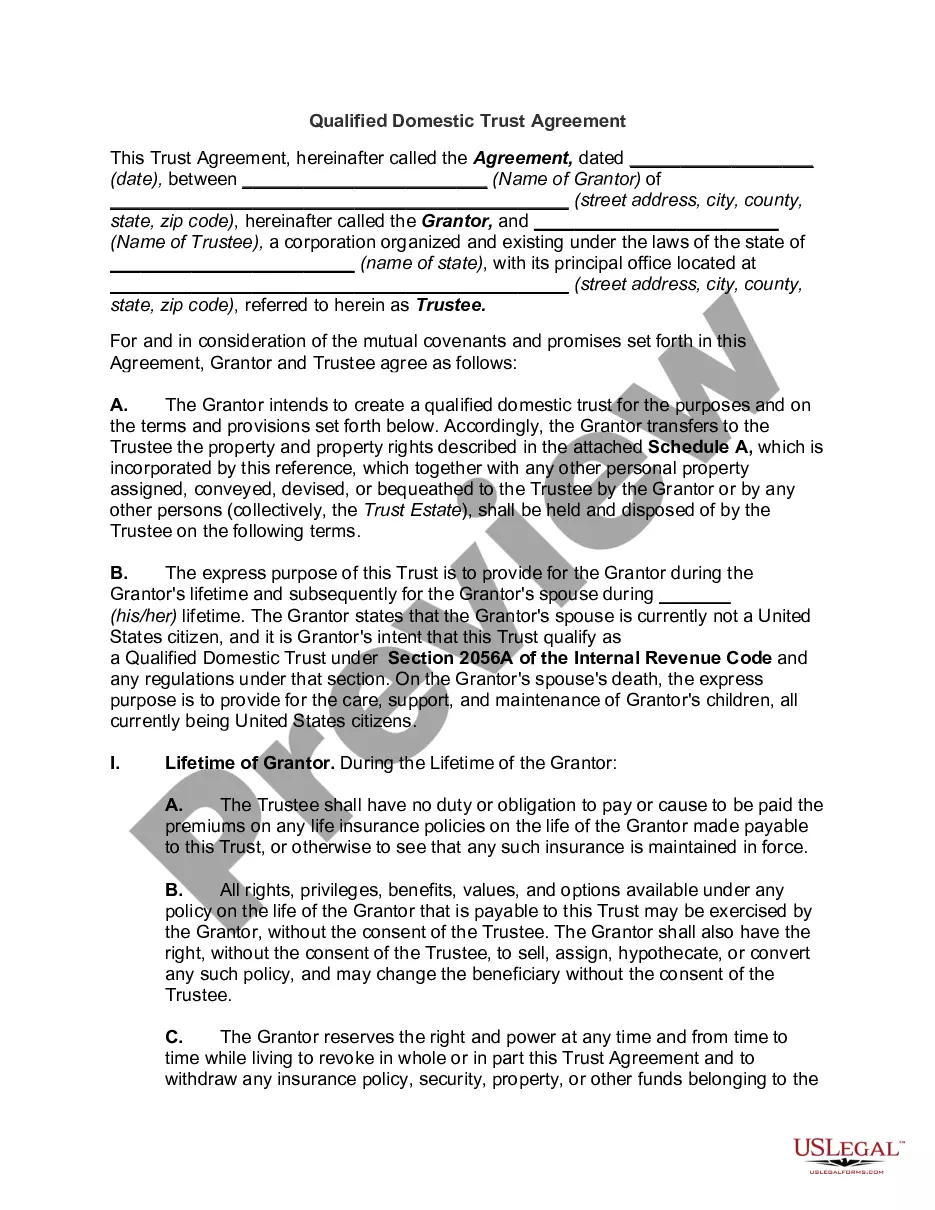

Oregon Qualified Domestic Trust Agreement, also known as Oregon DOT Agreement, is a legal document designed to help non-U.S. citizen spouses or surviving spouses of U.S. citizens or residents protect their assets and ensure their financial security after the death of their spouse. This agreement is created under Oregon law and specifically deals with the taxation of trusts for estate planning purposes. A Qualified Domestic Trust (DOT) is necessary when a non-U.S. citizen spouse inherits property from a U.S. citizen or resident spouse that exceeds the federal estate tax exemption limit. Without a DOT, the non-U.S. citizen spouse would be subject to immediate estate tax on the entire inheritance. However, with a properly structured Oregon DOT Agreement, the estate tax can be deferred until distributions are made from the trust. The primary purpose of an Oregon DOT Agreement is to ensure that estate tax is paid when distributions are made from the trust to the surviving spouse. This allows the non-U.S. citizen spouse to have access to the income generated by the trust while maintaining compliance with U.S. tax laws. There are two main types of Oregon DOT Agreements: 1. Testamentary DOT Agreement: This agreement is established through a provision in the deceased spouse's will. It becomes effective only after the death of the U.S. citizen or resident spouse. It allows for assets to be transferred into the trust upon the spouse's passing, ensuring proper estate tax planning. 2. Inter Vivos or Living DOT Agreement: This agreement is created during the lifetime of the U.S. citizen or resident spouse. Assets can be transferred into the trust while the granter is still alive. It offers flexibility and a proactive approach to estate planning, providing the non-U.S. citizen spouse with the security of knowing their assets are protected. The Oregon DOT Agreement must meet specific requirements set forth by the Internal Revenue Service (IRS) to qualify for the estate tax deferral. Some of these requirements include appointing a U.S. trustee, limiting distributions from the trust to the spouse's needs, and filing annual tax returns for the trust. In conclusion, the Oregon Qualified Domestic Trust Agreement is a valuable tool for non-U.S. citizen spouses or surviving spouses of U.S. citizens or residents to navigate the complexities of U.S. estate tax laws. By utilizing either a testamentary or inter vivos DOT Agreement, individuals can protect their assets and ensure financial security for themselves and their loved ones.

Oregon Qualified Domestic Trust Agreement

Description

How to fill out Oregon Qualified Domestic Trust Agreement?

Choosing the right authorized papers design can be a have a problem. Needless to say, there are tons of themes available on the net, but how can you get the authorized kind you will need? Make use of the US Legal Forms internet site. The support gives thousands of themes, for example the Oregon Qualified Domestic Trust Agreement, which can be used for organization and personal demands. All the forms are inspected by professionals and meet state and federal requirements.

In case you are currently signed up, log in to the account and then click the Acquire button to obtain the Oregon Qualified Domestic Trust Agreement. Make use of your account to check through the authorized forms you have purchased in the past. Go to the My Forms tab of the account and get one more backup from the papers you will need.

In case you are a fresh user of US Legal Forms, here are easy directions for you to comply with:

- First, ensure you have selected the right kind for your personal city/state. You are able to look through the shape making use of the Preview button and study the shape information to ensure this is basically the right one for you.

- In case the kind does not meet your requirements, take advantage of the Seach discipline to get the proper kind.

- When you are certain the shape is suitable, go through the Acquire now button to obtain the kind.

- Opt for the pricing prepare you need and type in the essential details. Build your account and pay money for the transaction utilizing your PayPal account or charge card.

- Select the document file format and download the authorized papers design to the product.

- Comprehensive, edit and print out and indication the obtained Oregon Qualified Domestic Trust Agreement.

US Legal Forms may be the most significant library of authorized forms that you can find various papers themes. Make use of the company to download expertly-created paperwork that comply with express requirements.