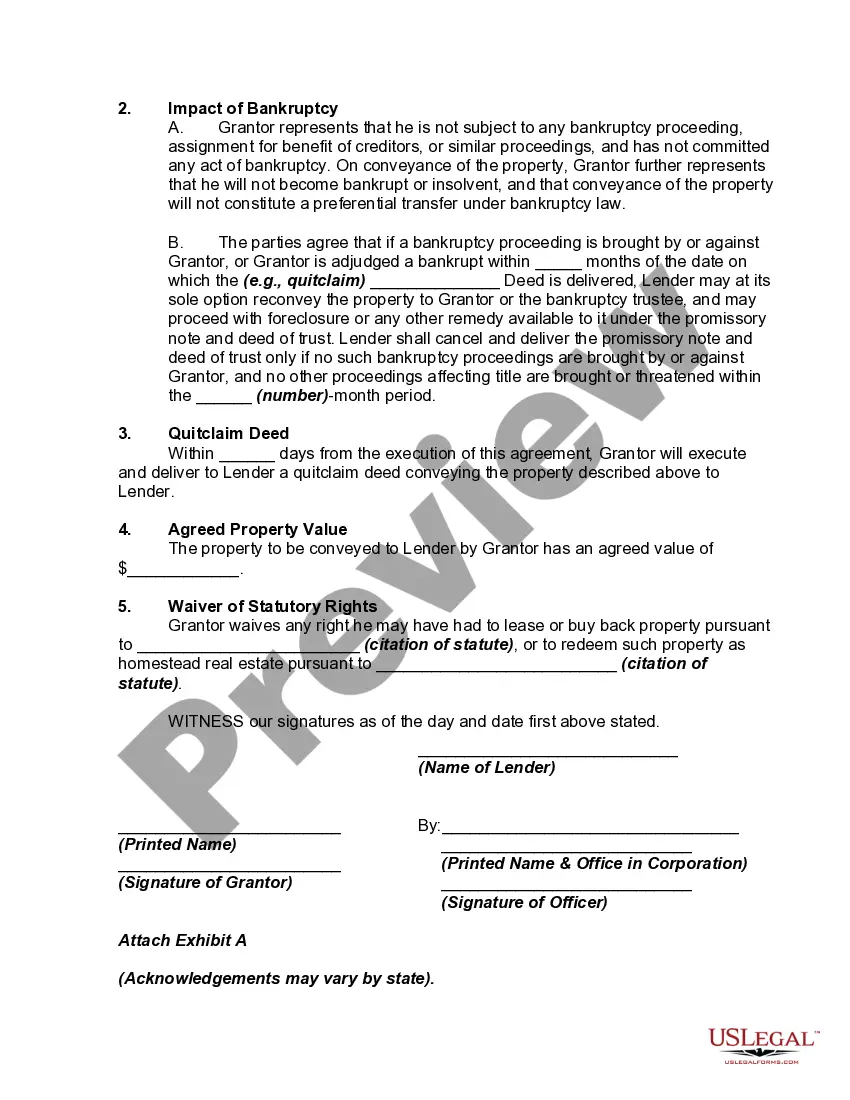

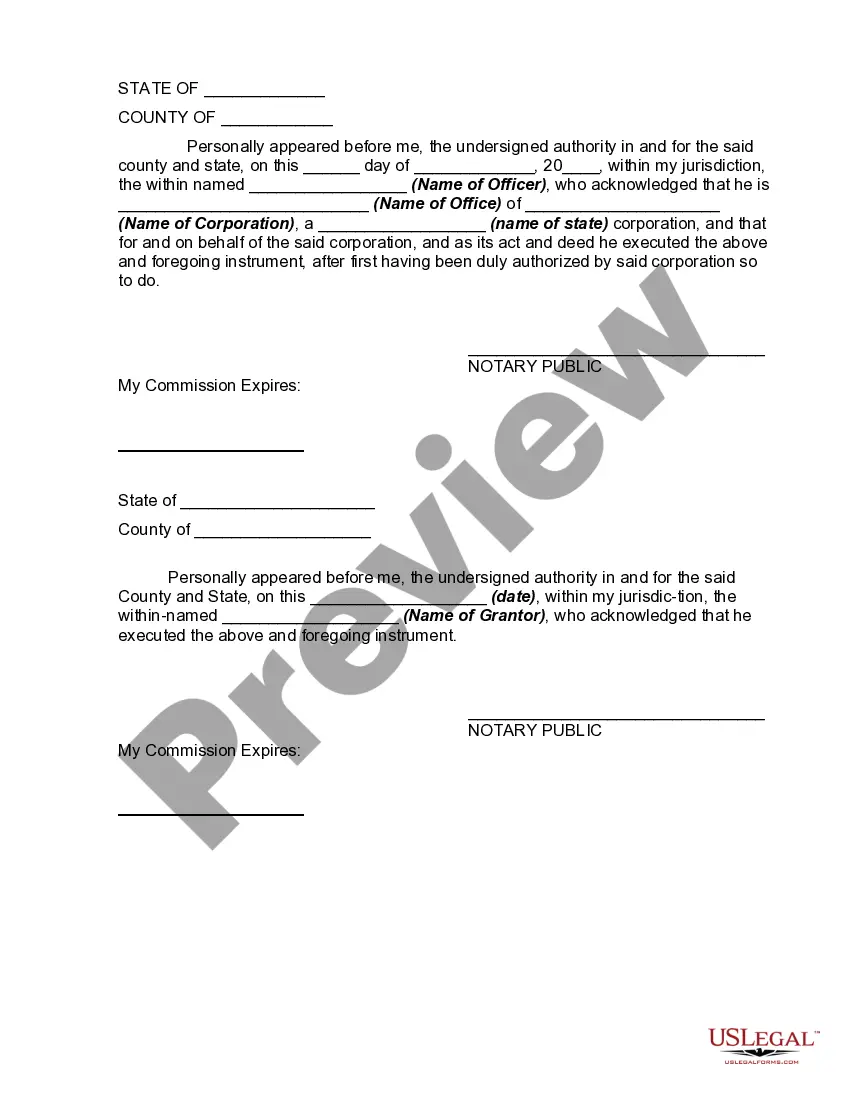

The Oregon Conveyance of Deed to Lender in Lieu of Foreclosure is a legal process that allows a borrower to voluntarily transfer the property's ownership to the lender instead of going through a formal foreclosure procedure. This arrangement can be mutually beneficial for both parties, as it helps the borrower avoid the negative consequences of foreclosure while allowing the lender to quickly take possession of the property. In Oregon, there are two primary types of Conveyance of Deed to Lender in Lieu of Foreclosure: 1. Voluntary Conveyance: This occurs when the borrower decides to proactively offer the deed to the lender as an alternative to foreclosure. It is often initiated when the borrower realizes they are facing financial difficulty that may prevent them from fulfilling their mortgage obligations. By voluntarily conveying the deed, the borrower can avoid the negative impact on their credit score that foreclosure would bring. 2. Negotiated Conveyance: In some cases, the lender might approach the borrower with the option of a negotiated conveyance. This happens when the lender determines that accepting the deed as a form of repayment could be more beneficial than proceeding with foreclosure. Negotiated conveyances often involve discussions between the borrower and lender to determine the terms of the deed transfer, such as potential waivers of deficiency judgments or the handling of outstanding debts. Key terms related to the Oregon Conveyance of Deed to Lender in Lieu of Foreclosure: — Lender: The financial institution or entity that holds the mortgage on the property. They have the legal right to accept the property's deed in lieu of foreclosure. — Foreclosure: The legal process through which a lender seizes and sells a property to recover the outstanding loan amount when a borrower defaults on their mortgage payments. — Deed: A legal document that signifies ownership or title to a property. In the conveyance of deed to the lender, the borrower transfers this ownership to the lender. — Borrower: The individual or entity that obtained a mortgage loan to finance the property and is now facing financial difficulties that may lead to foreclosure. — Credit Score: A numerical representation of an individual's creditworthiness, often used by lenders to evaluate the risk associated with extending credit. — Deficiency Judgment: If the property's value is less than the outstanding loan balance, there may be a deficiency. A deficiency judgment is a court order allowing the lender to collect the remaining debt from the borrower after the conveyance of deed. Understanding the Oregon Conveyance of Deed to Lender in Lieu of Foreclosure is crucial for borrowers who find themselves struggling with mortgage payments. By familiarizing themselves with this process, individuals can make informed decisions regarding their property and financial future, potentially avoiding the negative consequences of foreclosure.

