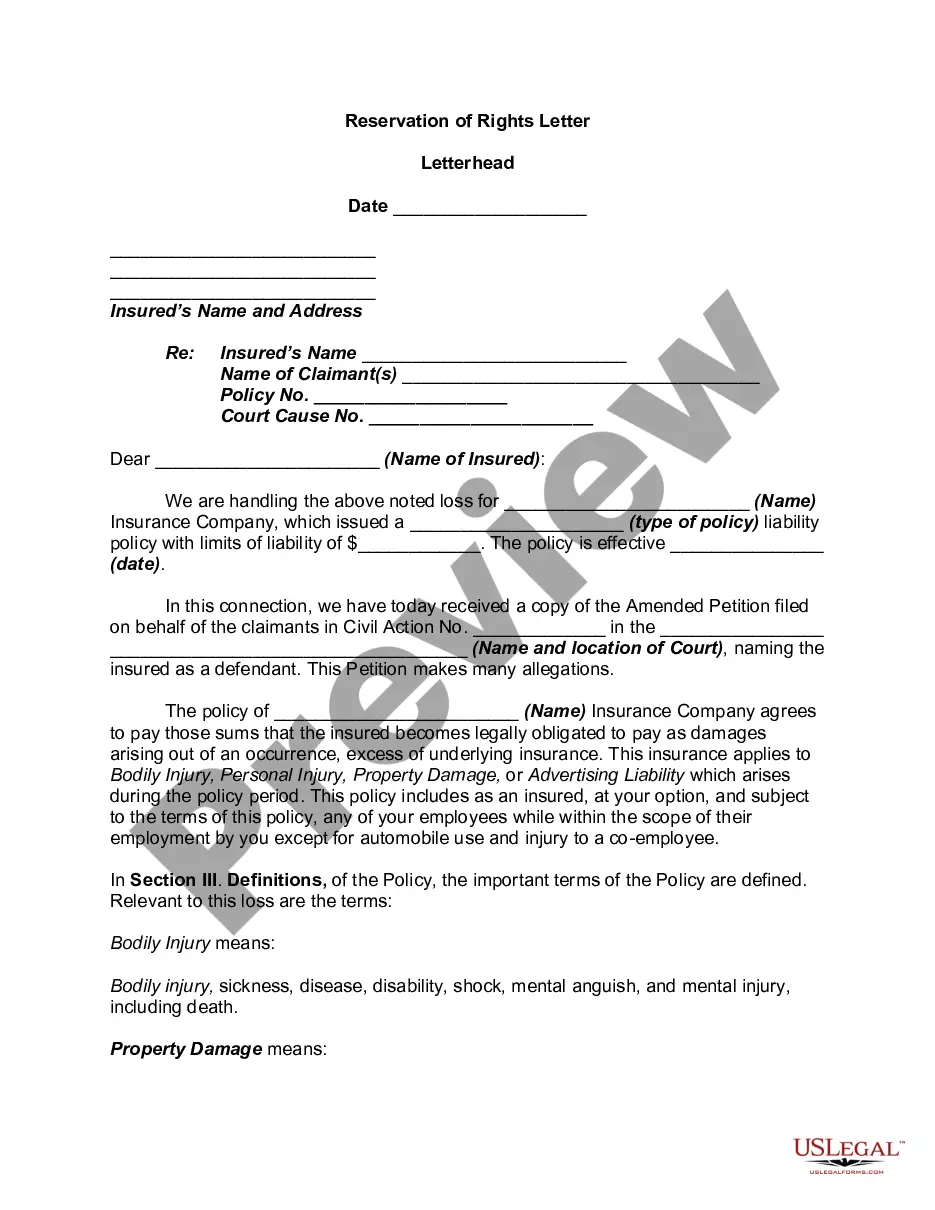

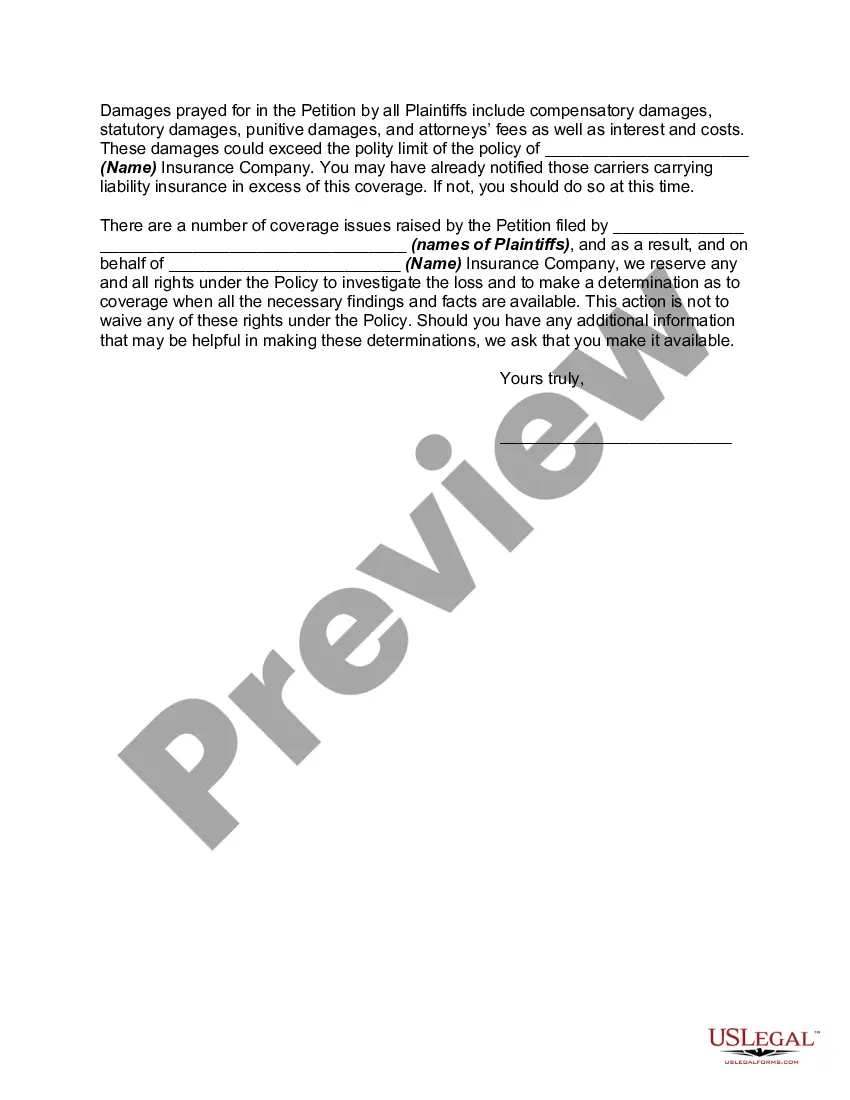

A reservation of rights defense is a means by which a liability insurance carrier agrees to protect and defend its insured against a claim or suit while reserving the right to further evaluate and perhaps even deny coverage for some or all of the claim. It is most commonly used when the claim or suit contains both covered and non-covered allegations, when the allegations are in excess of policy limits, or when the insurer is still investigating its defense and coverage obligations. For the insurer, a reservation of rights provides the flexibility to satisfy its duty to defend without committing to coverage. For the business owner who ultimately may have to pay for an adverse judgment, it requires careful monitoring and attention.

A reservation of rights letter is an essential tool used by insurance companies to notify policyholders of their intent to investigate and evaluate a claim, while simultaneously reserving their right to deny coverage if the claim falls outside the policy's terms and conditions. In Oregon, the reservation of rights letter serves a vital purpose in protecting both the insurer's interests and the insured party's rights. When an insurance company receives a claim, particularly one that may be subject to exclusions or limitations in the policy, it may issue an Oregon reservation of rights letter to the policyholder. This letter explicitly states that the insurer is reserving their right to deny coverage if the investigation determines that the claimed loss is not within the policy's coverage scope. The Oregon reservation of rights letter typically includes several crucial elements. It begins by identifying the insurance company and policyholder, stating the policy number, and providing the date of the