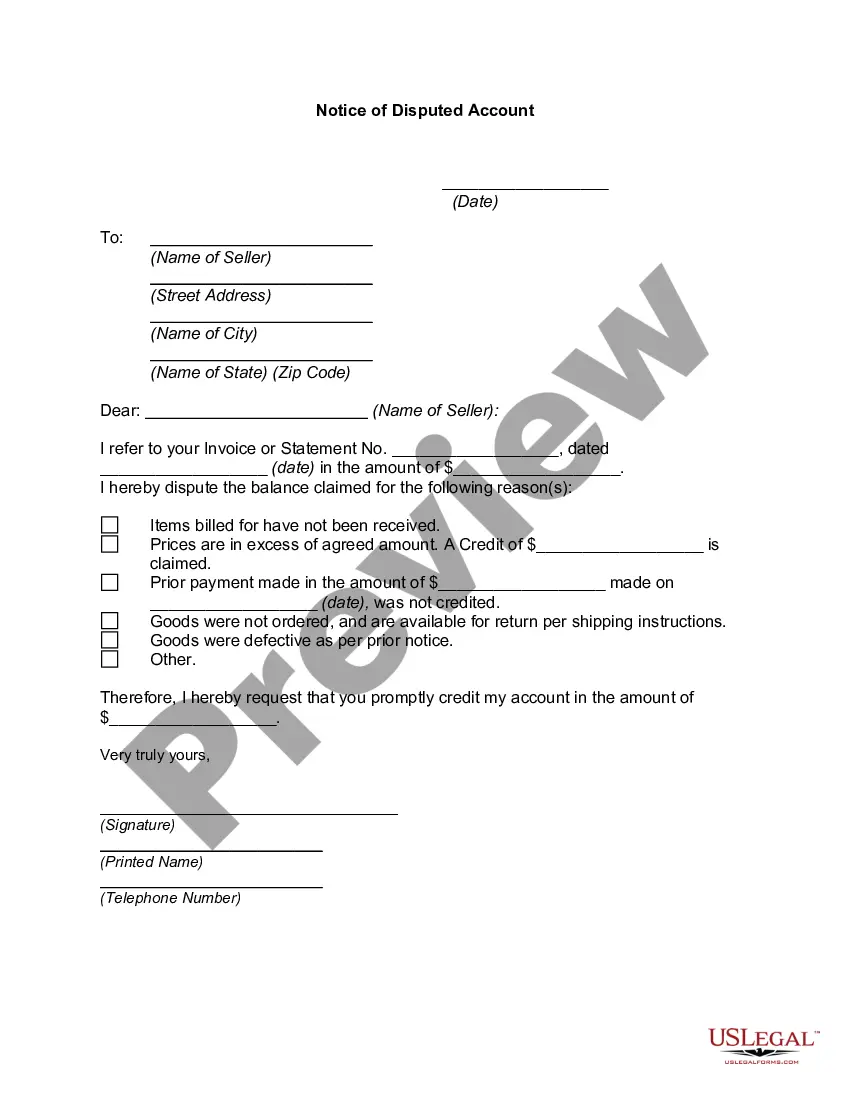

The Oregon Notice of Disputed Account is an important document used by consumers in the state of Oregon to formally dispute inaccuracies or errors related to their financial accounts. This notice is designed to protect consumers' rights under the Fair Credit Reporting Act (FCRA) and ensure the accuracy of their credit information. When a consumer discovers incorrect or unauthorized information on their credit report or other financial statements, they can use the Oregon Notice of Disputed Account to notify the relevant financial institution or credit reporting agency about the discrepancy. By doing so, they initiate a process that aims to investigate and resolve the disputed account as per the legal requirements. Here are some relevant keywords related to the Oregon Notice of Disputed Account: 1. Disputed Account: This refers to the financial account or entry that the consumer believes contains inaccurate or unauthorized information. 2. Fair Credit Reporting Act (FCRA): The federal law that regulates how consumer credit information is collected, shared, and used, and provides consumers with specific rights and protections in relation to their credit reports. 3. Credit Reporting Agency: Companies that compile credit information and provide credit reports to lenders, landlords, and other authorized parties. Examples include Equifax, Experian, and TransUnion. 4. Financial Institution: A bank, credit union, or any entity that holds or manages a consumer's financial account, such as a credit card issuer or a mortgage lender. 5. Inaccuracies: Refers to any incorrect, outdated, incomplete, or erroneous information found on the account or credit report that needs to be rectified. 6. Unauthorized Charges: Refers to any charges or transactions made on the account without the consumer's consent or knowledge. 7. Investigate and Resolve: The process initiated by the Notice of Disputed Account, where the financial institution or credit reporting agency is required to investigate the claim, correct any inaccurate information, and inform the consumer of the outcome. 8. Resolution Timeline: The time frame within which the financial institution or credit reporting agency must complete the investigation and provide a resolution to the consumer. It's worth noting that while the term "Oregon Notice of Disputed Account" generally refers to the standard process for disputing account-related errors, there may not be different types of notices specifically designated under this name. However, the concept of disputing erroneous account information is applicable to various types of financial accounts, such as credit cards, mortgages, auto loans, and student loans. The same principles apply regardless of the specific type of account being disputed.

Oregon Notice of Disputed Account

Description

How to fill out Oregon Notice Of Disputed Account?

You may devote hrs on-line attempting to find the legal record format that meets the state and federal demands you will need. US Legal Forms provides thousands of legal forms which are evaluated by experts. It is simple to obtain or produce the Oregon Notice of Disputed Account from my services.

If you already possess a US Legal Forms bank account, you may log in and click the Download button. Next, you may comprehensive, modify, produce, or indication the Oregon Notice of Disputed Account. Every single legal record format you acquire is the one you have permanently. To get yet another copy of the purchased kind, check out the My Forms tab and click the related button.

If you use the US Legal Forms web site initially, stick to the basic instructions below:

- Very first, be sure that you have selected the best record format for your area/metropolis that you pick. See the kind explanation to ensure you have selected the right kind. If readily available, utilize the Review button to search throughout the record format also.

- In order to find yet another model of your kind, utilize the Look for industry to get the format that meets your needs and demands.

- After you have found the format you would like, click Get now to continue.

- Find the prices prepare you would like, enter your qualifications, and register for your account on US Legal Forms.

- Comprehensive the deal. You should use your Visa or Mastercard or PayPal bank account to fund the legal kind.

- Find the file format of your record and obtain it to your system.

- Make adjustments to your record if needed. You may comprehensive, modify and indication and produce Oregon Notice of Disputed Account.

Download and produce thousands of record templates while using US Legal Forms web site, that offers the most important assortment of legal forms. Use professional and status-certain templates to handle your small business or individual needs.