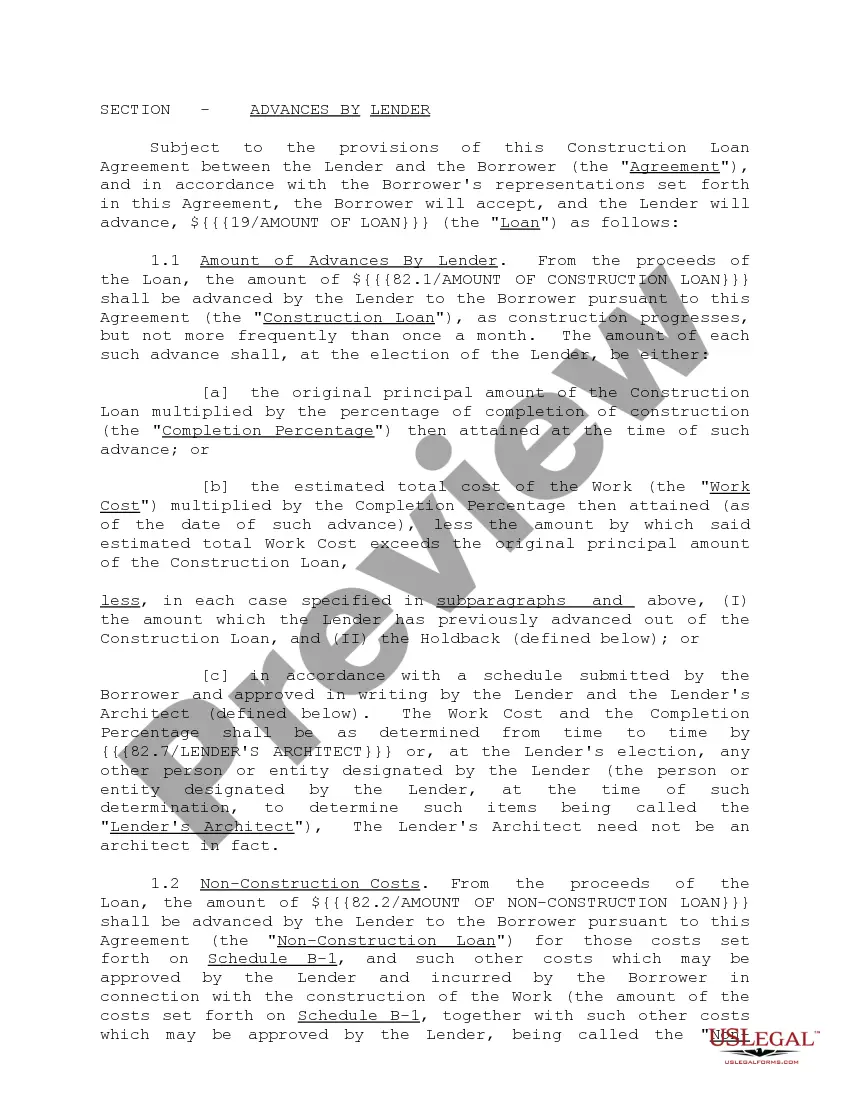

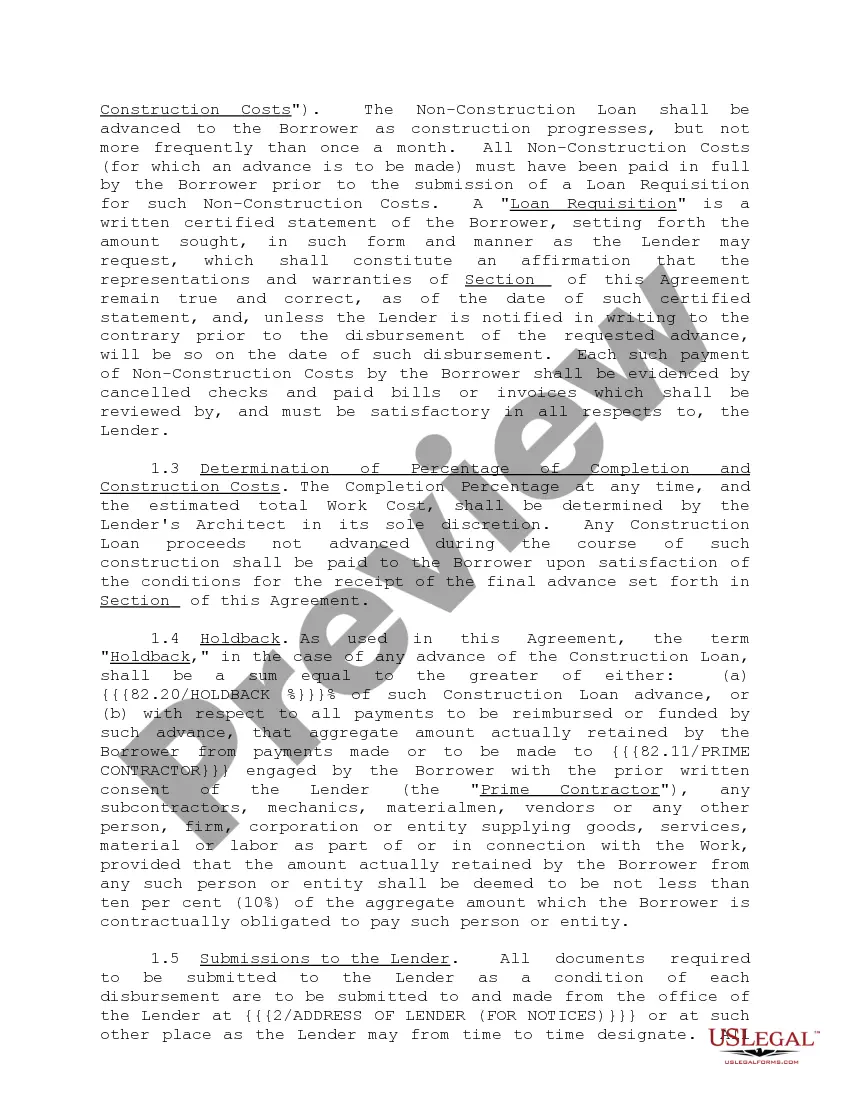

"Construction Loan Agreements and Variations" is a American Lawyer Media form. This form is to be used as a construction loan agreement.

Oregon Construction Loan Agreements and Variations: Explained Construction loan agreements serve as valuable tools for individuals and businesses looking to fund their construction projects in Oregon. These loan agreements provide the necessary financial resources to cover the costs of construction, including land acquisition, materials, labor, and other project-related expenses. In Oregon, construction loan agreements can take various forms, each tailored to meet the unique needs and requirements of different construction projects. Here are some key variations or types of Oregon construction loan agreements: 1. Construction-to-Permanent Loan: Also known as a "single-close loan," this construction loan agreement combines both the construction financing and permanent mortgage into a single loan, simplifying the process for the borrower. Once the construction phase is complete, the loan seamlessly converts into a regular mortgage. 2. Stand-Alone Construction Loan: This type of loan agreement is ideal for borrowers who already have a mortgage on the property and require separate financing for construction. The stand-alone construction loan allows borrowers to fund their construction project without affecting the existing mortgage. 3. Owner-Builder Construction Loan: Oregon also offers construction loan agreements specifically designed for individuals or entities acting as their own general contractors or builders. This option allows owner-builders to secure financing for both the land acquisition and the construction costs. 4. Bridge Loan: Bridge loans, also referred to as "interim financing," are short-term loans used to bridge the gap between the completion of a construction project and the long-term financing, like a permanent mortgage. This type of loan agreement is helpful when immediate funds are required to complete the construction while awaiting permanent financing. Each of these construction loan variations in Oregon considers different needs, timelines, and project arrangements. It is crucial for borrowers to clearly understand the terms, conditions, and repayment schedules associated with their chosen loan agreement. Consulting with lenders, financial experts, or legal professionals experienced in construction loan agreements can provide essential guidance in navigating the complexities of these loan arrangements. Oregon's construction loan agreements typically involve specific terms and conditions related to the disbursement of funds, potential penalties for delays or defaults, and mechanisms ensuring the completion of the project. These agreements require a thorough assessment of the construction project's viability, including detailed plans, cost estimates, and a comprehensive outline of construction stages. The construction loan agreements in Oregon play a vital role in making construction projects feasible by providing the necessary capital during various stages of the construction process. As with any financial agreement, it is crucial for borrowers to review and understand the terms, conditions, and legal obligations defined within