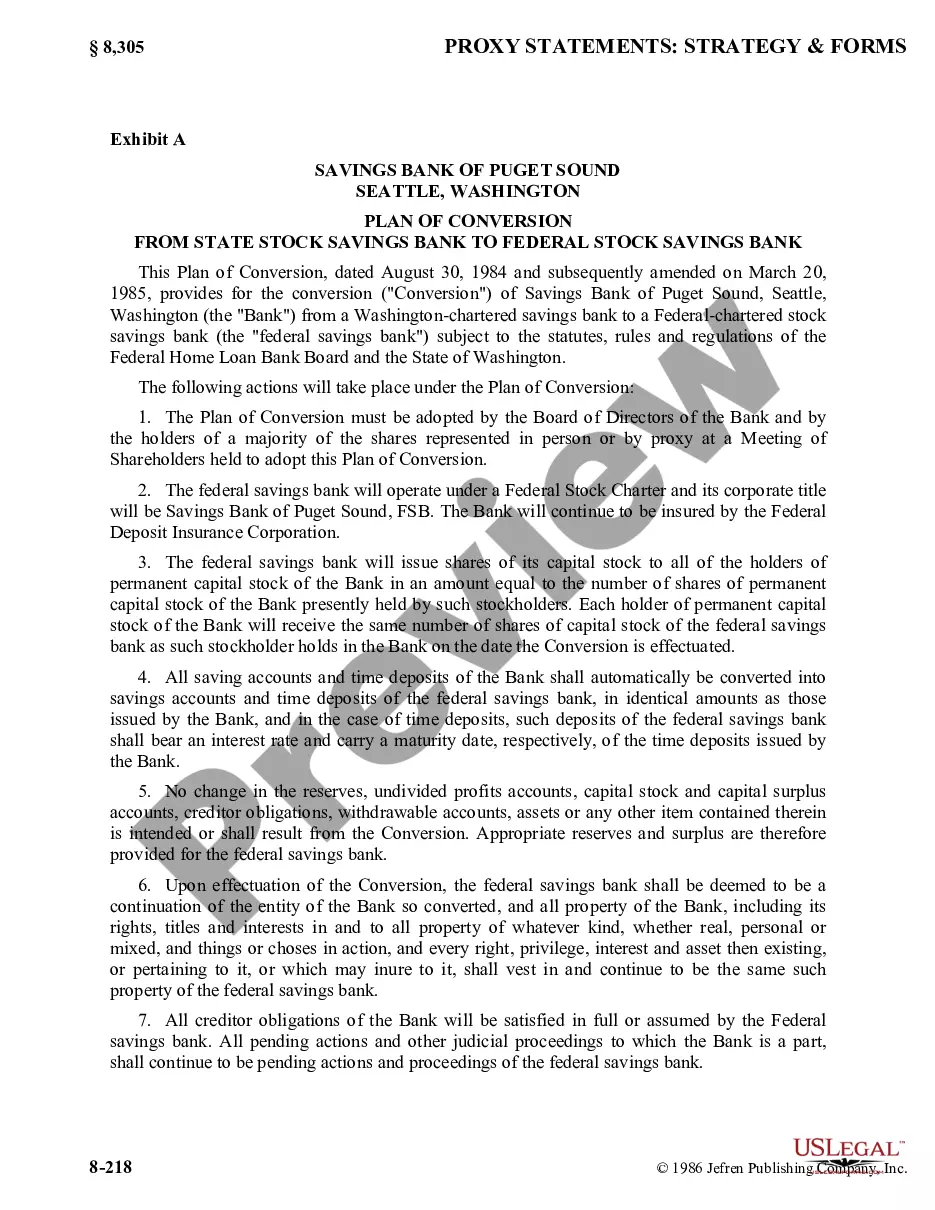

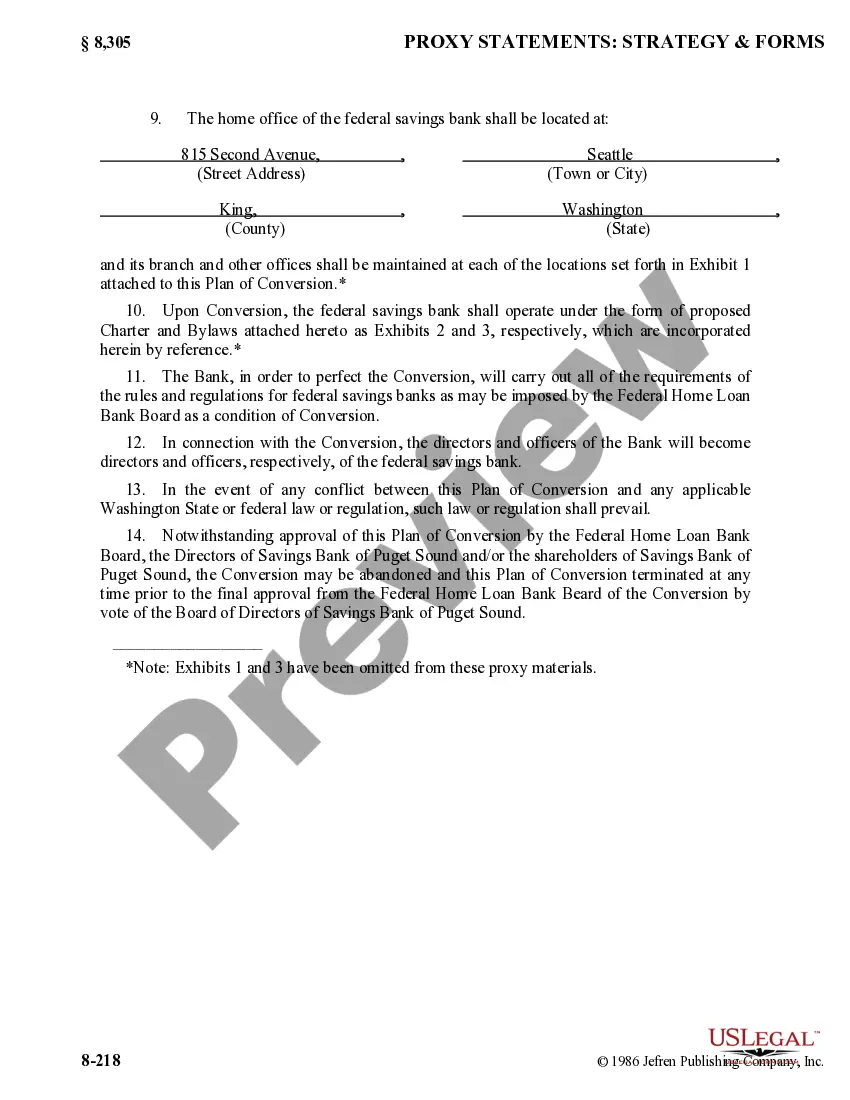

Title: The Oregon Plan of Conversion from State Stock Savings Bank to Federal Stock Savings Bank: Explained Introduction: In the state of Oregon, the Plan of Conversion from a state stock savings bank to a federal stock savings bank involves a series of legal and operational steps undertaken by a financial institution. The primary objective is to convert the bank's status, moving it from being regulated under state banking laws to federal banking laws. This comprehensive description aims to demystify the various aspects of the Oregon Plan of Conversion. Keywords: Oregon, Plan of Conversion, state stock savings bank, federal stock savings bank, banking laws, financial institution. Overview of the Oregon Plan of Conversion: The Oregon Plan of Conversion primarily revolves around the process of transitioning a state stock savings bank's regulatory authority from state-level oversight to federal-level oversight. This conversion is undertaken to enjoy the benefits and opportunities offered by federal banking laws and regulations, as well as to streamline operations and enhance competitiveness at a national level. Types of Oregon Plan of Conversion: 1. Voluntary Conversion: Under voluntary conversion, a state stock savings bank takes the initiative to convert its status to a federal stock savings bank. This type allows the bank to initiate the process, ensuring a smooth transition into federal jurisdiction while complying with regulatory requirements set forth by both state and federal authorities. Banks may opt for voluntary conversion to leverage federal programs, improve profitability, or strengthen market presence. 2. Involuntary Conversion: Involuntary conversions arise when a state stock savings bank's regulatory status is compulsorily converted to that of a federal stock savings bank. This can occur due to various reasons, including regulatory changes, mergers, acquisitions, legal obligations, or compliance issues. Involuntary conversions require the bank to conform to the prescribed conversion procedures, ensuring a seamless transition under the guidance of governing bodies. Key Steps Involved in the Oregon Plan of Conversion: 1. Identify the Need for Conversion: A state stock savings bank assesses various factors, such as market potential, business growth, regulatory advantages, and competitive positioning, to determine if a conversion is beneficial. 