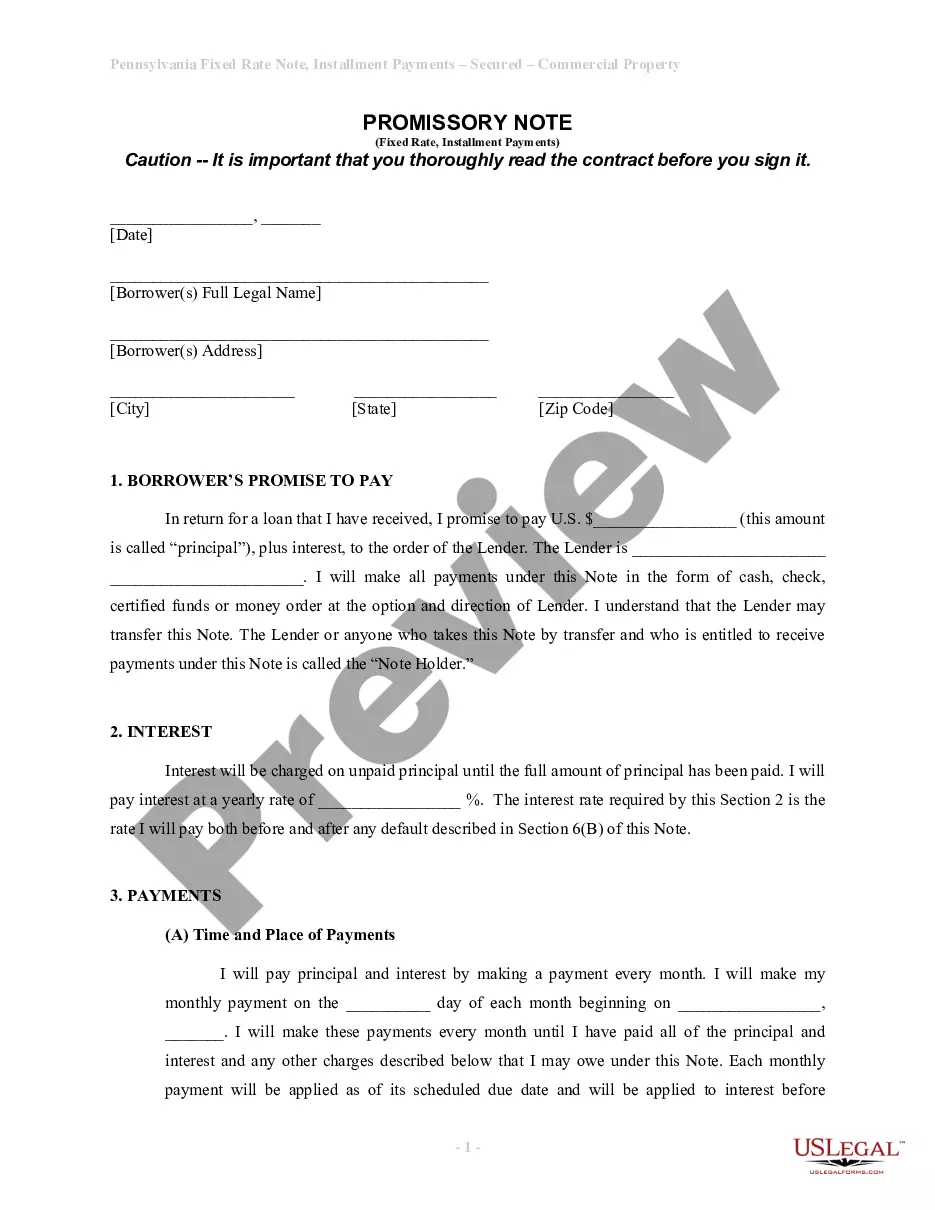

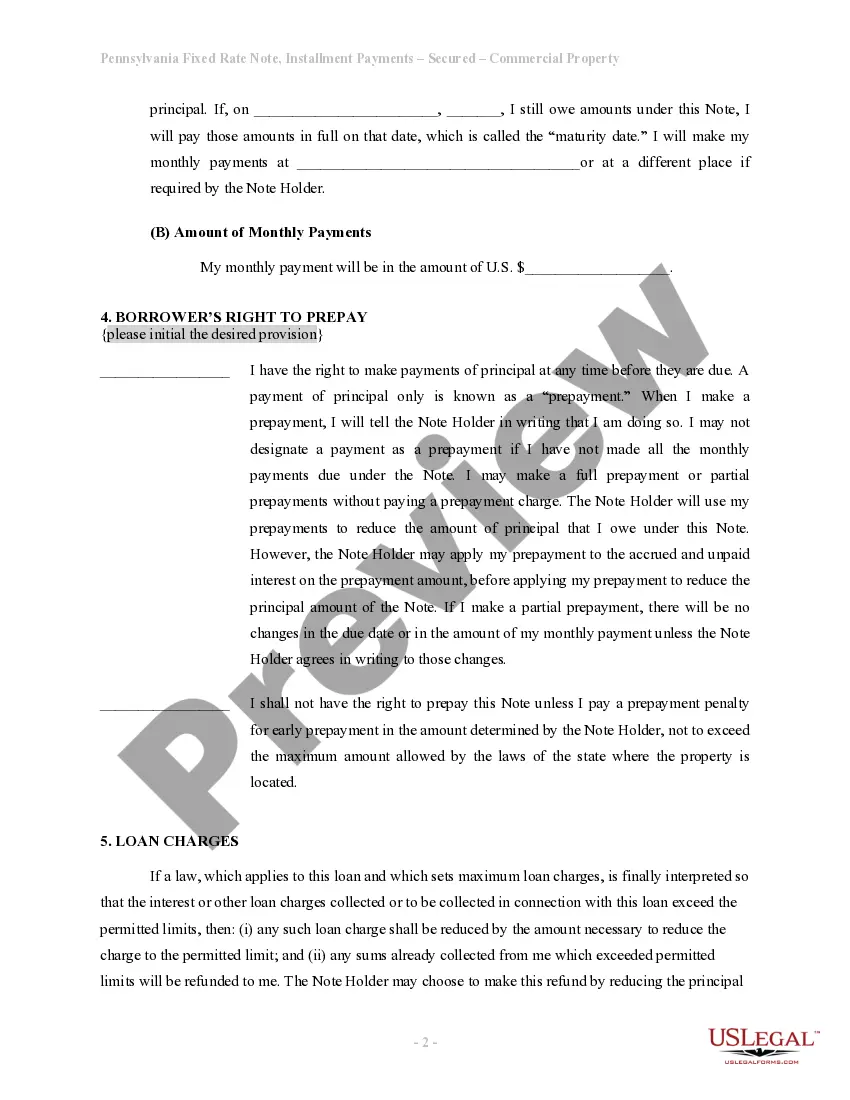

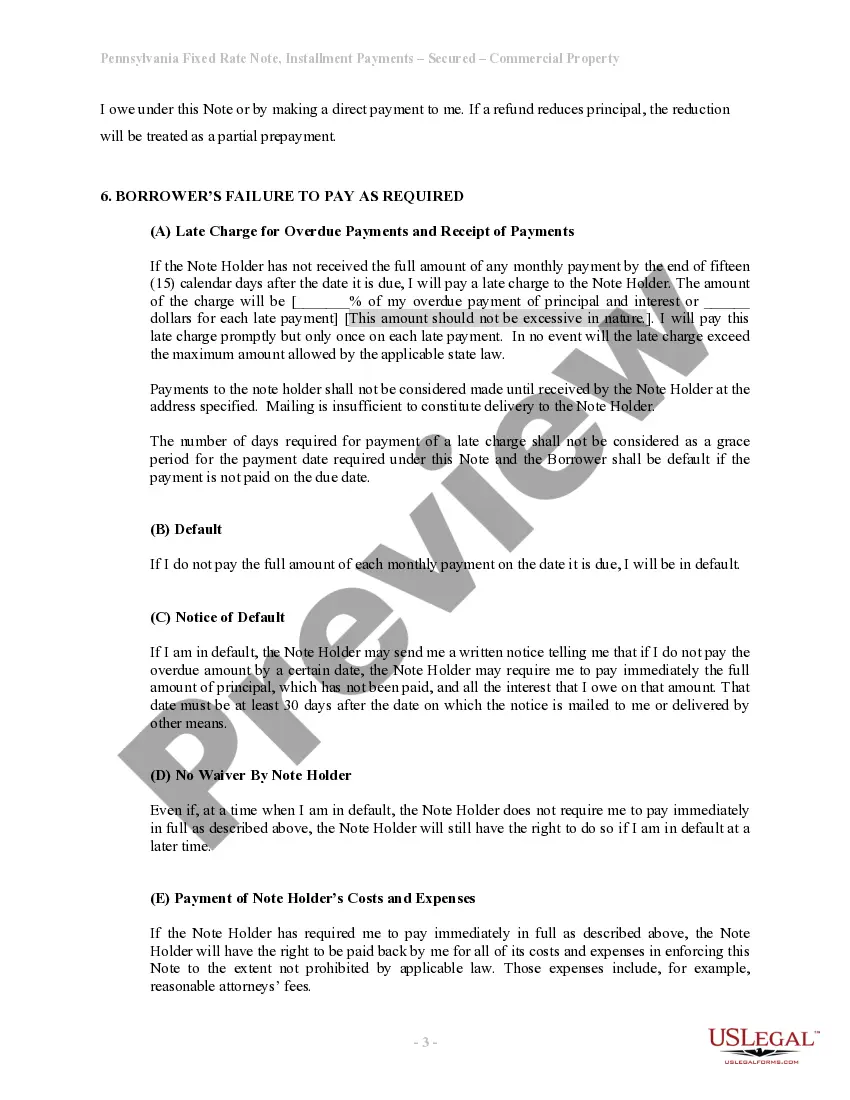

