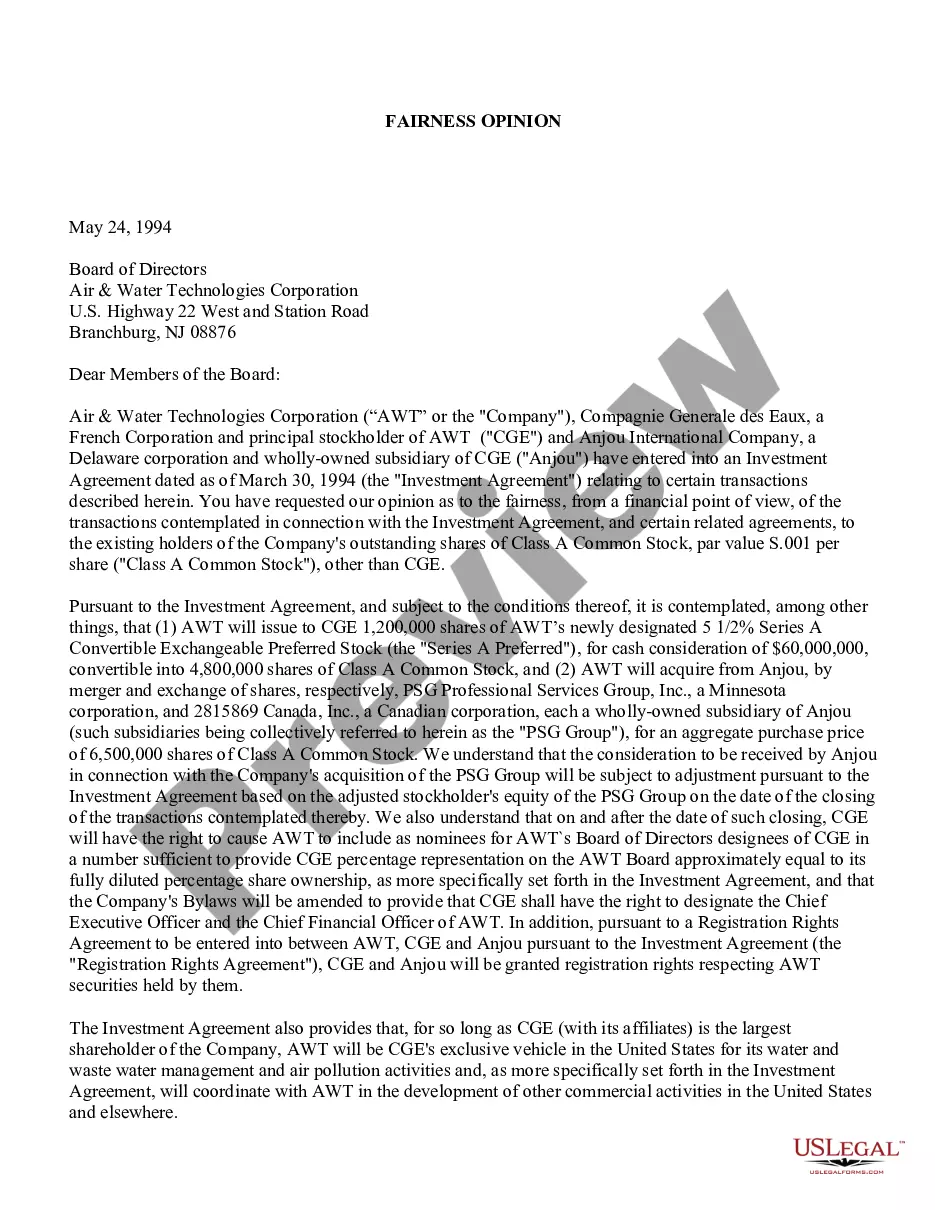

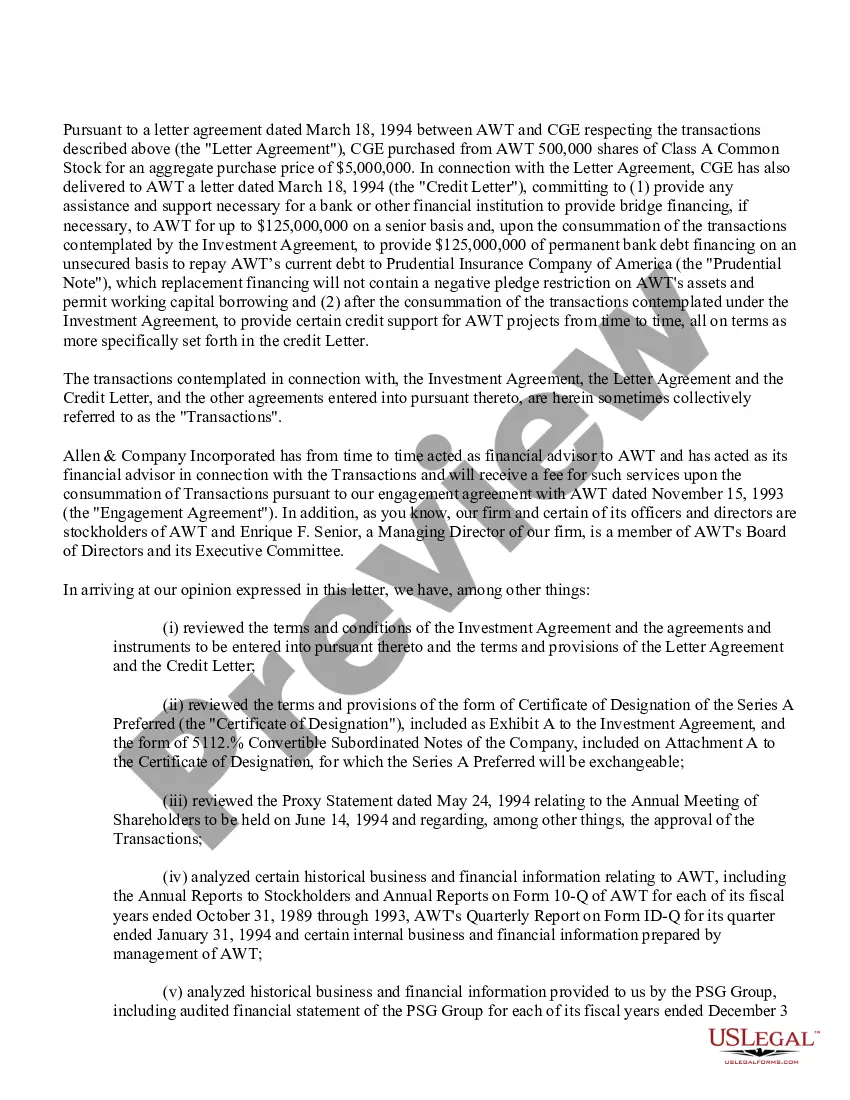

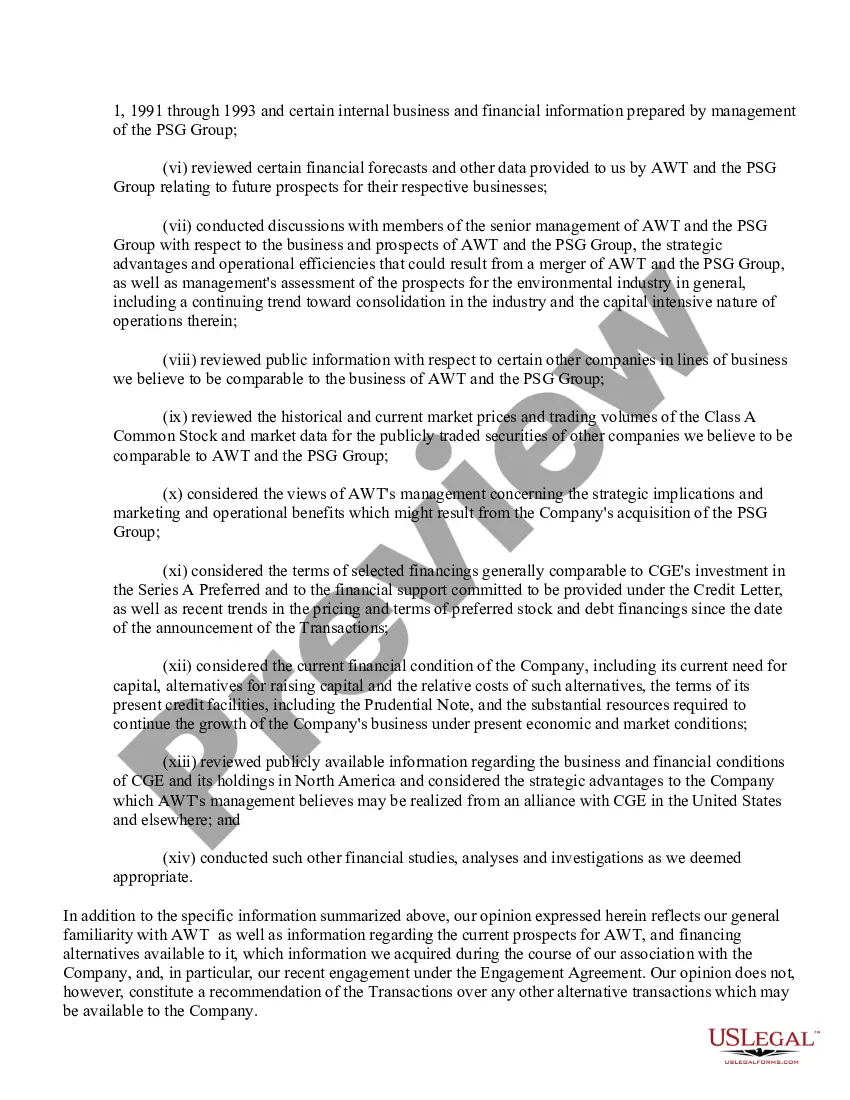

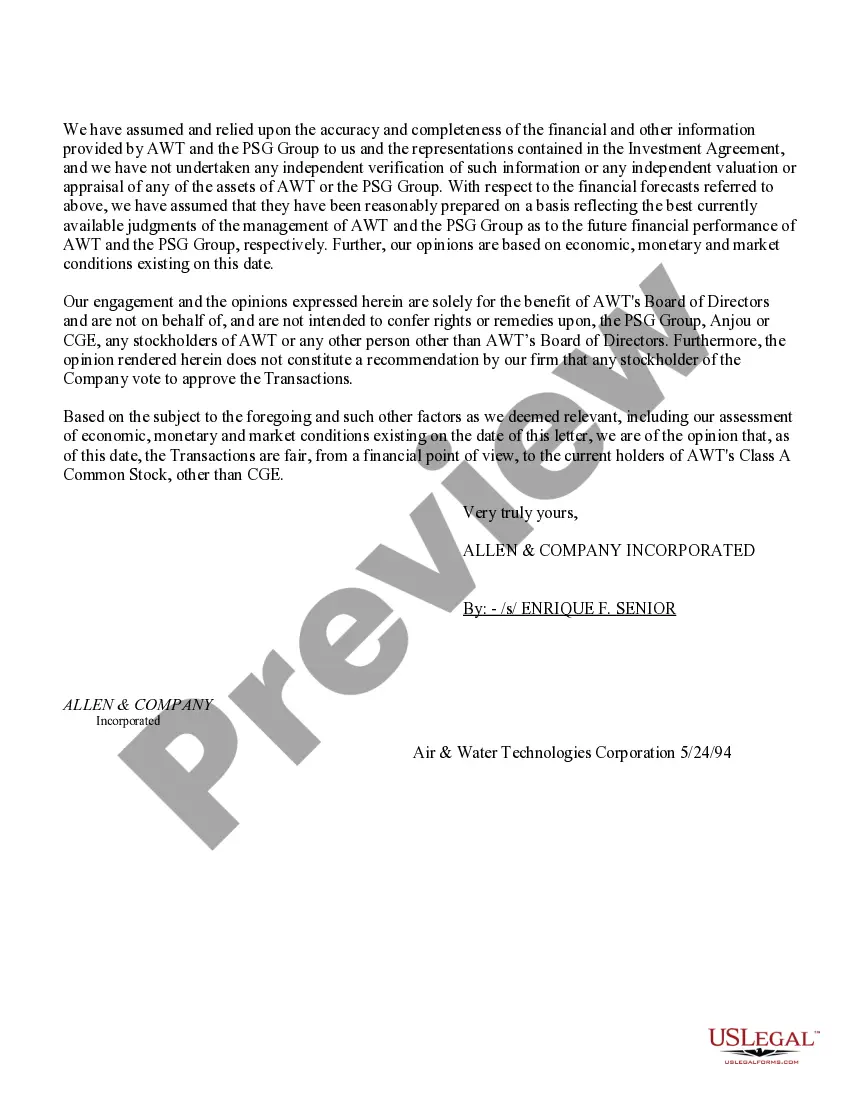

Title: Understanding the Oregon Letter to Board of Directors — Fairness Opinion Introduction: The Oregon Letter to Board of Directors — Fairness Opinion serves as a critical document in corporate transactions. It provides an independent assessment of the fairness of a transaction proposal to safeguard the interests of various stakeholders. This article delves into the purpose, types, and key components of the Oregon Letter to Board of Directors — Fairness Opinion, shedding light on its significance within corporate decision-making. 1. What is the Oregon Letter to Board of Directors — Fairness Opinion? The Oregon Letter to Board of Directors — Fairness Opinion is a formal letter issued by an impartial third-party firm, usually an investment banker or valuation expert. It assists the Board of Directors in evaluating the fairness of a proposed business transaction, such as a merger, acquisition, or significant corporate restructuring. It enables directors to fulfill their fiduciary duty to act in the best interest of shareholders. 2. Key Components: a. Background and scope: The letter provides a clear description of the transaction, its purpose, and the entities involved. It outlines the scope of the opinion, highlighting the specific aspects evaluated. b. Methodology: The fairness opinion