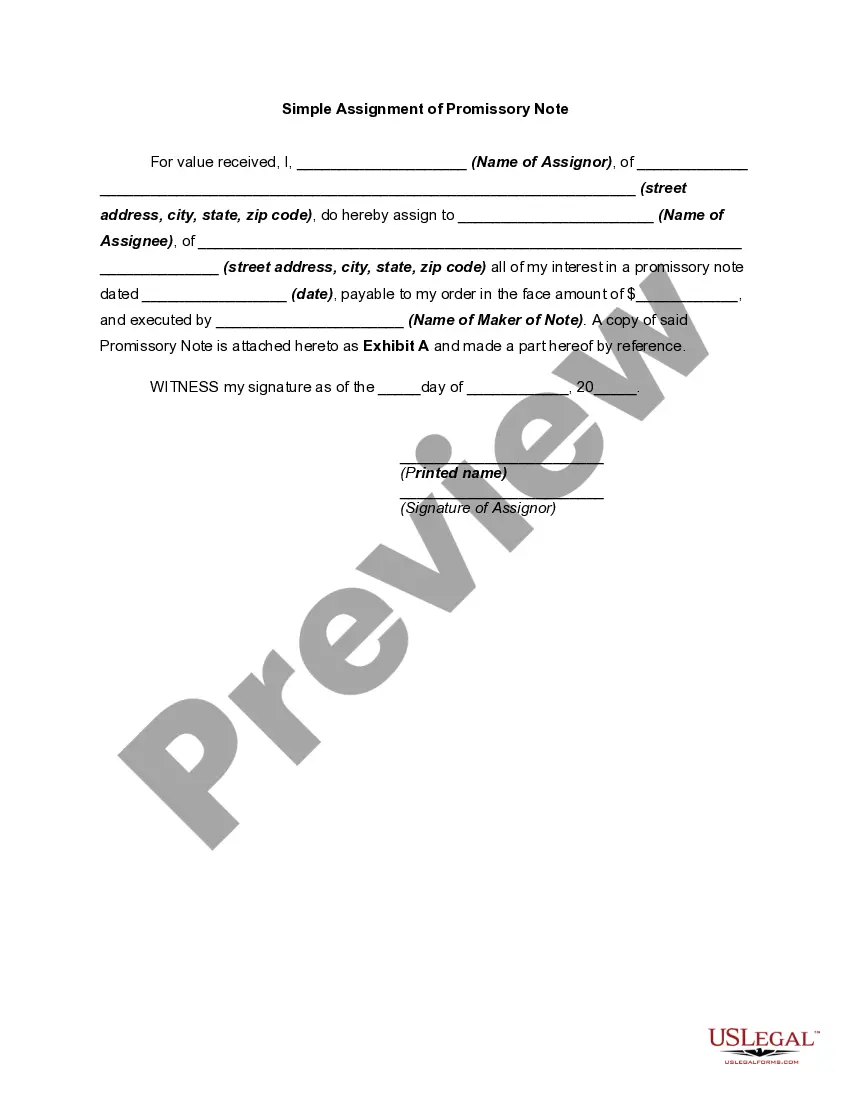

The Oregon Simple Promissory Note for Family Loan is a legally binding document that outlines the terms and conditions of a loan agreement between family members in the state of Oregon. This type of promissory note serves as evidence of a loan transaction and ensures that both parties are aware of their obligations and responsibilities. Keywords: Oregon, Simple Promissory Note, Family Loan, loan agreement, legal document, terms and conditions, loan transaction, obligations, responsibilities. There are several types of Oregon Simple Promissory Notes for Family Loans, each addressing different aspects and scenarios. Here are the main types: 1. Oregon Simple Promissory Note for Lump Sum Payment: This type of promissory note is used when a family member lends a fixed amount of money to another family member and requires repayment in a lump sum within a specified period. 2. Oregon Simple Promissory Note for Installment Payments: In cases where a family loan is to be repaid in fixed installments over a specific period, this type of promissory note is used. It outlines the amount of each installment and the repayment schedule. 3. Oregon Simple Promissory Note with Interest: When a family member lends money to another family member and expects interest on the loan, this type of promissory note is used. It specifies the interest rate, repayment schedule, and the total amount to be repaid, including interest. 4. Oregon Simple Promissory Note with Collateral: In situations where the lender requires collateral for the loan, such as a property or valuable asset, this type of promissory note is used. It details the collateral, repayment terms, and consequences in case of default. 5. Oregon Simple Promissory Note with Co-signer: When a family loan involves a co-signer, who assumes equal responsibility for loan repayment, this type of promissory note is used. It clarifies the obligations and responsibilities of both the borrower and the co-signer. It is important to consult with an attorney or use a reliable online legal service to draft a promissory note that adheres to Oregon laws and meets the specific needs of the family loan transaction.

Oregon Simple Promissory Note for Family Loan

Description

How to fill out Oregon Simple Promissory Note For Family Loan?

Are you presently in the place in which you require files for sometimes organization or person purposes nearly every working day? There are tons of legal papers themes available online, but locating types you can trust isn`t effortless. US Legal Forms offers a large number of type themes, such as the Oregon Simple Promissory Note for Family Loan, that happen to be created to meet state and federal demands.

In case you are previously informed about US Legal Forms web site and also have a free account, basically log in. Afterward, you may obtain the Oregon Simple Promissory Note for Family Loan web template.

If you do not provide an profile and need to start using US Legal Forms, abide by these steps:

- Get the type you will need and make sure it is to the right metropolis/county.

- Utilize the Preview button to check the form.

- Look at the outline to ensure that you have chosen the right type.

- In the event the type isn`t what you`re looking for, make use of the Research industry to discover the type that fits your needs and demands.

- If you find the right type, click on Purchase now.

- Opt for the rates prepare you would like, fill in the required information and facts to make your money, and pay for an order making use of your PayPal or credit card.

- Decide on a hassle-free data file formatting and obtain your backup.

Find all of the papers themes you possess purchased in the My Forms menu. You can aquire a additional backup of Oregon Simple Promissory Note for Family Loan anytime, if possible. Just click the required type to obtain or printing the papers web template.

Use US Legal Forms, the most extensive assortment of legal varieties, to save lots of time and prevent faults. The assistance offers appropriately made legal papers themes which you can use for a variety of purposes. Produce a free account on US Legal Forms and start creating your way of life a little easier.