Oregon Fair Credit Act Disclosure Notice

Description

How to fill out Fair Credit Act Disclosure Notice?

If you need extensive, acquire, or printing sanctioned document templates, utilize US Legal Forms, the largest compilation of official forms, available online.

Employ the website's straightforward and user-friendly search tool to find the documents you require.

Various templates for business and personal purposes are categorized by types and states, or keywords.

Step 4. After finding the form you need, click on the Get now button. Choose your pricing plan and provide your information to register for an account.

Step 5. Complete the transaction. You can use your Visa or MasterCard or PayPal account to finalize the payment.

- Employ US Legal Forms to discover the Oregon Fair Credit Act Disclosure Notice with just a few clicks.

- If you are already a US Legal Forms customer, Log In to your account and then click the Obtain button to retrieve the Oregon Fair Credit Act Disclosure Notice.

- You can also access forms you previously downloaded in the My documents section of your account.

- If this is your first time using US Legal Forms, follow the steps below.

- Step 1. Ensure you have selected the form for the correct city/state.

- Step 2. Use the Preview option to review the form's content. Remember to read the description.

- Step 3. If you are not satisfied with the form, use the Search area at the top of the screen to locate other versions of the legal form template.

Form popularity

FAQ

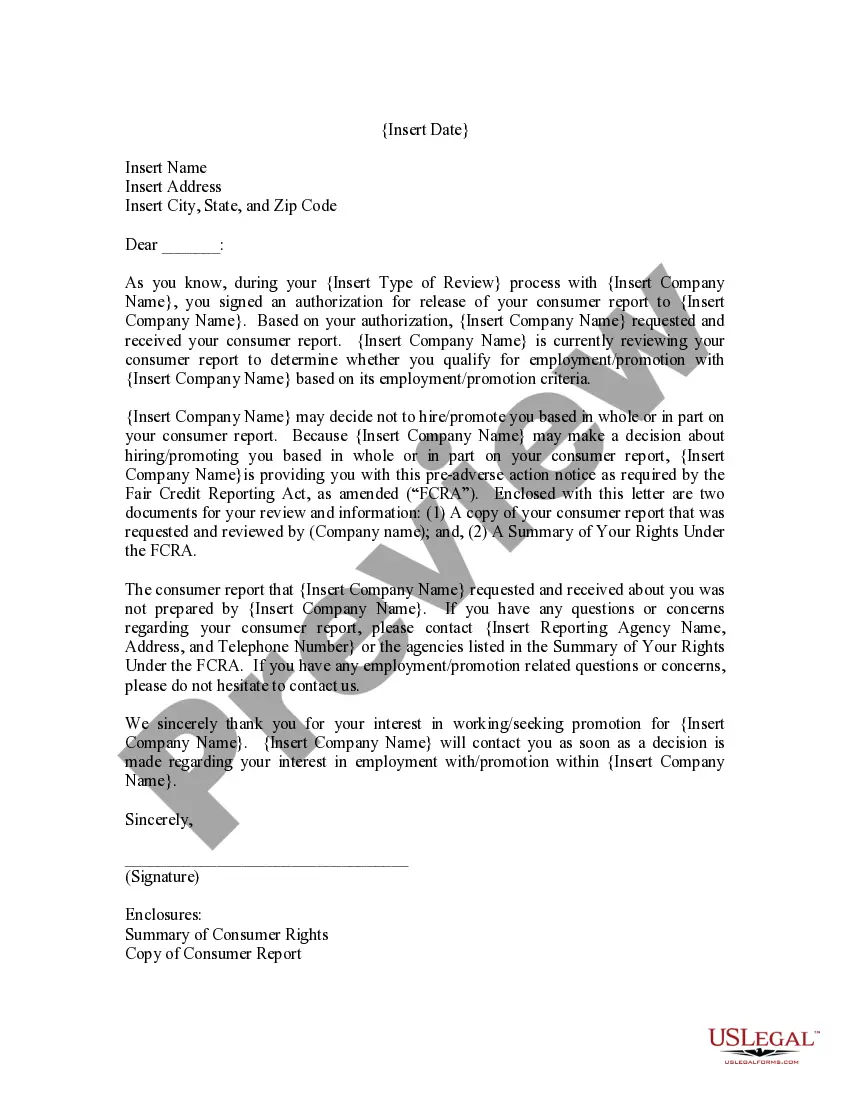

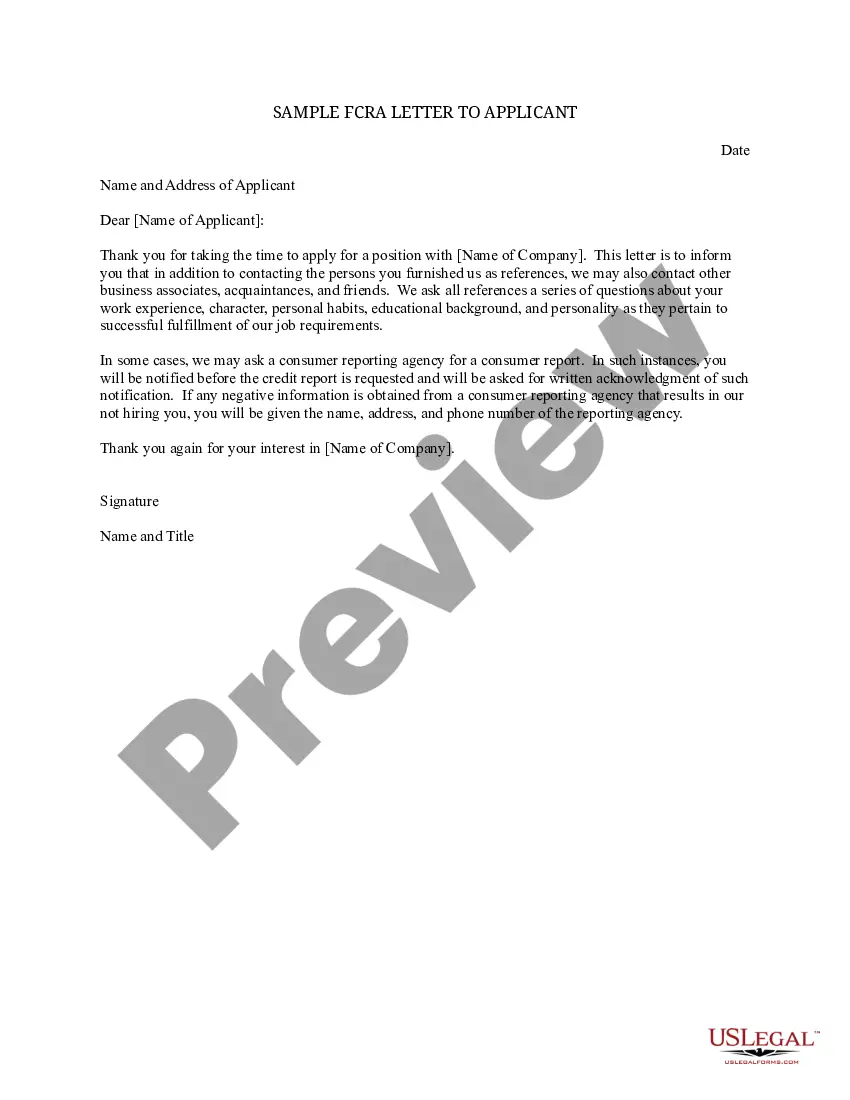

The FCRA gives you the right to be told if information in your credit file is used against you to deny your application for credit, employment or insurance. The FCRA also gives you the right to request and access all the information a consumer reporting agency has about you (this is called "file disclosure").

Credit Score Disclosure Section 609(g) referenced above has another requirement where a creditor must send a "credit score disclosure" to an applicant of a consumer loan secured by 1 to 4 units of residential real property.

