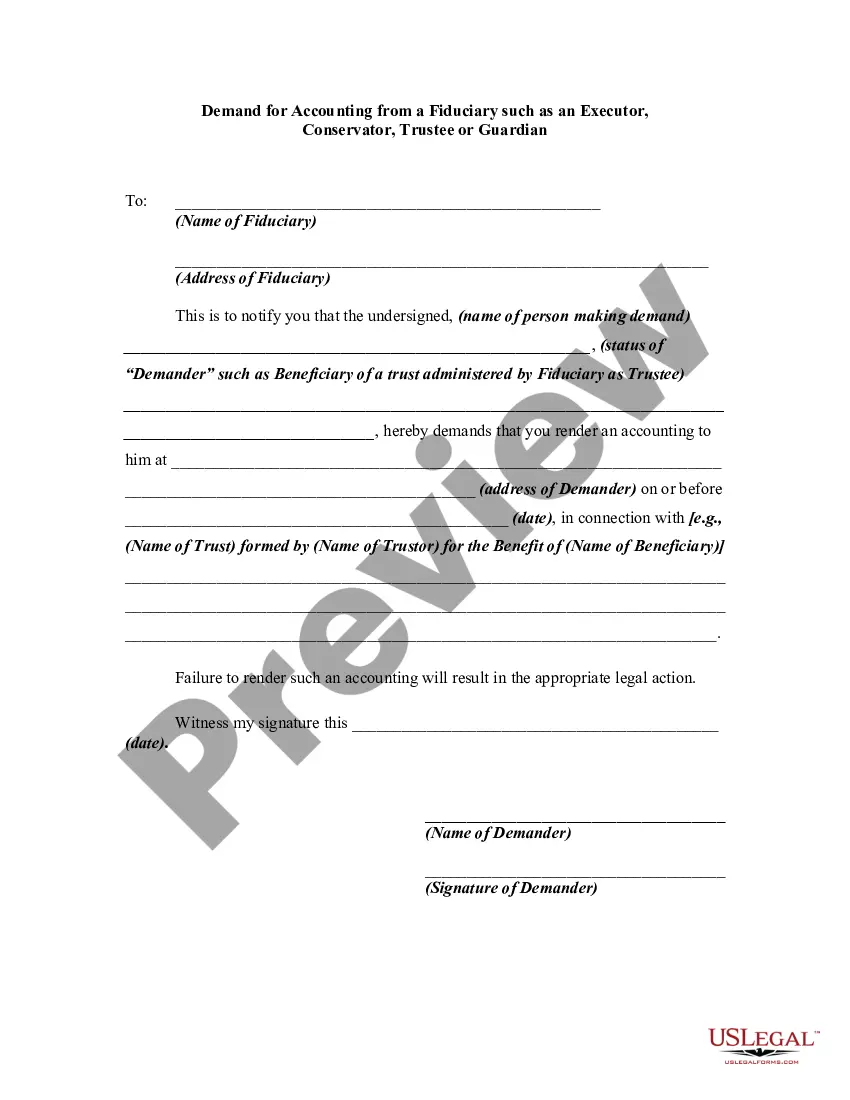

An accounting by a fiduciary usually involves an inventory of assets, debts, income, expenditures, and other items, which is submitted to a court. Such an accounting is used in various contexts, such as administration of a trust, estate, guardianship or conservatorship. Generally, a prior demand by an appropriate party for an accounting, and a refusal by the fiduciary to account, are conditions precedent to the bringing of an action for an accounting.

