The Fair Credit Reporting Act (FCRA) is designed to help ensure that credit bureaus furnish correct and complete information to businesses to use when evaluating your application. Your rights include:

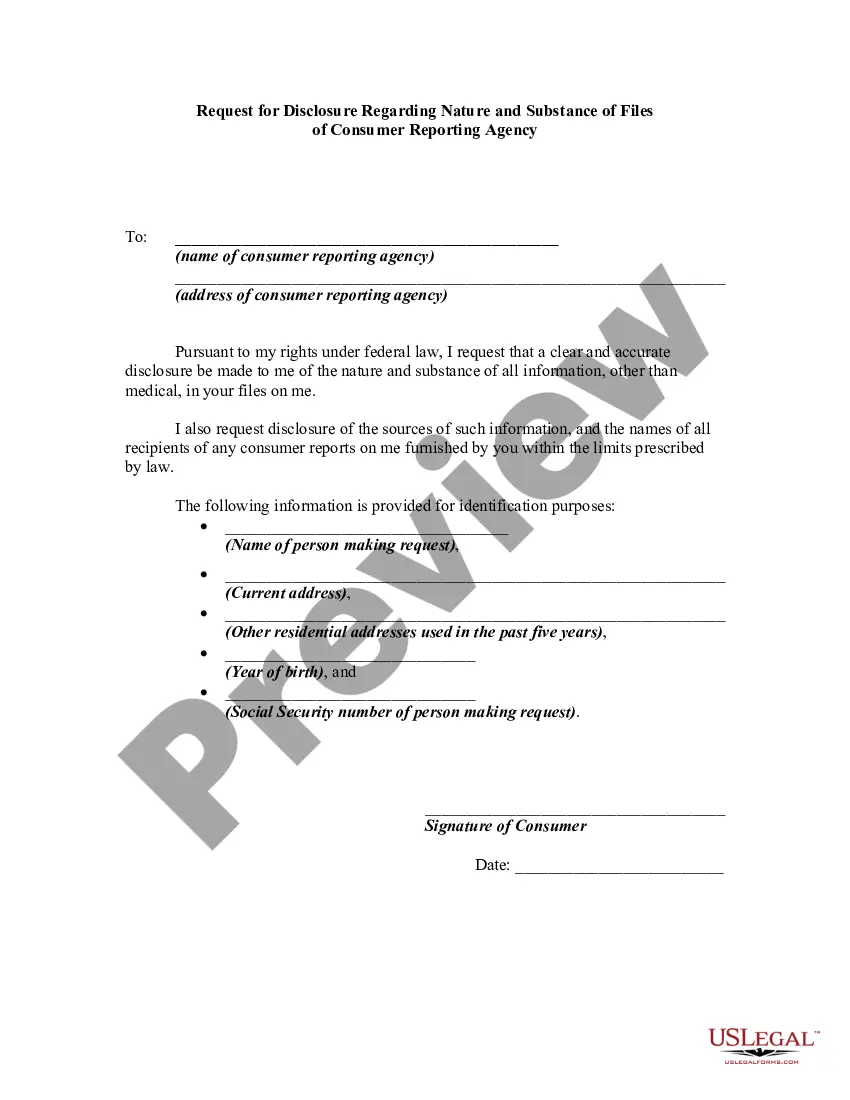

The right to receive a copy of your credit report. The copy of your report must contain all of the information in your file at the time of your request.

The right to know the name of anyone who received your credit report in the last year for most purposes or in the last two years for employment purposes.