the loan agreements to ensure successful project completion while mitigating potential risks and challenges.Oregon Construction Loan Agreements and Variations: Explained Construction loan agreements serve as valuable tools for individuals and businesses looking to fund their construction projects in Oregon. These loan agreements provide the necessary financial resources to cover the costs of construction, including land acquisition, materials, labor, and other project-related expenses. In Oregon, construction loan agreements can take various forms, each tailored to meet the unique needs and requirements of different construction projects. Here are some key variations or types of Oregon construction loan agreements: 1. Construction-to-Permanent Loan: Also known as a "single-close loan," this construction loan agreement combines both the construction financing and permanent mortgage into a single loan, simplifying the process for the borrower. Once the construction phase is complete, the loan seamlessly converts into a regular mortgage. 2. Stand-Alone Construction Loan: This type of loan agreement is ideal for borrowers who already have a mortgage on the property and require separate financing for construction. The stand-alone construction loan allows borrowers to fund their construction project without affecting the existing mortgage. 3. Owner-Builder Construction Loan: Oregon also offers construction loan agreements specifically designed for individuals or entities acting as their own general contractors or builders. This option allows owner-builders to secure financing for both the land acquisition and the construction costs. 4. Bridge Loan: Bridge loans, also referred to as "interim financing," are short-term loans used to bridge the gap between the completion of a construction project and the long-term financing, like a permanent mortgage. This type of loan agreement is helpful when immediate funds are required to complete the construction while awaiting permanent financing. Each of these construction loan variations in Oregon considers different needs, timelines, and project arrangements. It is crucial for borrowers to clearly understand the terms, conditions, and repayment schedules associated with their chosen loan agreement. Consulting with lenders, financial experts, or legal professionals experienced in construction loan agreements can provide essential guidance in navigating the complexities of these loan arrangements. Oregon's construction loan agreements typically involve specific terms and conditions related to the disbursement of funds, potential penalties for delays or defaults, and mechanisms ensuring the completion of the project. These agreements require a thorough assessment of the construction project's viability, including detailed plans, cost estimates, and a comprehensive outline of construction stages. The construction loan agreements in Oregon play a vital role in making construction projects feasible by providing the necessary capital during various stages of the construction process. As with any financial agreement, it is crucial for borrowers to review and understand the terms, conditions, and legal obligations defined within the loan agreements to ensure successful project completion while mitigating potential risks and challenges.