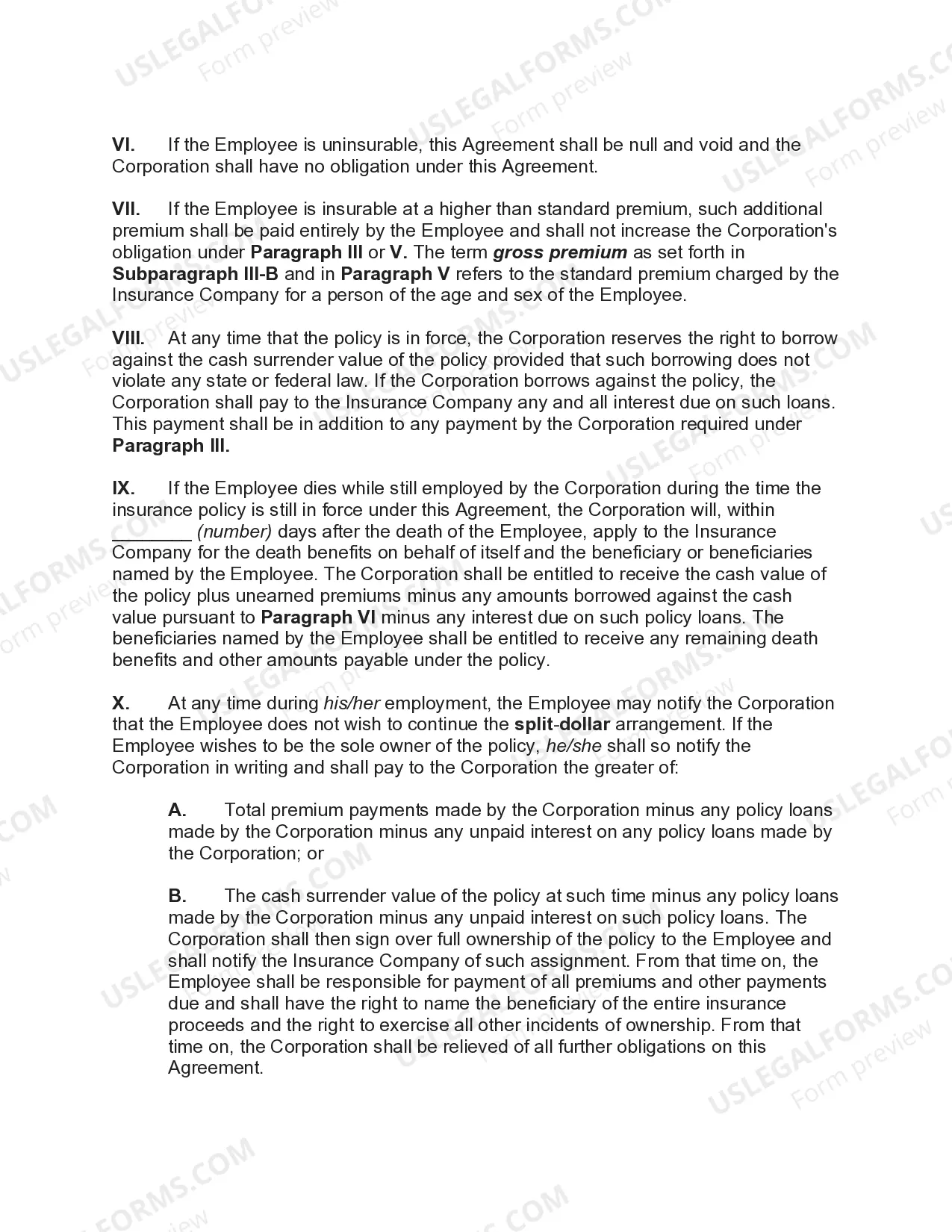

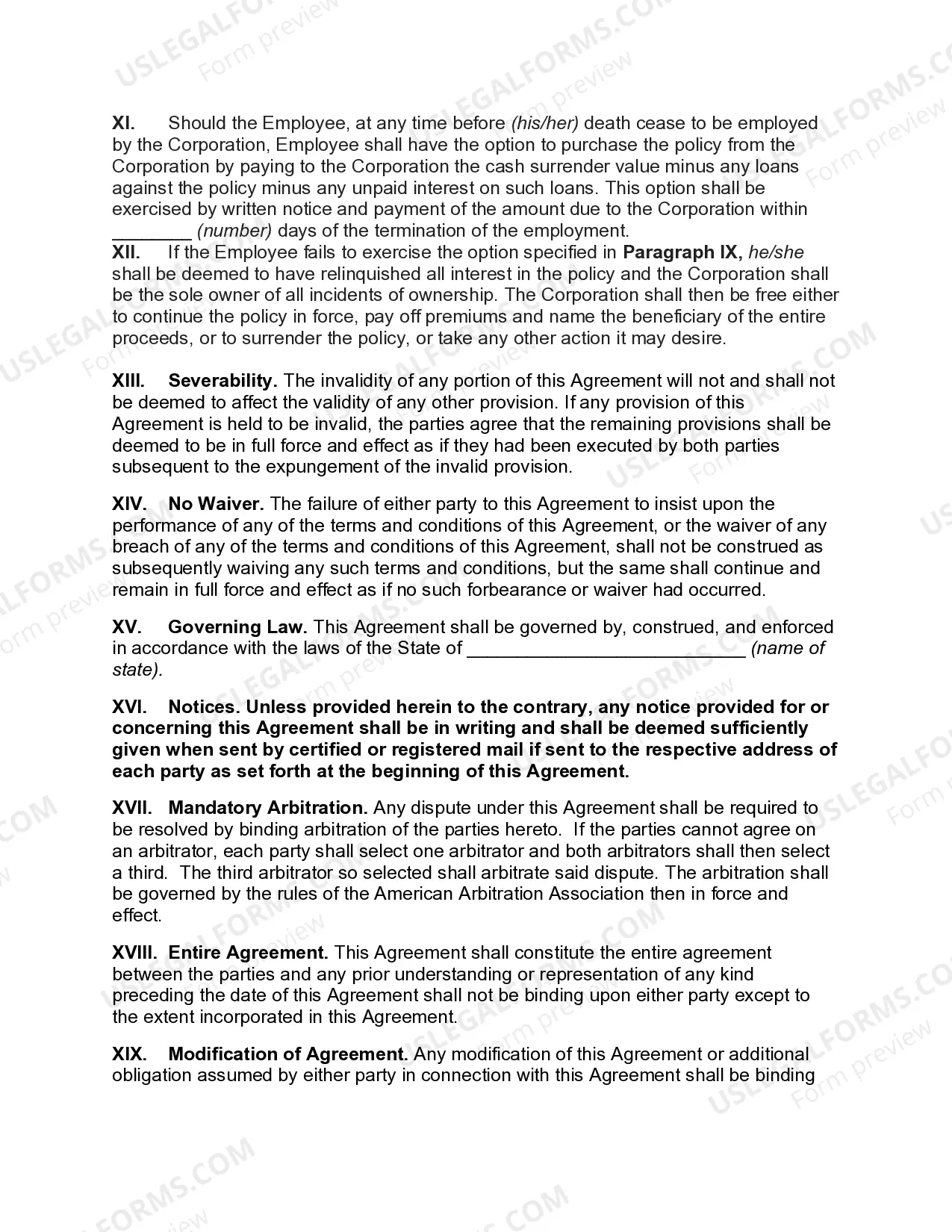

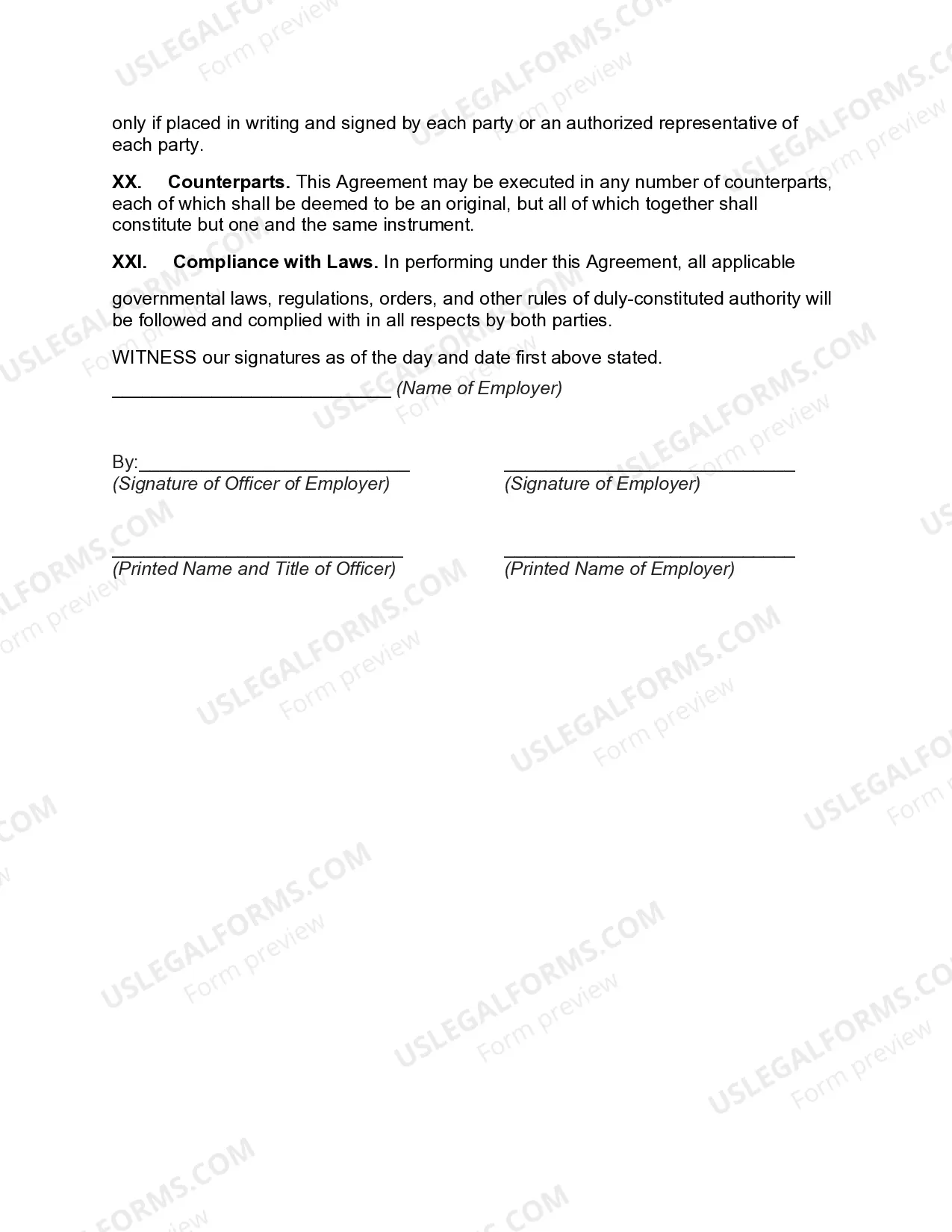

Oregon Split-Dollar Insurance Agreement with Policy Owned Jointly by Employer and Employee is a financial arrangement where the employer and the employee enter into an agreement to jointly own a life insurance policy. This arrangement generally involves the employer paying a portion of the insurance premiums while the employee pays the remaining portion. Split-dollar insurance is a common method used by employers to provide their key employees with valuable life insurance coverage. It is often used as a retention tool or as a means to help executives and other high-level employees protect their families financially. In the state of Oregon, there are different types of Split-Dollar Insurance Agreements with Policy Owned Jointly by Employer and Employee. These agreements may vary based on the terms and conditions set forth by both parties involved. Let's explore a few of these types: 1. Traditional Split-Dollar Agreement: This is the most basic form of split-dollar agreement where the employer and the employee mutually agree to share the premium payments and the benefits of the policy upon the employee's death. The agreement may specify the percentage of ownership or premium payments assumed by each party. 2. Endorsement Split-Dollar Agreement: In this type of arrangement, the employer pays the premiums and is the sole owner of the policy. However, the employee receives a contractual right to a portion of the policy's cash value or death benefit. The employer typically recovers its premium payments upon the employee's death. 