2. Prepare Conversion Plan: A comprehensive conversion plan is formulated, outlining the goals, strategies, and necessary legal and regulatory requirements for the conversion. 3. Approval and Notification Process: The bank seeks approval from appropriate regulatory bodies, Including the Oregon Department of Consumer and Business Services (DUBS) and the Office of the Comptroller of the Currency (OCC). All relevant stakeholders are notified about the proposed conversion. 4. Compliance and Due Diligence: The bank ensures adherence to all state and federal regulations, may conduct external audits, and provides documentation and financial information to support the conversion process. 5. Transfer of Assets and Liabilities: The bank transfers all assets and liabilities to the new federal stock savings bank. This process requires meticulous planning and coordination to minimize disruptions and ensure customer satisfaction. 6. Customer Awareness and Communication: Recognizing the importance of customer relationships, the bank educates its customers about the conversion, addresses concerns, and provides guidance to ensure a seamless transition. Conclusion: The Oregon Plan of Conversion from state stock savings bank to federal stock savings bank offers financial institutions an opportunity to transition into a different regulatory framework, leveraging the benefits and opportunities afforded by federal banking laws. The voluntary and involuntary conversion types provide banks with different pathways to achieving their strategic objectives. Successful execution of the conversion process requires meticulous planning, regulatory compliance, effective communication, and utmost dedication to customer satisfaction.

Oregon Plan of Conversion from state stock savings bank to federal stock savings bank

Description

How to fill out Oregon Plan Of Conversion From State Stock Savings Bank To Federal Stock Savings Bank?