Oregon Conveyance of Deed to Lender in Lieu of Foreclosure

Description

How to fill out Oregon Conveyance Of Deed To Lender In Lieu Of Foreclosure?

US Legal Forms - one of several greatest libraries of legal varieties in America - delivers a wide range of legal file web templates you can obtain or produce. Utilizing the web site, you can find a large number of varieties for company and personal functions, categorized by classes, states, or search phrases.You can get the newest versions of varieties just like the Oregon Conveyance of Deed to Lender in Lieu of Foreclosure within minutes.

If you currently have a monthly subscription, log in and obtain Oregon Conveyance of Deed to Lender in Lieu of Foreclosure from your US Legal Forms catalogue. The Download key will appear on every single develop you view. You get access to all in the past saved varieties in the My Forms tab of your own profile.

If you want to use US Legal Forms for the first time, listed here are simple instructions to obtain started out:

- Be sure to have picked the best develop for your personal area/region. Go through the Preview key to examine the form`s articles. Browse the develop information to ensure that you have chosen the proper develop.

- When the develop doesn`t match your specifications, use the Research area near the top of the monitor to find the the one that does.

- Should you be satisfied with the shape, verify your selection by clicking the Acquire now key. Then, opt for the rates strategy you prefer and give your credentials to sign up on an profile.

- Procedure the deal. Use your bank card or PayPal profile to accomplish the deal.

- Choose the format and obtain the shape in your gadget.

- Make adjustments. Fill up, revise and produce and sign the saved Oregon Conveyance of Deed to Lender in Lieu of Foreclosure.

Every single design you put into your bank account lacks an expiration date and is the one you have forever. So, in order to obtain or produce an additional version, just check out the My Forms portion and click about the develop you want.

Obtain access to the Oregon Conveyance of Deed to Lender in Lieu of Foreclosure with US Legal Forms, one of the most considerable catalogue of legal file web templates. Use a large number of professional and state-distinct web templates that satisfy your business or personal needs and specifications.