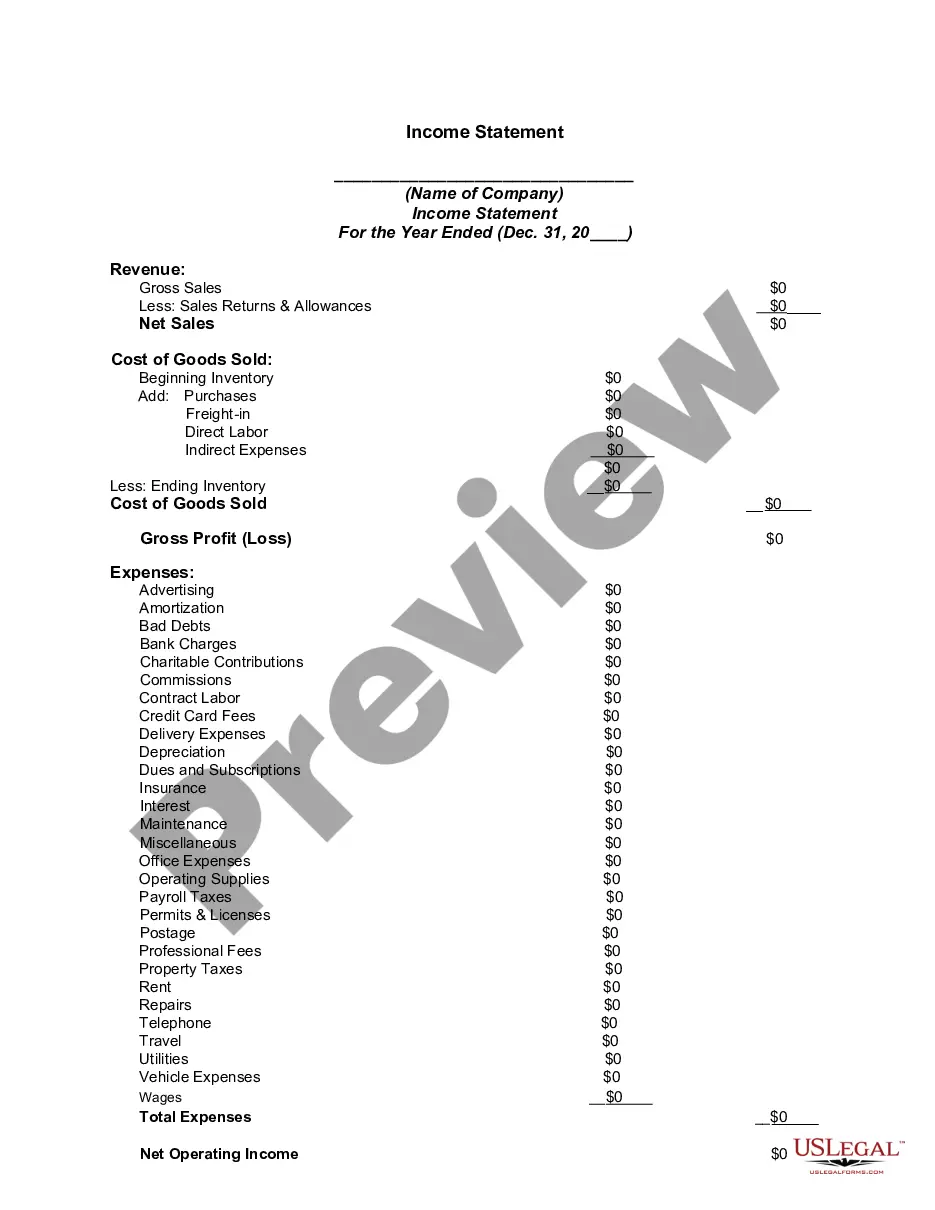

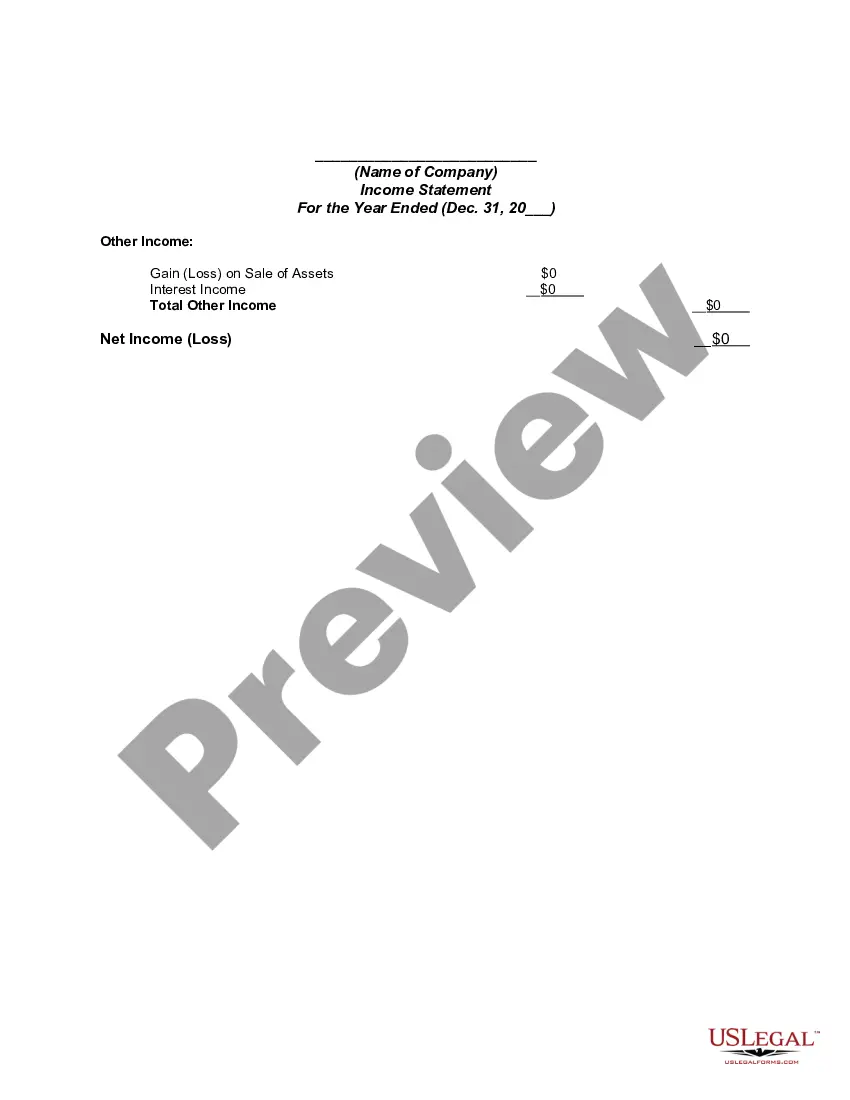

An income statement (sometimes called a profit and loss statement) lists your revenues and expenses, and tells you the profit or loss of your business for a given period of time. You can use this income statement form as a starting point to create one yourself.