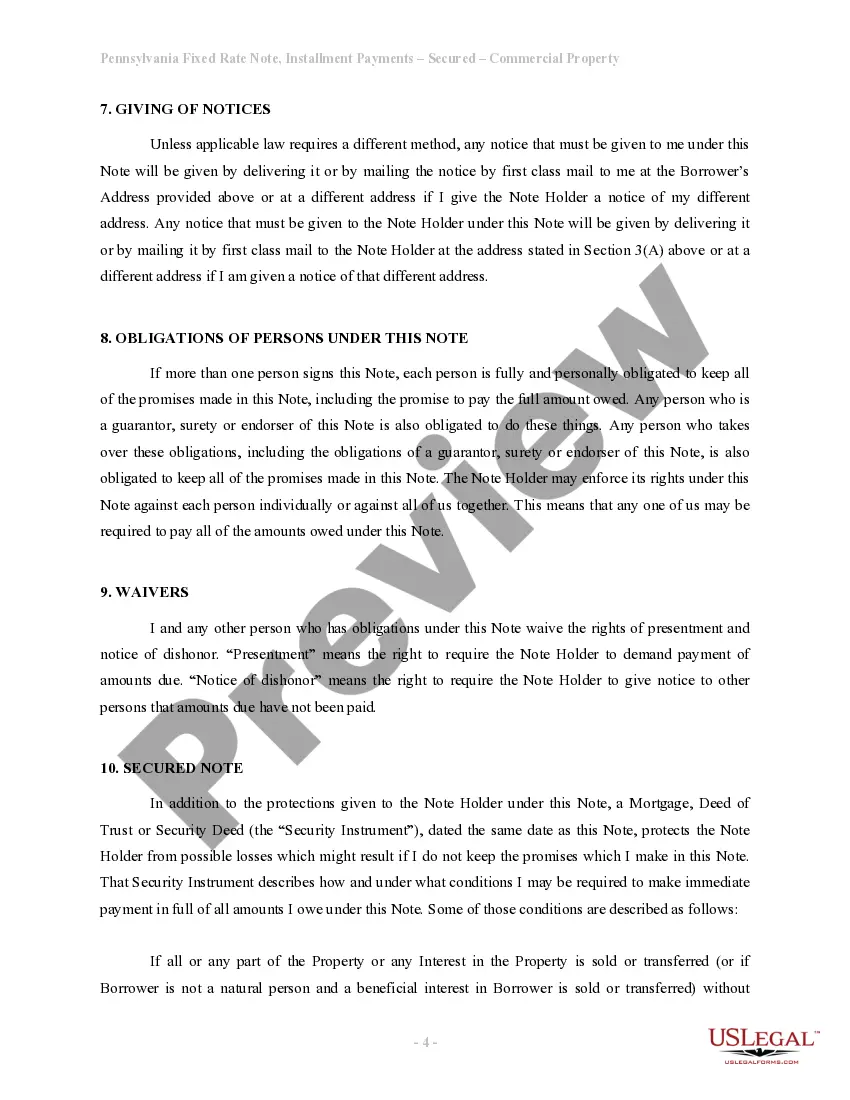

This is a form of Promissory Note for use where commercial property is security for the loan. A separate deed of trust or mortgage is also required.

