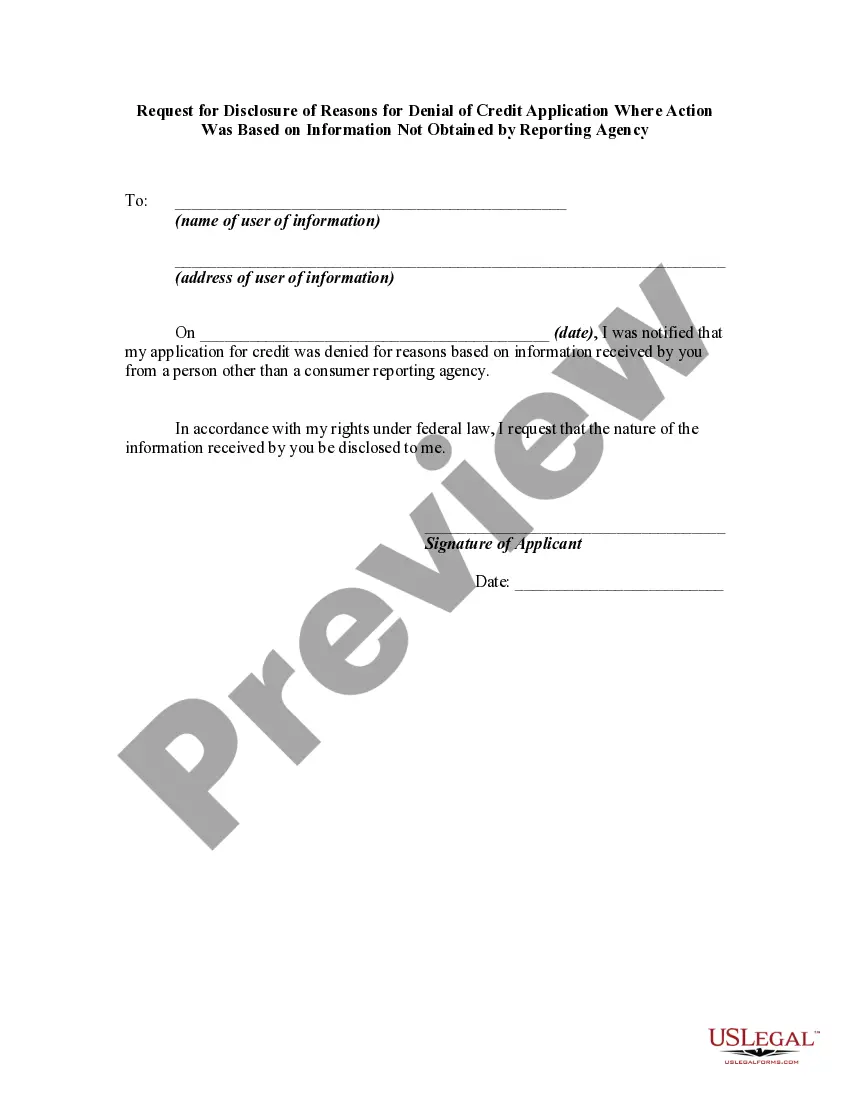

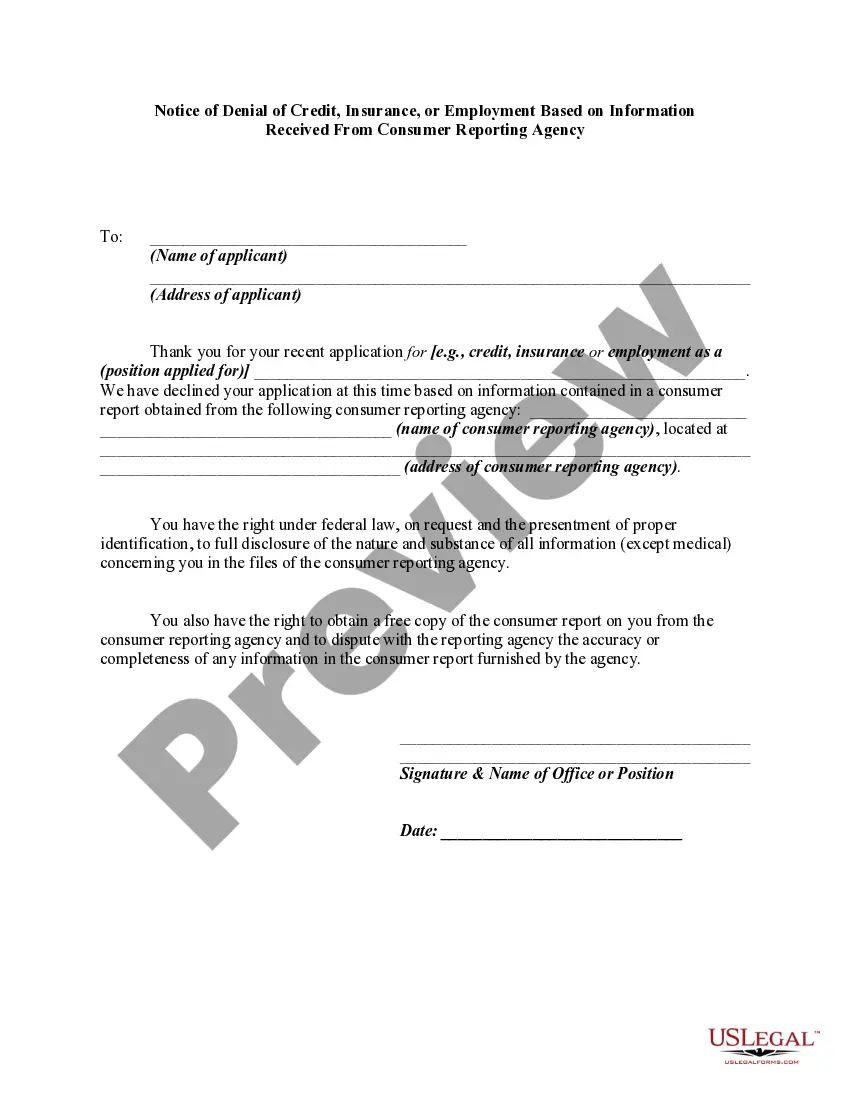

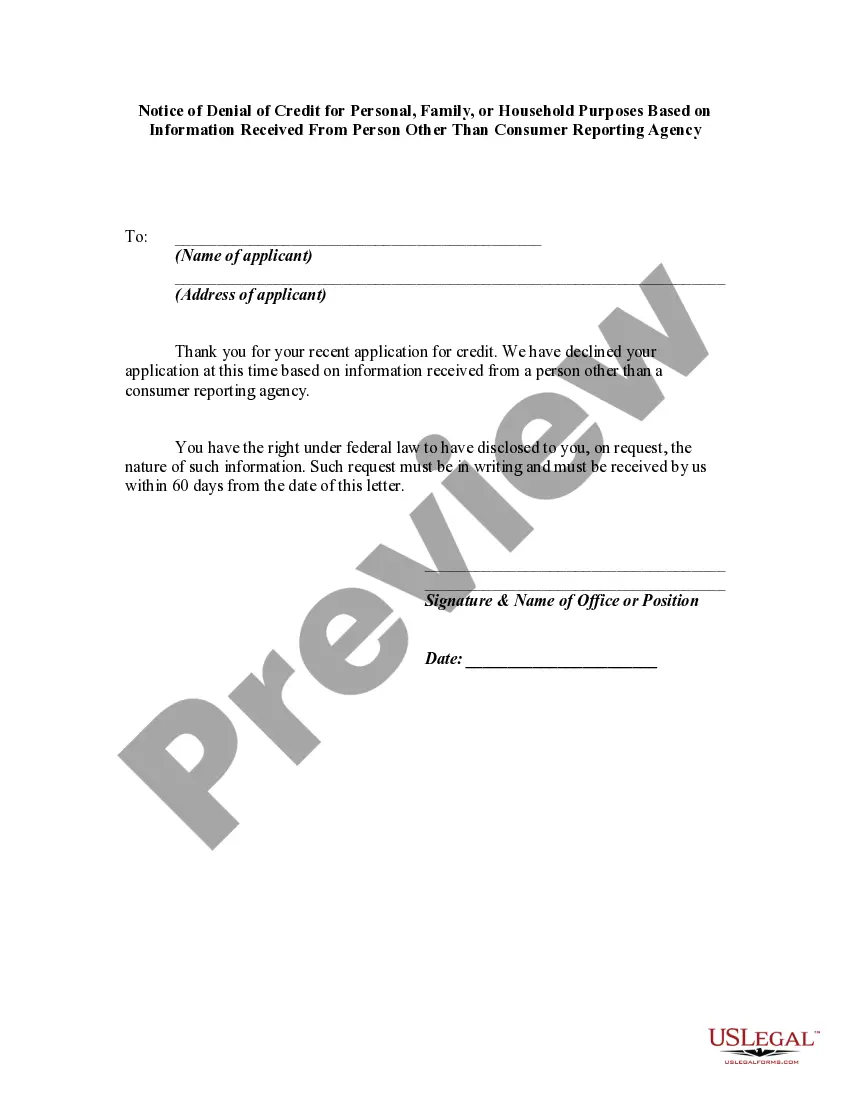

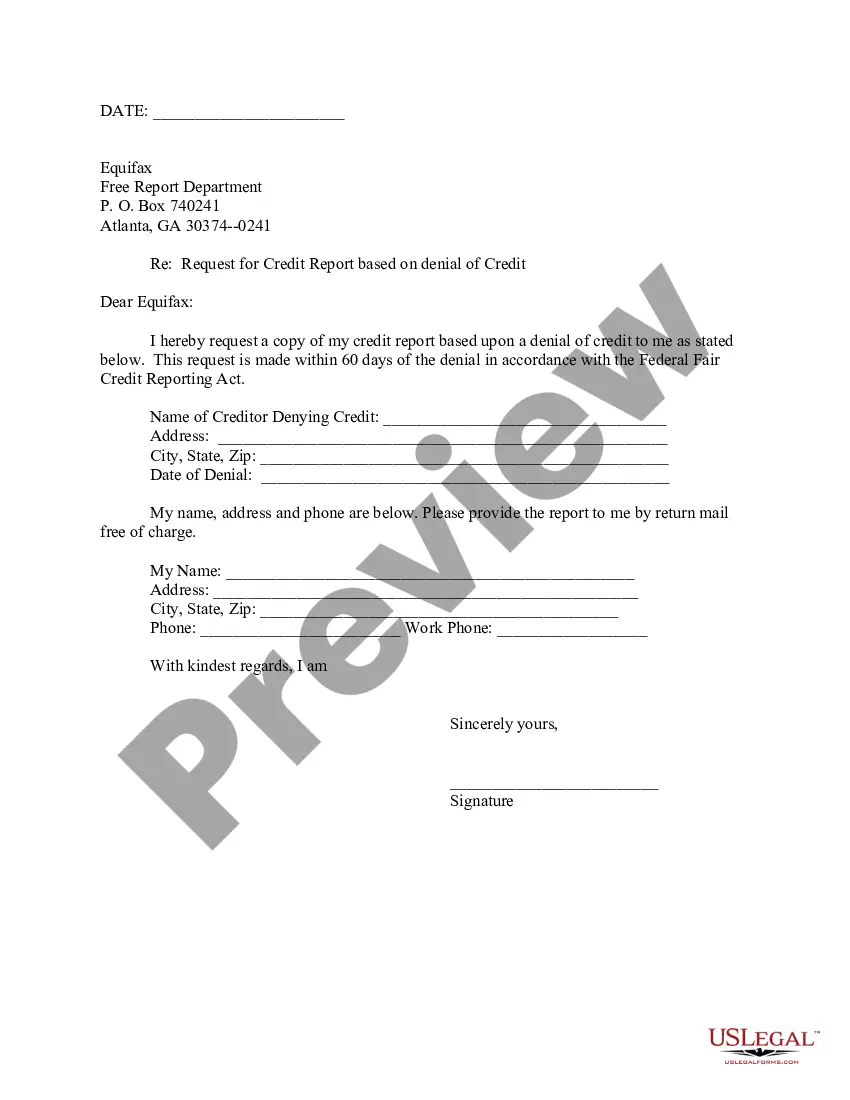

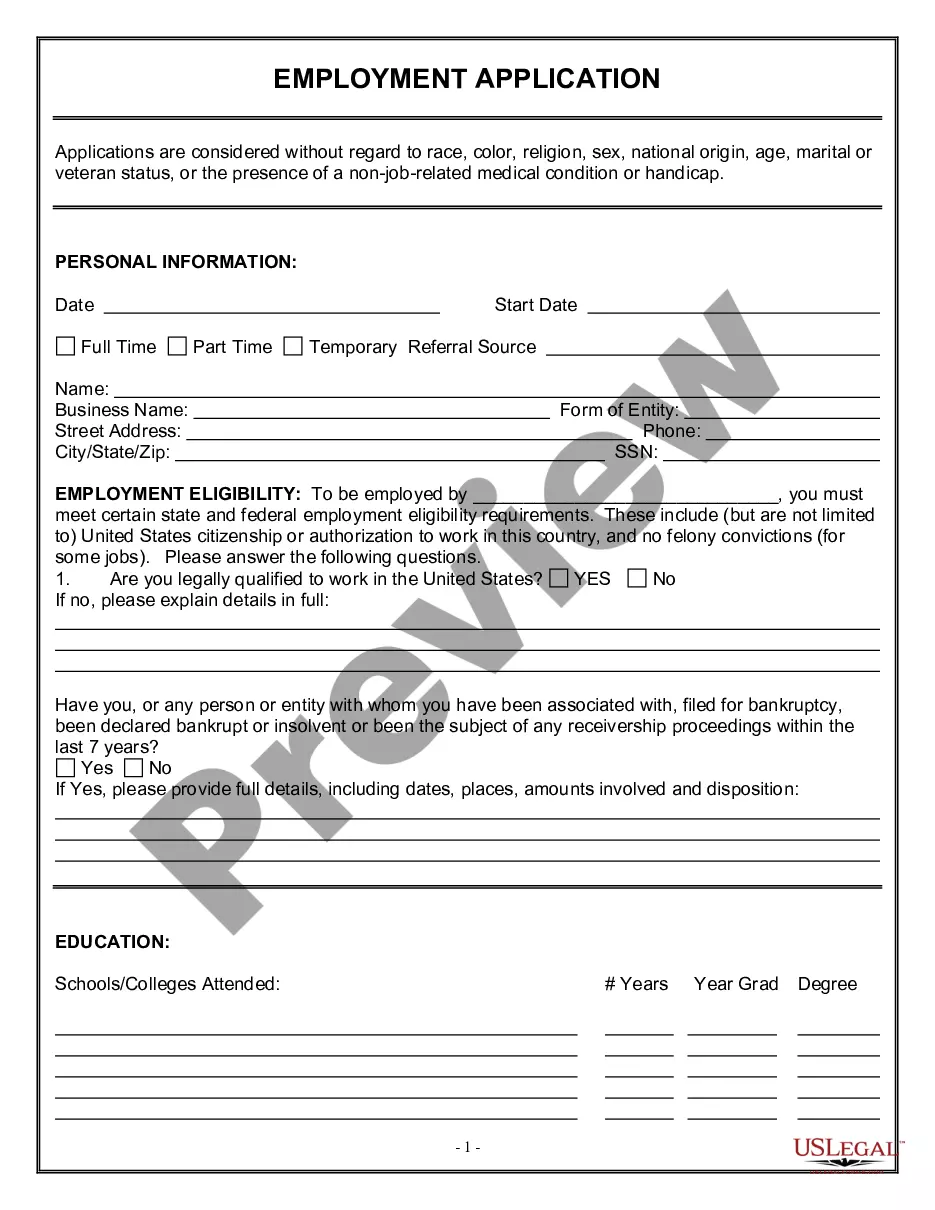

If a user of consumer reports takes any adverse action (such as denial of credit, insurance, or employment) with respect to any consumer that is based in whole or in part on any information contained in a consumer report, the Fair Credit Reporting Act requires that the user:

notify the consumer of the adverse action,

identify the consumer reporting agency making the report, and

notify the consumer of the consumer's right to obtain a free copy of a consumer report on the consumer from the consumer reporting agency and to dispute with the reporting agency the accuracy or completeness of any information in the consumer report furnished by the agency.

Under the federal Equal Credit Opportunity Act, a creditor must notify a consumer applicant for credit of the reasons for any adverse action taken on the application, and must make certain disclosures to the consumer concerning the applicant's rights and the provisions of federal law prohibiting discrimination in credit opportunities.