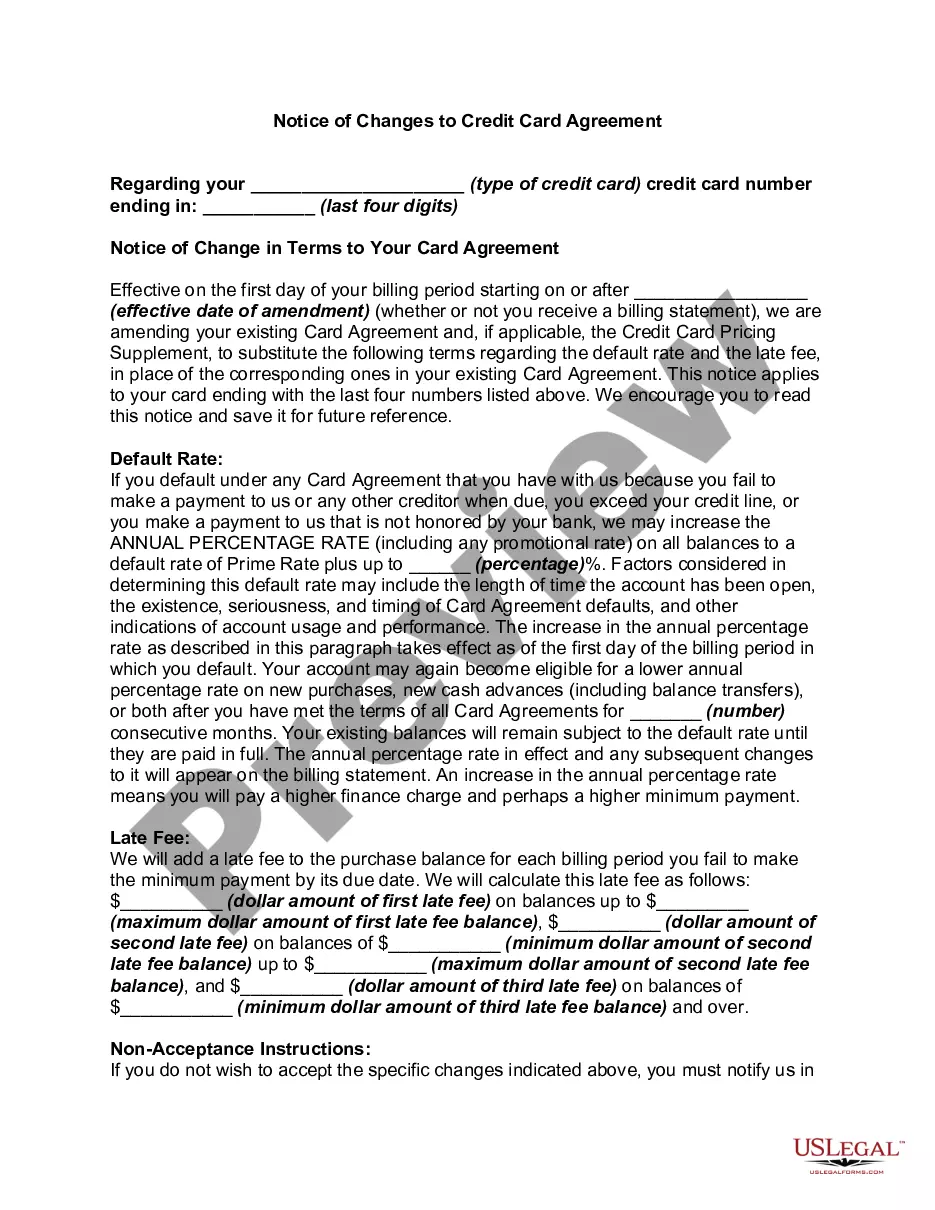

Title: Understanding the Oregon Notice of Changes to Credit Card Agreement Keywords: Oregon, Notice of Changes, Credit Card Agreement, types, details, consumer rights, legal obligations, interest rates, fees, penalties, terms, conditions, contract, disclosure Introduction: The Oregon Notice of Changes to Credit Card Agreement is a crucial document that outlines modifications made to an existing credit card agreement. It serves to inform consumers in Oregon about any amendments made to ensure transparency, fairness, and adherence to state and federal regulations. Keep reading to understand the various types of Oregon Notice of Changes to Credit Card Agreement and the key information contained within them. Types of Oregon Notice of Changes to Credit Card Agreement: 1. Interest Rate Modifications: This type of notice informs cardholders about alterations made to their credit card's interest rates. It could include changes to the annual percentage rate (APR) for purchases, balance transfers, cash advances, and penalty APR's for late payments. The notice will specify the new rates and the effective date of the change. 2. Fee Adjustments: This notice highlights revisions in various fees associated with the credit card, such as annual fees, late payment fees, over-limit fees, or foreign transaction fees. It ensures cardholders are aware of any changes in fee structures and their impact on account management and overall costs. 3. Penalty Changes: In cases where a cardholder violates specific terms and conditions, penalty charges may be imposed. This notice details any modifications made to existing penalty fees, such as increased late payment charges or penalties for returned payments. 4. Terms and Conditions Alterations: This type of notice covers broader modifications to the credit card agreement, encompassing changes to terms, conditions, and contractual obligations between the card issuer and the cardholder. It may include changes in payment due dates, grace periods, or dispute resolution processes. Key Details and Information: a) Effective Date: The notice specifies the date on which the changes to the credit card agreement will become effective. This allows cardholders to adjust their financial planning accordingly. b) Method of Communication: Credit card issuers are required to inform cardholders of any changes in the agreement through a written notice. The notification might be delivered via postal mail, email, or electronic statements, depending on the agreed communication methods. c) Consumer Rights: The notice will often provide essential information about a cardholder's rights in response to the changes made. It may provide guidance on how to reject the changes, close the account, or seek clarification regarding the new terms. d) Disclosure of Changes: The notice is expected to provide a clear and concise explanation of the changes to the credit card agreement. This includes disclosing whether the modification favors the cardholder or the issuer and explaining the reasons behind the adjustments. Conclusion: Understanding the Oregon Notice of Changes to Credit Card Agreement is vital for all credit cardholders in Oregon. By being aware of the types of changes, key details, and their consumer rights, individuals can make informed decisions regarding their credit card use. It is crucial to review such notices thoroughly to ensure compliance with legal obligations and protect their financial interests.