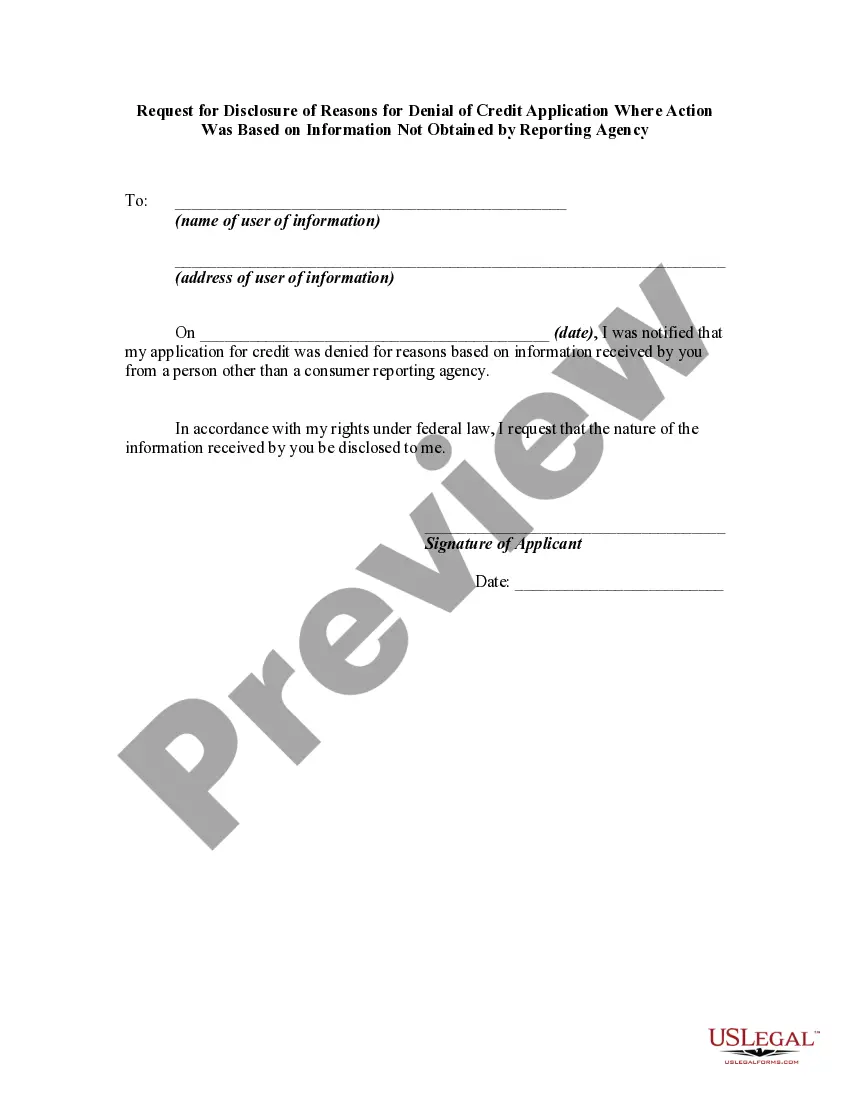

Any company that denies your application must supply the name and address of the credit bureau they contacted, provided the denial was based on information given by the credit bureau.

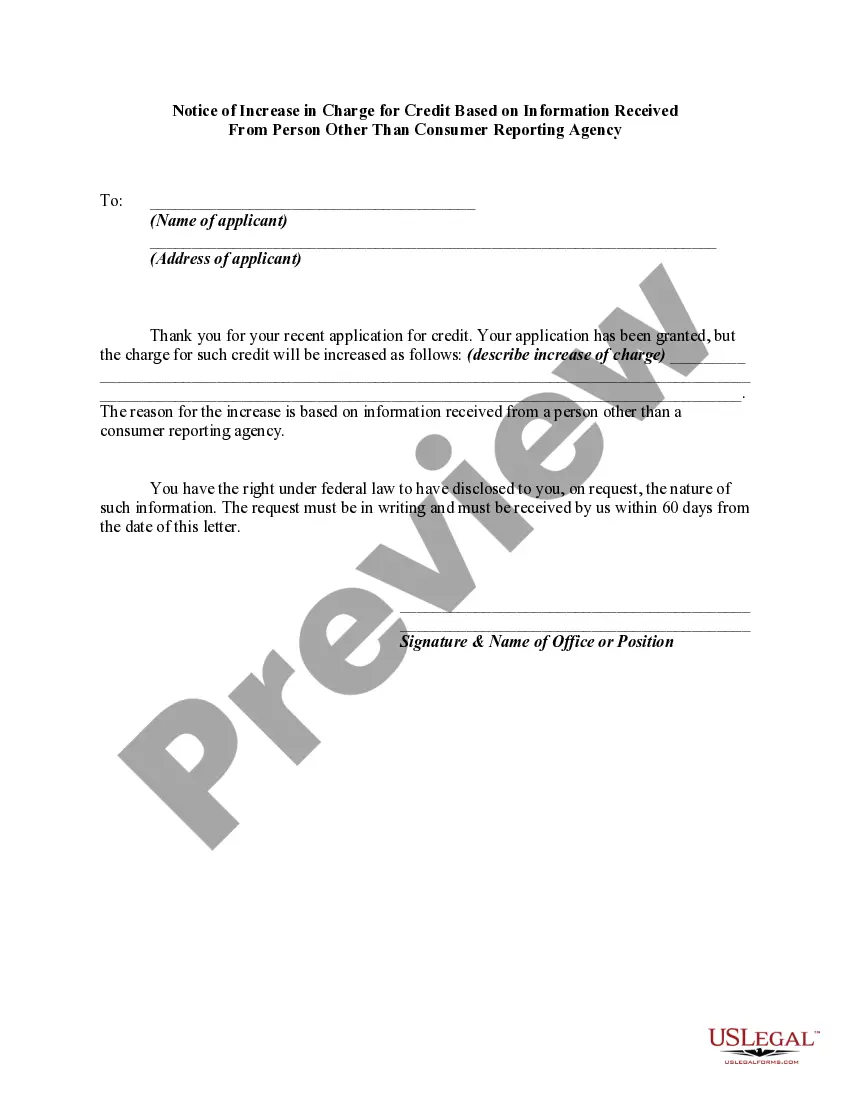

The right to a free copy of your credit report when your application is denied because of information supplied by the credit bureau. Your request must be made within 60 days of receiving your denial notice.

