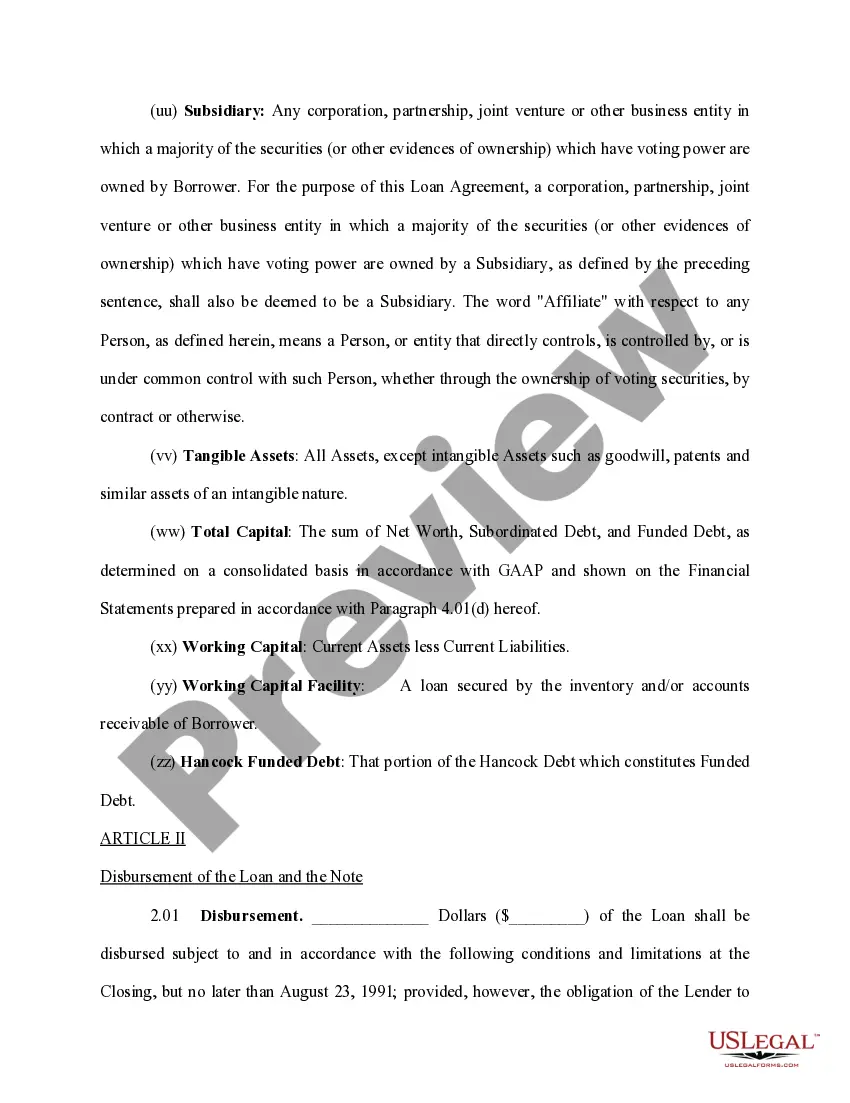

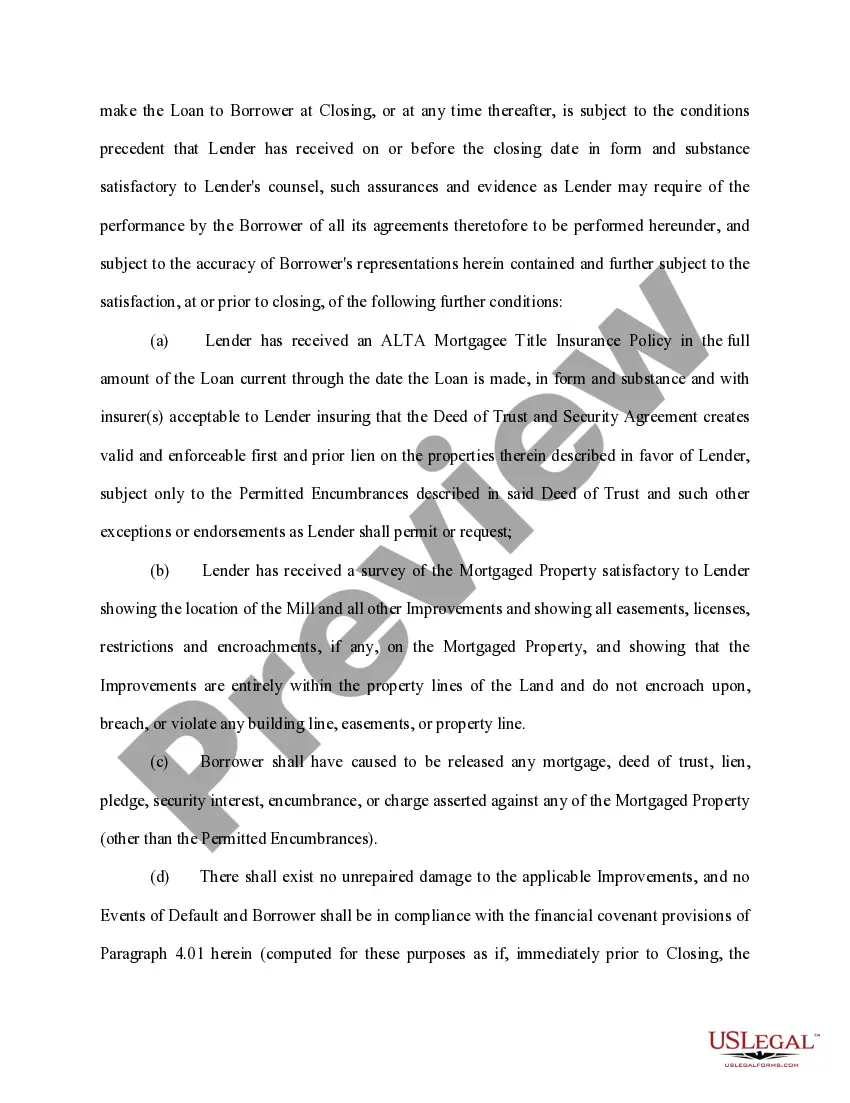

Oregon Loan Agreement for Car is a legally-binding contract that outlines the terms and conditions of borrowing money to purchase a vehicle in the state of Oregon. This loan agreement serves as proof of the loan and specifies the obligations and responsibilities of both the borrower and lender. In Oregon, there are primarily two types of Loan Agreements for cars: 1. Traditional Car Loan Agreement: This is the most common type of loan agreement used when financing a vehicle in Oregon. It involves borrowing money from a lender, often a financial institution such as a bank or credit union, to purchase a car. The agreement will detail the loan amount, interest rate, repayment terms, and any additional fees or charges associated with the loan. The borrower promises to repay the loan according to the specified terms, and the lender may impose penalties or take legal action in case of default. 2. Private Party Car Loan Agreement: This type of loan agreement is used when the vehicle is being purchased directly from an individual seller, rather than through a dealership. Private party car loans are typically less formal than traditional car loans, but it is still crucial to have a written agreement to protect both parties. The agreement should include the loan amount, interest rate (if applicable), repayment schedule, and any other terms agreed upon by the buyer and seller. It is essential to understand the terms and conditions of an Oregon Loan Agreement for Car before signing. Key considerations that should be included in the agreement are: 1. Loan Amount: The total amount being borrowed for the purchase of the car. 2. Interest Rate: The percentage charged on the total loan amount, which directly affects the overall cost of borrowing. 3. Repayment Schedule: The agreed-upon timeline for repaying the loan, including the frequency of payments (monthly, bi-weekly) and the number of payments required to complete the repayment. 4. Late Payment and Default: The consequences of late or missed payments, including potential penalties or additional charges. It is crucial to ensure these terms are fair and reasonable. 5. Security Interest: The loan agreement may include provisions for the lender to take a security interest in the vehicle. This means that if the borrower defaults on the loan, the lender has the right to repossess the vehicle. 6. Governing Law: Specifies that the loan agreement is subject to the laws and regulations of the state of Oregon. 7. Signatures: Both the borrower and lender must sign the loan agreement to make it legally enforceable. Oregon Loan Agreement for Car provides a clear framework for both parties involved in the car financing process. Whether using a traditional car loan or a private party arrangement, having a well-drafted loan agreement is essential to protect the rights and interests of all parties involved.

Oregon Loan Agreement for Car

Description

How to fill out Oregon Loan Agreement For Car?