A creditor must disclose a consumer's credit score and information relating to a credit score on a risk-based pricing notice when the score of the consumer to whom the creditor extends credit or whose extension of credit is under review is used in setting the material terms of credit.

A Credit Score Disclosure alerts a consumer of their FICO scores, defines what a FICO is, informs how FICO scores affect their access to consumer credit and provides contact information for the bureaus.

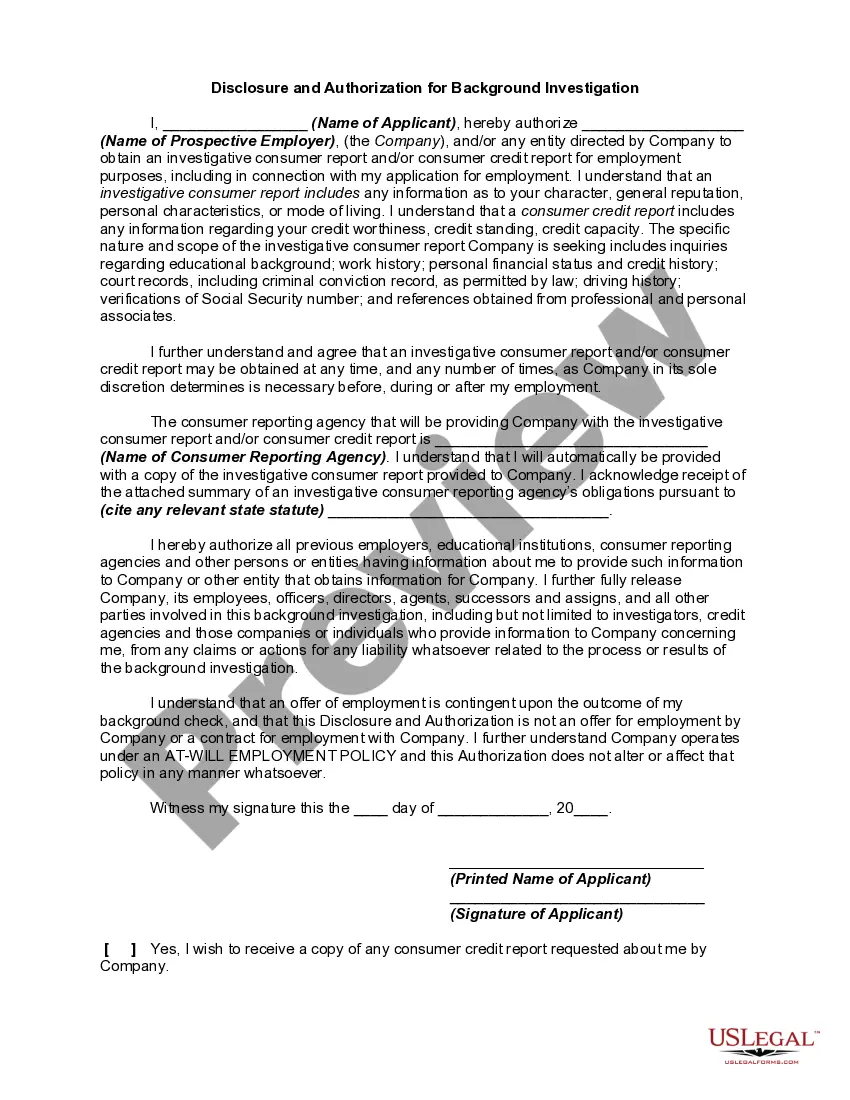

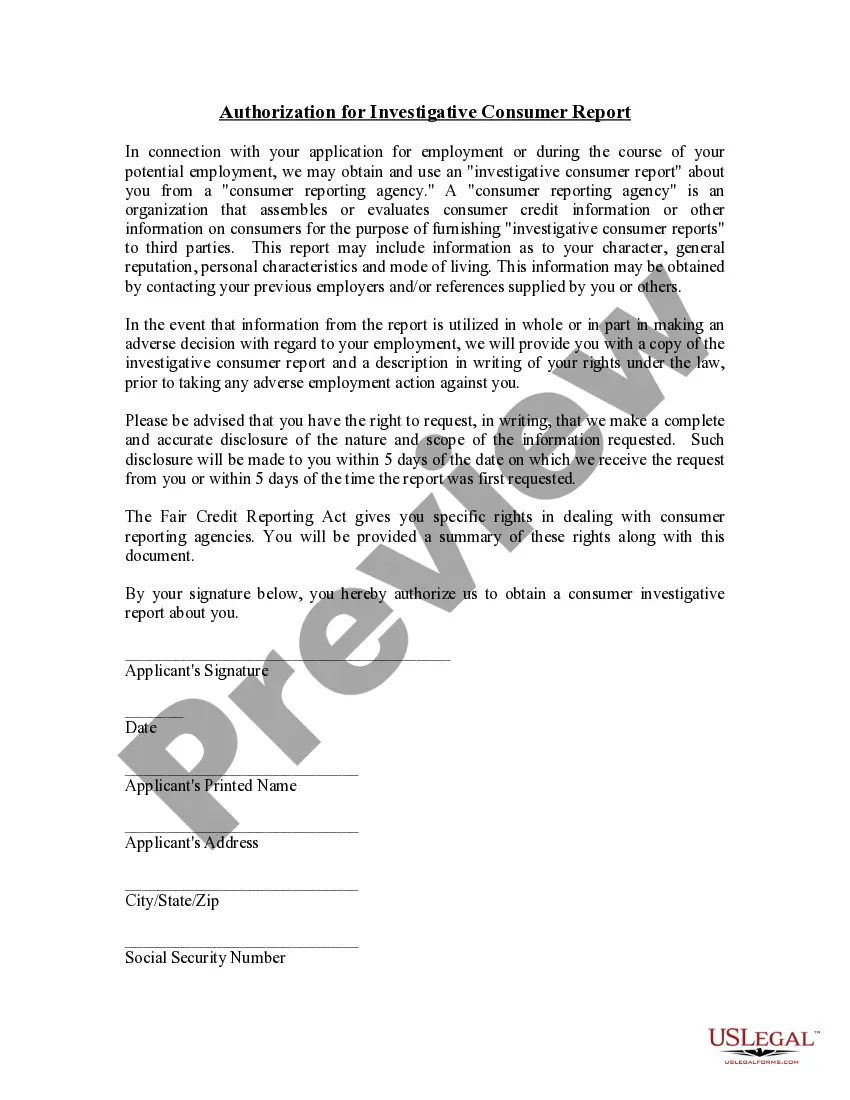

Under the FCRA, an employer may not run a background check on a prospective employee without first providing "a clear and conspicuous disclosure . . . in a document that consists solely of that disclosure, that a consumer report may be obtained for employment purposes." For efficiency, many employers include all

Under the FCRA, an employer may not run a background check on a prospective employee without first providing "a clear and conspicuous disclosure . . . in a document that consists solely of that disclosure, that a consumer report may be obtained for employment purposes." For efficiency, many employers include all

The Dodd-Frank Act also amended two provisions of the FCRA to require the disclosure of a credit score and related information when a credit score is used in taking an adverse action or in risk-based pricing. On December 21, 2011, the CFPB restated FCRA regulations under its authority at 12 CFR Part 1022 (76 Fed. Reg.

Consumer reporting agencies must correct or delete inaccurate, incomplete, or unverifiable information. Inaccurate, incomplete, or unverifiable information must be removed or corrected, usually within 30 days. However, a consumer reporting agency may continue to report information it has verified as accurate.

Section 612(a) of the FCRA gives consumers the right to a free file disclosure upon request once every 12 months from the nationwide consumer reporting agencies and nationwide specialty consumer reporting agencies.

The Act (Title VI of the Consumer Credit Protection Act) protects information collected by consumer reporting agencies such as credit bureaus, medical information companies and tenant screening services. Information in a consumer report cannot be provided to anyone who does not have a purpose specified in the Act.