The Oregon Income Statement is a crucial financial document that provides a summary of a company's revenues, expenses, and net income during a specific period. It is a key component of financial reporting in Oregon and plays a vital role in analyzing a company's financial performance, profitability, and growth potential. The primary purpose of an Oregon Income Statement is to disclose the company's revenue sources, the costs and expenses incurred, and the resulting profit or loss. It provides insights into the financial health of businesses based in Oregon and helps stakeholders make informed decisions regarding investments, lending, and other financial arrangements. The Oregon Income Statement typically includes several key components: 1. Revenue: This section outlines the total sales, fees, or other income generated by the company during the specified period. It may include sales of products or services, interest income, and gains from investments or asset sales. 2. Cost of Goods Sold (COGS): COGS represents the direct costs associated with producing or delivering goods or services. It encompasses expenses like raw materials, labor, and production overheads. 3. Gross Profit: Gross profit is calculated by subtracting the COGS from the total revenue. It demonstrates the profitability of a company's core operations before considering operating expenses. 4. Operating Expenses: This section covers all the costs incurred in running a business, excluding COGS. Operating expenses commonly include employee salaries, rent, utilities, marketing costs, and other general overhead expenses. 5. Operating Income: By deducting the total operating expenses from the gross profit, the operating income is determined. It reflects the earnings (or losses) generated from recurring business activities before considering non-operating items. 6. Non-Operating Income/Expense: This component accounts for income or expenses derived from activities outside the core business operations. Examples include gains or losses from investments, interest income, or one-off transactions. 7. Net Income: The net income represents the final figure after accounting for all revenues, expenses, and taxes. It showcases the company's overall profitability for the given period. Net income is often used to calculate various financial ratios and assess the financial position of the business. Different types of Oregon Income Statements may exist, depending on the specific reporting requirements or purpose. Some variations of income statements include: 1. Single-step Income Statement: This straightforward format lists all revenues followed by all expenses, resulting in a single operating income figure. It is commonly used by small businesses or for internal reporting. 2. Multi-step Income Statement: This format presents a more detailed breakdown of revenues and expenses, allowing for better analysis. It calculates gross profit and operating income separately, providing a comprehensive view of the company's financial performance. 3. Comparative Income Statement: This type allows for the comparison of financial data across different periods, usually previous years or quarters. By highlighting changes in revenue and expenses over time, it helps identify trends and measure growth. In conclusion, the Oregon Income Statement is a vital tool for assessing the financial performance of businesses based in Oregon. It encapsulates revenues, expenses, and net income, providing valuable insights for decision-making. Understanding the different types of Oregon Income Statements can further enhance the analysis of a company's financial health and facilitate effective financial planning.The Oregon Income Statement is a crucial financial document that provides a summary of a company's revenues, expenses, and net income during a specific period. It is a key component of financial reporting in Oregon and plays a vital role in analyzing a company's financial performance, profitability, and growth potential. The primary purpose of an Oregon Income Statement is to disclose the company's revenue sources, the costs and expenses incurred, and the resulting profit or loss. It provides insights into the financial health of businesses based in Oregon and helps stakeholders make informed decisions regarding investments, lending, and other financial arrangements. The Oregon Income Statement typically includes several key components: 1. Revenue: This section outlines the total sales, fees, or other income generated by the company during the specified period. It may include sales of products or services, interest income, and gains from investments or asset sales. 2. Cost of Goods Sold (COGS): COGS represents the direct costs associated with producing or delivering goods or services. It encompasses expenses like raw materials, labor, and production overheads. 3. Gross Profit: Gross profit is calculated by subtracting the COGS from the total revenue. It demonstrates the profitability of a company's core operations before considering operating expenses. 4. Operating Expenses: This section covers all the costs incurred in running a business, excluding COGS. Operating expenses commonly include employee salaries, rent, utilities, marketing costs, and other general overhead expenses. 5. Operating Income: By deducting the total operating expenses from the gross profit, the operating income is determined. It reflects the earnings (or losses) generated from recurring business activities before considering non-operating items. 6. Non-Operating Income/Expense: This component accounts for income or expenses derived from activities outside the core business operations. Examples include gains or losses from investments, interest income, or one-off transactions. 7. Net Income: The net income represents the final figure after accounting for all revenues, expenses, and taxes. It showcases the company's overall profitability for the given period. Net income is often used to calculate various financial ratios and assess the financial position of the business. Different types of Oregon Income Statements may exist, depending on the specific reporting requirements or purpose. Some variations of income statements include: 1. Single-step Income Statement: This straightforward format lists all revenues followed by all expenses, resulting in a single operating income figure. It is commonly used by small businesses or for internal reporting. 2. Multi-step Income Statement: This format presents a more detailed breakdown of revenues and expenses, allowing for better analysis. It calculates gross profit and operating income separately, providing a comprehensive view of the company's financial performance. 3. Comparative Income Statement: This type allows for the comparison of financial data across different periods, usually previous years or quarters. By highlighting changes in revenue and expenses over time, it helps identify trends and measure growth. In conclusion, the Oregon Income Statement is a vital tool for assessing the financial performance of businesses based in Oregon. It encapsulates revenues, expenses, and net income, providing valuable insights for decision-making. Understanding the different types of Oregon Income Statements can further enhance the analysis of a company's financial health and facilitate effective financial planning.