Choosing the best legitimate papers design can be quite a have difficulties. Obviously, there are a variety of web templates accessible on the Internet, but how would you obtain the legitimate kind you need? Make use of the US Legal Forms internet site. The support provides thousands of web templates, such as the Oregon Loan Agreement for Car, which you can use for organization and personal demands. Every one of the varieties are checked by professionals and fulfill state and federal demands.

Should you be currently signed up, log in to the account and click the Download switch to obtain the Oregon Loan Agreement for Car. Make use of account to appear throughout the legitimate varieties you might have purchased previously. Go to the My Forms tab of your own account and acquire yet another backup from the papers you need.

Should you be a brand new user of US Legal Forms, here are basic recommendations that you can stick to:

- Initial, make sure you have chosen the appropriate kind for your personal area/region. It is possible to examine the form making use of the Review switch and look at the form information to guarantee it is the best for you.

- If the kind fails to fulfill your expectations, utilize the Seach discipline to find the appropriate kind.

- Once you are positive that the form is proper, go through the Purchase now switch to obtain the kind.

- Opt for the pricing program you need and enter in the essential information and facts. Create your account and pay money for the order making use of your PayPal account or charge card.

- Select the data file format and obtain the legitimate papers design to the system.

- Full, modify and produce and indicator the acquired Oregon Loan Agreement for Car.

US Legal Forms will be the biggest library of legitimate varieties where you can see numerous papers web templates. Make use of the company to obtain expertly-made papers that stick to state demands.

Form popularity

FAQ

What to include in your loan agreement? The amount of the loan, also known as the principal amount. The date of the creation of the loan agreement. The name, address, and contact information of the borrower. The name, address, and contact information of the lender.

What should be in a personal loan contract? Names and addresses of the lender and the borrower. Information about the loan co-borrower or cosigner, if it's a joint personal loan. Loan amount and the method for disbursement (lump sum, installments, etc.) Date the loan was provided. Expected repayment date.

Title loans are not available in every state, but it is possible to apply for title loans in Washington.

A title loan in Oregon offers the cash you need to pay for unexpected expenses like medical bills, unexpected bills, or other emergencies. To apply for a title loan, visit an ACE Cash Express near you! We offer title loans in Oregon from $100 - $300. If approved, you could walk out with cash in hand immediately.

To draft a Loan Agreement, you should include the following: The addresses and contact information of all parties involved. The conditions of use of the loan (what the money can be used for) Any repayment options. The payment schedule. The interest rates.

You must provide the lender with your automobile title and the lender holds it until the loan is paid. The limits of these loans are: Must be for at least 31 days and cannot exceed 60 days. If it exceeds 60 days, it is considered an installment loan.