Title: Pennsylvania Demand for Accounting from a Fiduciary: Understanding Executor, Conservator, Trustee, and Legal Guardian Responsibilities Introduction: In Pennsylvania, a Demand for Accounting from a Fiduciary is an essential tool to ensure transparency and accountability within various fiduciary roles, including that of an Executor, Conservator, Trustee, or Legal Guardian. This article aims to provide a detailed description of these roles and the importance of demanding accounting from fiduciaries to protect the interests of beneficiaries. I. Executor Demand for Accounting: In the context of estate administration, an Executor is a person appointed to manage and distribute the assets of a deceased individual's estate. Executors have a duty to act in the best interests of the estate beneficiaries and are required to provide an accurate and comprehensive accounting of the estate's financial transactions, including assets, debts, income, expenses, distributions, and any accompanying documentation. Beneficiaries can demand accounting from the Executor to ensure the executor is fulfilling their fiduciary duties. II. Conservator Demand for Accounting: A Conservator is a court-appointed individual responsible for managing the affairs and assets of a person deemed unable to care for themselves, commonly referred to as a ward. A Conservator must keep detailed records of all financial transactions and provide periodic reports to the court regarding the ward's assets, income, expenses, and other relevant information. Interested parties, such as family members or representatives of the ward, may file a Demand for Accounting to assess the Conservator's financial management. III. Trustee Demand for Accounting: Trustees are entrusted with administering trusts, which hold assets for the benefit of designated beneficiaries. Trustees are obligated to act in the best interests of beneficiaries and must provide transparent, accurate, and regular accounting of the trust's financial activities. A Demand for Accounting from a Trustee allows beneficiaries to review the financial records and ensure the Trustee fulfills their fiduciary duties. IV. Legal Guardian Demand for Accounting: Legal Guardians are appointed by the court to make decisions for individuals who are unable to manage their personal or financial affairs, often referred to as wards. Guardians must maintain detailed records of all financial transactions pertaining to the ward and provide regular reports to the court, demonstrating the proper management of the ward's assets. Interested parties can demand accounting from the Legal Guardian to ensure the ward's financial well-being. Conclusion: In Pennsylvania, demanding accounting from fiduciaries such as Executors, Conservators, Trustees, or Legal Guardians is crucial to safeguard the interests of beneficiaries and wards. By utilizing the demand for accounting process, interested parties can ensure transparency, accountability, and fulfill their role as diligent overseers. It ensures that fiduciaries abide by their responsibilities and enhances the integrity of the estate administration, conservatorship, trust, and guardianship processes.

Title: Pennsylvania Demand for Accounting from a Fiduciary: Understanding Executor, Conservator, Trustee, and Legal Guardian Responsibilities Introduction: In Pennsylvania, a Demand for Accounting from a Fiduciary is an essential tool to ensure transparency and accountability within various fiduciary roles, including that of an Executor, Conservator, Trustee, or Legal Guardian. This article aims to provide a detailed description of these roles and the importance of demanding accounting from fiduciaries to protect the interests of beneficiaries. I. Executor Demand for Accounting: In the context of estate administration, an Executor is a person appointed to manage and distribute the assets of a deceased individual's estate. Executors have a duty to act in the best interests of the estate beneficiaries and are required to provide an accurate and comprehensive accounting of the estate's financial transactions, including assets, debts, income, expenses, distributions, and any accompanying documentation. Beneficiaries can demand accounting from the Executor to ensure the executor is fulfilling their fiduciary duties. II. Conservator Demand for Accounting: A Conservator is a court-appointed individual responsible for managing the affairs and assets of a person deemed unable to care for themselves, commonly referred to as a ward. A Conservator must keep detailed records of all financial transactions and provide periodic reports to the court regarding the ward's assets, income, expenses, and other relevant information. Interested parties, such as family members or representatives of the ward, may file a Demand for Accounting to assess the Conservator's financial management. III. Trustee Demand for Accounting: Trustees are entrusted with administering trusts, which hold assets for the benefit of designated beneficiaries. Trustees are obligated to act in the best interests of beneficiaries and must provide transparent, accurate, and regular accounting of the trust's financial activities. A Demand for Accounting from a Trustee allows beneficiaries to review the financial records and ensure the Trustee fulfills their fiduciary duties. IV. Legal Guardian Demand for Accounting: Legal Guardians are appointed by the court to make decisions for individuals who are unable to manage their personal or financial affairs, often referred to as wards. Guardians must maintain detailed records of all financial transactions pertaining to the ward and provide regular reports to the court, demonstrating the proper management of the ward's assets. Interested parties can demand accounting from the Legal Guardian to ensure the ward's financial well-being. Conclusion: In Pennsylvania, demanding accounting from fiduciaries such as Executors, Conservators, Trustees, or Legal Guardians is crucial to safeguard the interests of beneficiaries and wards. By utilizing the demand for accounting process, interested parties can ensure transparency, accountability, and fulfill their role as diligent overseers. It ensures that fiduciaries abide by their responsibilities and enhances the integrity of the estate administration, conservatorship, trust, and guardianship processes.