with state laws and to make informed borrowing decisions.

Oregon Line of Credit Promissory Note

Description

How to fill out Oregon Line Of Credit Promissory Note?

Have you been in a placement in which you need to have papers for possibly company or person functions nearly every time? There are a lot of legal record templates available online, but getting kinds you can rely on is not straightforward. US Legal Forms provides a huge number of type templates, just like the Oregon Line of Credit Promissory Note, which are written to fulfill federal and state needs.

In case you are currently acquainted with US Legal Forms internet site and possess an account, just log in. Next, you are able to acquire the Oregon Line of Credit Promissory Note format.

Should you not come with an account and need to begin using US Legal Forms, follow these steps:

- Get the type you want and ensure it is for that correct town/county.

- Utilize the Preview key to review the shape.

- Browse the outline to actually have selected the right type.

- If the type is not what you are looking for, utilize the Search area to discover the type that suits you and needs.

- Whenever you discover the correct type, click on Get now.

- Select the pricing program you desire, fill in the specified info to produce your bank account, and buy your order utilizing your PayPal or Visa or Mastercard.

- Pick a practical document file format and acquire your duplicate.

Find all of the record templates you might have purchased in the My Forms food selection. You may get a further duplicate of Oregon Line of Credit Promissory Note at any time, if required. Just click on the required type to acquire or print the record format.

Use US Legal Forms, probably the most substantial variety of legal forms, in order to save time and stay away from mistakes. The service provides expertly created legal record templates which you can use for a range of functions. Create an account on US Legal Forms and begin creating your life easier.