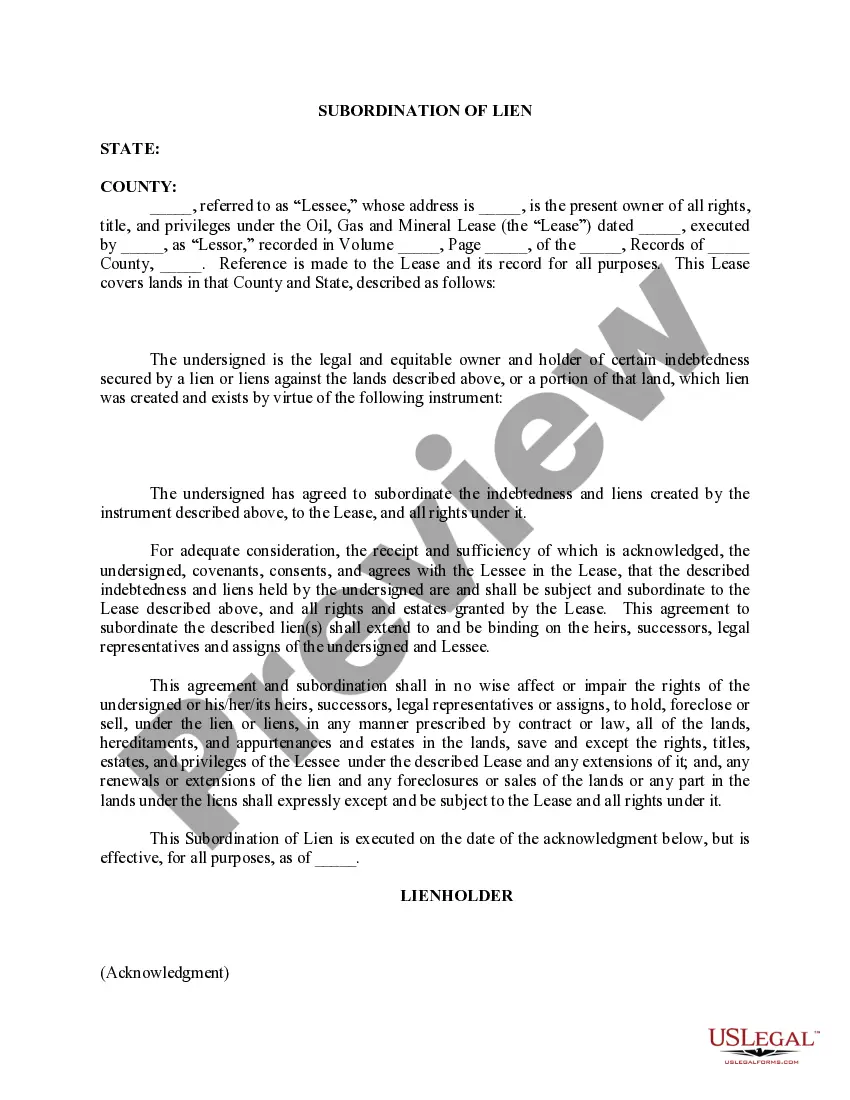

Oregon Subordination of Lien refers to a legal process that allows a creditor to agree to a lower priority position in their lien rights against a property or asset. This agreement is often made to enable the property owner to obtain additional financing or refinancing, while still protecting the interests of the existing lien holders. Subordination of lien is a common practice in real estate transactions and is regulated by specific laws and regulations in Oregon. There are two primary types of Oregon Subordination of Lien: 1. Voluntary Subordination: Voluntary subordination occurs when a lien holder willingly agrees to subordinate their lien position to another creditor. This enables the property owner to secure a new loan or mortgage that will take priority over the existing lien. By voluntarily subordinating their lien, the creditor accepts a secondary position and acknowledges that in the event of default or foreclosure, the new loan will be paid off first, and only then will they receive their share of the proceeds. 2. Involuntary Subordination: Involuntary subordination, also known as "equitable subordination," happens when a court enforces the subordination of lien against the wishes of the creditor. This type of subordination typically occurs in cases of fraud, misrepresentation, or when it is in the best interest of fairness and justice. For example, if a creditor has engaged in unethical practices or holds an invalid or unenforceable lien, the court may order an involuntary subordination, protecting the rights of other lien holders or securing the borrower's best interest. It is important to note that the terms and conditions of subordination agreements may vary depending on the specific circumstances of each case. Parties involved in a subordination agreement should consult legal professionals to ensure compliance with Oregon laws and the protection of their rights and interests. Oregon Subordination of Lien can be a complex legal process, and it is crucial to understand its implications before entering into any agreements. By effectively utilizing this legal mechanism, property owners can unlock additional financing options while still maintaining the rights of existing lien holders.

Oregon Subordination of Lien

Description

How to fill out Oregon Subordination Of Lien?

Are you presently in the position in which you require files for both organization or specific purposes just about every day? There are a lot of authorized papers web templates available online, but locating kinds you can trust isn`t easy. US Legal Forms gives a large number of form web templates, much like the Oregon Subordination of Lien, which are created to fulfill federal and state requirements.

When you are currently familiar with US Legal Forms website and have your account, basically log in. Following that, you may acquire the Oregon Subordination of Lien template.

If you do not offer an accounts and want to begin to use US Legal Forms, follow these steps:

- Find the form you will need and make sure it is for that proper area/area.

- Utilize the Preview option to check the shape.

- See the outline to actually have selected the correct form.

- In the event the form isn`t what you are seeking, utilize the Search industry to discover the form that meets your requirements and requirements.

- If you obtain the proper form, simply click Acquire now.

- Pick the prices plan you would like, fill in the necessary info to make your bank account, and pay for the order making use of your PayPal or Visa or Mastercard.

- Choose a practical paper formatting and acquire your duplicate.

Locate all the papers web templates you possess purchased in the My Forms menu. You can aquire a more duplicate of Oregon Subordination of Lien anytime, if possible. Just select the essential form to acquire or print the papers template.

Use US Legal Forms, probably the most extensive assortment of authorized types, to save lots of time and steer clear of mistakes. The service gives appropriately created authorized papers web templates which you can use for a selection of purposes. Produce your account on US Legal Forms and begin generating your life a little easier.