3. Collateral Assignment Split-Dollar Agreement: Here, the employer takes out a loan to pay the premium costs, and the policy is assigned to a financial institution as collateral for the loan. The employee retains the rights to a portion of the policy's cash value or death benefit. The employer's loan is repaid upon the employee's death. These are just a few examples of Oregon Split-Dollar Insurance Agreements with Policy Owned Jointly by Employer and Employee. The specifics of these agreements can be customized based on the unique needs and preferences of both the employer and the employee. It is essential to consult with a qualified insurance professional or attorney to ensure compliance with state laws and to fully understand the benefits and implications of entering into such an agreement.

Oregon Split-Dollar Insurance Agreement with Policy Owned Jointly by Employer and Employee

Description

How to fill out Oregon Split-Dollar Insurance Agreement With Policy Owned Jointly By Employer And Employee?

Discovering the right legitimate papers format might be a battle. Of course, there are plenty of web templates accessible on the Internet, but how will you find the legitimate kind you will need? Make use of the US Legal Forms internet site. The services offers a large number of web templates, like the Oregon Split-Dollar Insurance Agreement with Policy Owned Jointly by Employer and Employee, that can be used for company and personal requirements. Each of the types are examined by pros and satisfy state and federal needs.

When you are currently listed, log in to the accounts and click the Down load button to get the Oregon Split-Dollar Insurance Agreement with Policy Owned Jointly by Employer and Employee. Make use of your accounts to appear with the legitimate types you may have bought formerly. Visit the My Forms tab of the accounts and have an additional backup from the papers you will need.

When you are a new end user of US Legal Forms, here are basic guidelines that you should adhere to:

- Initially, make sure you have selected the appropriate kind for your metropolis/area. It is possible to check out the form while using Preview button and browse the form explanation to ensure this is basically the best for you.

- In the event the kind does not satisfy your preferences, use the Seach area to discover the appropriate kind.

- Once you are sure that the form is suitable, go through the Buy now button to get the kind.

- Pick the pricing strategy you need and enter in the needed info. Make your accounts and buy your order making use of your PayPal accounts or charge card.

- Pick the document formatting and download the legitimate papers format to the system.

- Complete, revise and printing and signal the received Oregon Split-Dollar Insurance Agreement with Policy Owned Jointly by Employer and Employee.

US Legal Forms is definitely the most significant collection of legitimate types in which you can find various papers web templates. Make use of the company to download professionally-created papers that adhere to express needs.