letter. The letter then proceeds to summarize the nature of the claim and mentions the potential policy exclusions or coverage limitations that may apply. It is crucial to emphasize that receiving such a letter does not necessarily mean coverage will be denied, but it acts as a notice that an investigation is needed to determine the extent of coverage. The letter highlights any concerns or issues regarding the claim that need further investigation or clarification. It may include requests for additional documentation, statements, or evidence related to the claim to aid in the assessment process. This allows the insurance company to gather the necessary facts to evaluate coverage and potential liability. Oregon also recognizes variations of the reservation of rights letter. One common type is the "partial reservation of rights letter." This version is used when only specific aspects or elements of the claim may be subject to potential exclusions or coverage limitations. It serves as a more detailed notice, enabling the policyholder to better understand the specific areas of concern. Another variation is the "superseding reservation of rights letter." This type of letter is issued when the insurer initially issues a standard reservation of rights letter but later discovers new or previously unknown facts that could impact the investigation and coverage determination. The updated letter amends or supersedes the initial notice to reflect the additional information. In conclusion, an Oregon reservation of rights letter is a crucial communication tool used by insurance companies to safeguard their interests during claim investigations while notifying policyholders of any potential exclusions or limitations. By providing transparency and clarity, these letters enable both parties to ensure a fair and thorough claims process.