If you contest the completeness or accuracy of information in your report, you should file a dispute with the credit bureau and with the company that furnished the information to the bureau. Both the credit bureau and the furnisher of information are legally obligated to investigate your dispute.

A right to add a summary explanation to your credit report if your dispute is not resolved to your satisfaction.

Pennsylvania Request for Disclosure of Reasons for Increasing Charge for Credit Regarding Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency

Description

How to fill out Request For Disclosure Of Reasons For Increasing Charge For Credit Regarding Credit Application Where Action Was Based On Information Not Obtained By Reporting Agency?

If you have to full, obtain, or print out lawful document layouts, use US Legal Forms, the biggest assortment of lawful types, that can be found on-line. Make use of the site`s basic and practical look for to discover the files you require. Numerous layouts for enterprise and specific reasons are sorted by groups and says, or keywords. Use US Legal Forms to discover the Pennsylvania Request for Disclosure of Reasons for Increasing Charge for Credit Regarding Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency with a handful of mouse clicks.

Should you be presently a US Legal Forms buyer, log in to the bank account and click on the Download option to get the Pennsylvania Request for Disclosure of Reasons for Increasing Charge for Credit Regarding Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency. Also you can gain access to types you in the past saved from the My Forms tab of the bank account.

If you use US Legal Forms the first time, refer to the instructions beneath:

- Step 1. Make sure you have selected the form to the right city/land.

- Step 2. Utilize the Preview solution to look through the form`s information. Never neglect to read through the description.

- Step 3. Should you be unsatisfied using the form, use the Search industry at the top of the screen to discover other variations of the lawful form format.

- Step 4. Upon having identified the form you require, go through the Buy now option. Pick the costs plan you prefer and put your qualifications to register for an bank account.

- Step 5. Procedure the transaction. You can use your credit card or PayPal bank account to accomplish the transaction.

- Step 6. Pick the formatting of the lawful form and obtain it on your product.

- Step 7. Complete, change and print out or indication the Pennsylvania Request for Disclosure of Reasons for Increasing Charge for Credit Regarding Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency.

Each lawful document format you buy is yours permanently. You have acces to every single form you saved in your acccount. Click on the My Forms portion and decide on a form to print out or obtain once more.

Contend and obtain, and print out the Pennsylvania Request for Disclosure of Reasons for Increasing Charge for Credit Regarding Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency with US Legal Forms. There are many specialist and condition-certain types you may use for your personal enterprise or specific requires.

Form popularity

FAQ

The Act (Title VI of the Consumer Credit Protection Act) protects information collected by consumer reporting agencies such as credit bureaus, medical information companies and tenant screening services. Information in a consumer report cannot be provided to anyone who does not have a purpose specified in the Act.

The Fair Credit Reporting Act (FCRA) , 15 U.S.C. § 1681 et seq., governs access to consumer credit report records and promotes accuracy, fairness, and the privacy of personal information assembled by Credit Reporting Agencies (CRAs).

In addition, all consumers are entitled to one free disclosure every 12 months upon request from each nationwide credit bureau and from nationwide specialty consumer reporting agencies. See .consumerfinance.gov/learnmore for additional information. your credit-worthiness based on information from credit bureaus.

Consumer reporting agencies may not report outdated negative information. In most cases, a consumer reporting agency may not report negative information that is more than seven years old, or bankruptcies that are more than 10 years old. Access to your file is limited.

Common violations of the FCRA include: Failure to update reports after completion of bankruptcy is just one example. Agencies might also report old debts as new and report a financial account as active when it was closed by the consumer. Creditors give reporting agencies inaccurate financial information about you.

If a credit bureau's violations of the Fair Credit Reporting Act are deemed ?willful? (knowing or reckless) by a Court, consumers can recover damages ranging from $100 ? $1,000 for each violation of the FCRA.

Some examples of violations include: failing to report that a debt was discharged in bankruptcy. reporting old debts as new or re-aged. reporting an account as active when it was voluntarily closed by a consumer and.

Require that a consumer authorize the release of certain information. The bill would increase the consumers' control over when and how their reports are released, and it would require verification of a consumer's identity and the consumer's permission before releasing reports in certain instances.