introduces the analytical methods employed to assess the transaction. It may involve financial analysis, market comparisons, or industry-specific valuation techniques. c. Evaluation criteria: The opinion states the criteria against which fairness is assessed, such as price, financial terms, synergies, and other relevant factors. These criteria align with industry standards and regulatory requirements. d. Financial analyses: The letter presents comprehensive financial analyses, including pro forma financial statements, discounted cash flow (DCF) analysis, comparable company analysis, and other relevant valuation metrics. e. Assumptions and limitations: The fairness opinion explicitly mentions the assumptions made during the evaluation process and identifies any limitations in the data or methodologies used. f. Conclusion: Based on the evaluation, the fairness opinion concludes whether the proposed transaction is fair, from a financial perspective, to the shareholders involved. 3. Types of Oregon Letters to Board of Directors — Fairness Opinion: a. Sell-side opinion: Provided by an independent financial advisor engaged by a company that is selling assets or considering a merger or acquisition. The opinion aims to reassure the board and shareholders that the transaction is fair. b. Buy-side opinion: Similar to the sell-side opinion, this type is employed when a company seeks an external assessment to confirm that the proposed acquisition is fair and reasonable. c. Going-private opinion: This type of fairness opinion is required when a publicly traded company is considering taking the company private. The opinion evaluates the fairness of the buyout offer to the shareholders. d. Spin-off opinion: Issued when a company plans to separate a subsidiary or a division into an independent entity. This fairness opinion assesses the fairness of the proposed terms for shareholders of the spun-off company. Conclusion: The Oregon Letter to Board of Directors — Fairness Opinion plays a critical role in corporate decision-making processes. It ensures transparency, protects the interests of shareholders, and promotes accountability among the board of directors. Understanding its purpose and various types enables businesses to navigate significant transactions with confidence, fostering trust and credibility within the corporate sphere.

Oregon Letter to Board of Directors - Fairness Opinion

Description

How to fill out Oregon Letter To Board Of Directors - Fairness Opinion?

Are you currently within a position the place you will need paperwork for both business or person functions virtually every working day? There are a variety of authorized papers layouts available online, but locating kinds you can depend on is not simple. US Legal Forms gives a large number of kind layouts, just like the Oregon Letter to Board of Directors - Fairness Opinion, which are published to meet state and federal requirements.

Should you be already knowledgeable about US Legal Forms internet site and get your account, just log in. Following that, it is possible to acquire the Oregon Letter to Board of Directors - Fairness Opinion format.

Unless you have an accounts and would like to start using US Legal Forms, abide by these steps:

- Find the kind you will need and make sure it is for the appropriate area/area.

- Use the Preview option to analyze the form.

- See the explanation to actually have selected the appropriate kind.

- If the kind is not what you`re seeking, take advantage of the Lookup discipline to discover the kind that meets your needs and requirements.

- Whenever you get the appropriate kind, simply click Get now.

- Opt for the rates plan you want, fill in the specified information and facts to generate your money, and pay for the order with your PayPal or charge card.

- Pick a handy paper structure and acquire your backup.

Find all the papers layouts you may have bought in the My Forms menu. You can aquire a further backup of Oregon Letter to Board of Directors - Fairness Opinion at any time, if needed. Just select the essential kind to acquire or printing the papers format.

Use US Legal Forms, probably the most comprehensive variety of authorized kinds, to conserve time and avoid errors. The assistance gives expertly produced authorized papers layouts which you can use for an array of functions. Make your account on US Legal Forms and commence making your lifestyle a little easier.