US Legal Forms - one of several most significant libraries of authorized varieties in the USA - offers a wide array of authorized record templates you are able to down load or produce. Using the website, you will get a huge number of varieties for business and personal functions, sorted by groups, says, or keywords.You will find the newest versions of varieties just like the Oregon Plan of Conversion from state stock savings bank to federal stock savings bank in seconds.

If you already possess a membership, log in and down load Oregon Plan of Conversion from state stock savings bank to federal stock savings bank through the US Legal Forms catalogue. The Download button will show up on every single develop you see. You have accessibility to all in the past saved varieties inside the My Forms tab of your respective bank account.

In order to use US Legal Forms the first time, listed here are basic directions to help you get started out:

- Be sure you have picked out the right develop to your town/area. Click the Review button to check the form`s content material. Look at the develop explanation to actually have chosen the right develop.

- When the develop doesn`t fit your needs, utilize the Search field near the top of the display to find the one who does.

- When you are happy with the form, validate your decision by clicking the Acquire now button. Then, opt for the pricing plan you favor and give your qualifications to register to have an bank account.

- Process the deal. Make use of your Visa or Mastercard or PayPal bank account to accomplish the deal.

- Pick the file format and down load the form on your system.

- Make changes. Load, revise and produce and sign the saved Oregon Plan of Conversion from state stock savings bank to federal stock savings bank.

Each and every web template you added to your account lacks an expiry day and is also the one you have for a long time. So, if you wish to down load or produce another backup, just visit the My Forms area and click on in the develop you want.

Get access to the Oregon Plan of Conversion from state stock savings bank to federal stock savings bank with US Legal Forms, one of the most considerable catalogue of authorized record templates. Use a huge number of professional and express-specific templates that fulfill your company or personal needs and needs.