Oregon Notice of Changes to Credit Card Agreement

Description

How to fill out Oregon Notice Of Changes To Credit Card Agreement?

Have you been in a position the place you need papers for sometimes company or individual purposes nearly every time? There are tons of authorized papers layouts available on the Internet, but discovering ones you can trust isn`t simple. US Legal Forms offers a huge number of kind layouts, much like the Oregon Notice of Changes to Credit Card Agreement, which can be written in order to meet state and federal demands.

When you are already familiar with US Legal Forms web site and also have an account, merely log in. After that, you can download the Oregon Notice of Changes to Credit Card Agreement template.

If you do not offer an account and wish to begin using US Legal Forms, abide by these steps:

- Discover the kind you need and make sure it is for that appropriate city/region.

- Utilize the Preview switch to check the form.

- Browse the explanation to actually have chosen the right kind.

- If the kind isn`t what you`re seeking, use the Search industry to get the kind that fits your needs and demands.

- Whenever you discover the appropriate kind, click on Buy now.

- Opt for the prices program you want, fill out the required info to make your money, and pay money for the order utilizing your PayPal or credit card.

- Select a handy data file file format and download your copy.

Discover all the papers layouts you possess bought in the My Forms food list. You can obtain a further copy of Oregon Notice of Changes to Credit Card Agreement any time, if needed. Just select the required kind to download or print out the papers template.

Use US Legal Forms, the most extensive assortment of authorized varieties, in order to save time and prevent mistakes. The services offers skillfully produced authorized papers layouts which you can use for an array of purposes. Create an account on US Legal Forms and begin making your way of life easier.

Form popularity

FAQ

To opt out for five years: Go to optoutprescreen.com or call 1-888-5-OPT-OUT (1-888-567-8688). The major credit bureaus operate the phone number and website. To opt out permanently: Go to optoutprescreen.com or call 1-888-5-OPT-OUT (1-888-567-8688) to start the process. Prescreened Credit and Insurance Offers | Consumer Advice Federal Trade Commission (.gov) ? articles ? prescreened-credit... Federal Trade Commission (.gov) ? articles ? prescreened-credit...

Canceling a credit card can hurt your credit, so it's important to consider the decision carefully before you do so. Creating a well-thought plan will help you avoid or minimize changes to your score. If you decide to close the account, pay off all outstanding balances and cancel recurring payments. Does Canceling a Credit Card Hurt Your Credit? - TransUnion transunion.com ? blog ? credit-advice ? wo... transunion.com ? blog ? credit-advice ? wo...

When they plan to increase your rate or other fees. Your credit card company must send you a notice 45 days before they can increase your interest rate; change certain fees (such as annual fees, cash advance fees, and late fees) that ap- ply to your account; or make other significant changes to the terms of your card.

Generally, the notice must be provided to you at least 45 days before the change takes effect. There are some exceptions: If you agreed to a particular change, the bank must still provide you with a written notice, but it does not have to be provided before the change takes effect.

It depends on the type of change and the terms of your account agreement. If you receive a notice that states you have the right to reject the change, the notice will give you instructions on how you can do so. You can reject many types of changes to your credit card account.

The Credit Card Competition Act of 2023 seeks to provide network choice for processing credit card transactions by requiring banks to name an additional network (besides Visa or Mastercard) to process credit card transactions. What Is The Credit Card Competition Act? | Bankrate bankrate.com ? finance ? credit-cards ? cred... bankrate.com ? finance ? credit-cards ? cred...

In most situations, it's better to keep unused credit card accounts open, as closing credit accounts can have a negative impact on your credit score. Should You Close an Unused Credit Card? | The Motley Fool fool.com ? the-ascent ? should-you-close-un... fool.com ? the-ascent ? should-you-close-un...

The CARD Act requires card issuers to provide written notice to consumers at least 45 days before the effective date of an increase in an annual percentage rate (APR) or any other "significant change."8 This requirement addresses the concern that some issuers were increasing APRs or adversely changing other account ...