Pennsylvania Installments Fixed Rate Promissory Note Secured by Commercial Real Estate

Category:

State:

Pennsylvania

Control #:

PA-NOTESEC3

Format:

Word;

Rich Text

Instant download

Description Installments Promissory Secured

Free preview Pennsylvania Rate Estate

How to fill out Promissory Commercial Estate?

The work with documents isn't the most simple process, especially for those who almost never work with legal paperwork. That's why we advise making use of correct Pennsylvania Installments Fixed Rate Promissory Note Secured by Commercial Real Estate samples created by skilled lawyers. It gives you the ability to stay away from troubles when in court or dealing with formal organizations. Find the documents you need on our website for top-quality forms and correct explanations.

If you’re a user having a US Legal Forms subscription, just log in your account. Once you’re in, the Download button will immediately appear on the template page. After accessing the sample, it will be stored in the My Forms menu.

Customers with no a subscription can quickly get an account. Look at this brief step-by-step help guide to get the Pennsylvania Installments Fixed Rate Promissory Note Secured by Commercial Real Estate:

- Ensure that file you found is eligible for use in the state it’s needed in.

- Verify the file. Use the Preview option or read its description (if available).

- Buy Now if this file is the thing you need or utilize the Search field to get another one.

- Select a convenient subscription and create your account.

- Utilize your PayPal or credit card to pay for the service.

- Download your file in a required format.

Right after completing these straightforward steps, it is possible to complete the form in a preferred editor. Double-check completed data and consider requesting a lawyer to examine your Pennsylvania Installments Fixed Rate Promissory Note Secured by Commercial Real Estate for correctness. With US Legal Forms, everything gets much simpler. Try it now!

Note Estate Form popularity

Installments Promissory Note Other Form Names

Promissory Note Estate

How To Write A Promise To Pay Letter

Promissory Real Estate

Fixed Promissory Purchase

Note Commercial Real

Rate Commercial Estate

Promise To Pay Rent Letter Sample

Rate Promissory Real FAQ

The individual who promises to pay is the maker, and the person to whom payment is promised is called the payee or holder. If signed by the maker, a promissory note is a negotiable instrument.

A secured promissory note is an obligation to pay that is secured by some type of property. This means that if the payor fails to pay, the payee can seize the designated property to obtain reimbursement of the loan.If the collateral is real property, there will be either a mortgage or a deed of trust.

What Is a Promissory Note? A promissory note is a financial instrument that contains a written promise by one party (the note's issuer or maker) to pay another party (the note's payee) a definite sum of money, either on demand or at a specified future date.

Promissory notes are legally binding whether the note is secured by collateral or based only on the promise of repayment. If you lend money to someone who defaults on a promissory note and does not repay, you can legally possess any property that individual promised as collateral.

When a loan changes hands, the promissory note is endorsed (signed over) to the new owner of the loan. In some cases, the note is endorsed in blank which makes it a bearer instrument under Article 3 of the Uniform Commercial Code. So, any party that possesses the note has the legal authority to enforce it.

Promissory notes are a valuable legal tool that any individual can use to legally bind another individual to an agreement for purchasing goods or borrowing money. A well-executed promissory note has the full effect of law behind it and is legally binding on both parties.

The lender holds the promissory note while the loan is being repaid, then the note is marked as paid and returned to the borrower when the loan is satisfied. Promissory notes aren't the same as mortgages, but the two often go hand in hand when someone is buying a home.

Unlike a mortgage or deed of trust, the promissory note isn't recorded in the county land records. The lender holds the promissory note while the loan is outstanding. When the loan is paid off, the note is marked as "paid in full" and returned to the borrower.

A promissory note can be secured with a pledge of collateral, which is something of value that can be seized if a borrower defaults.