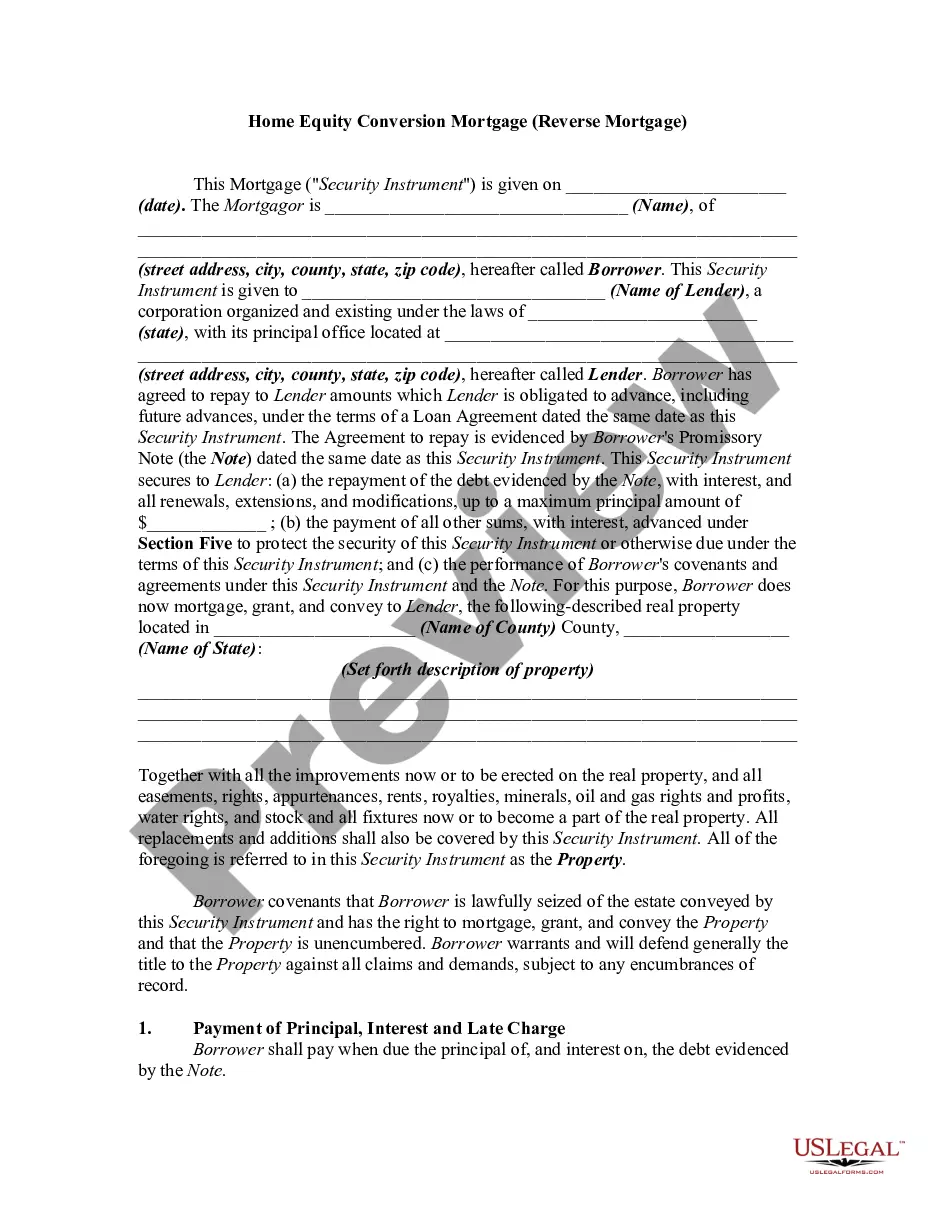

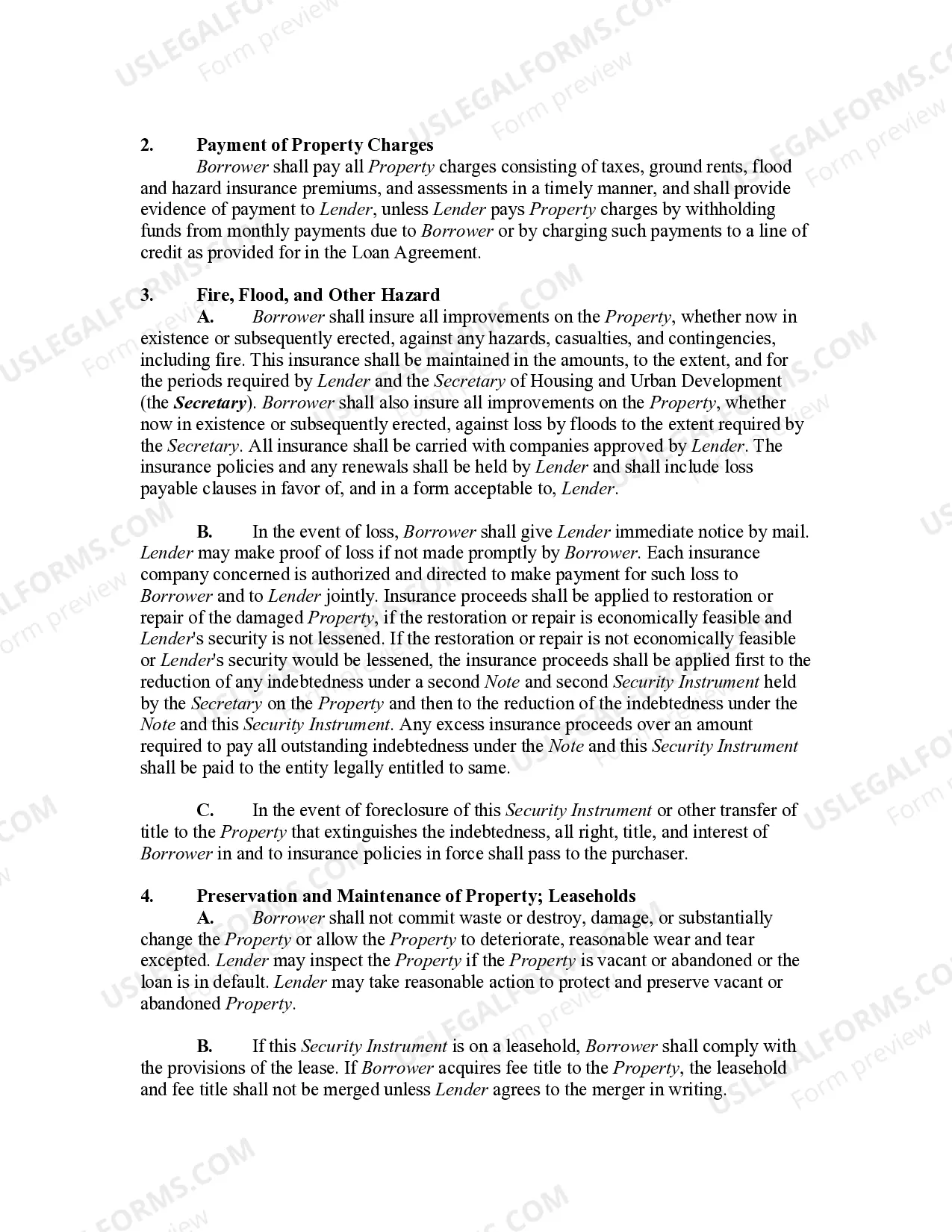

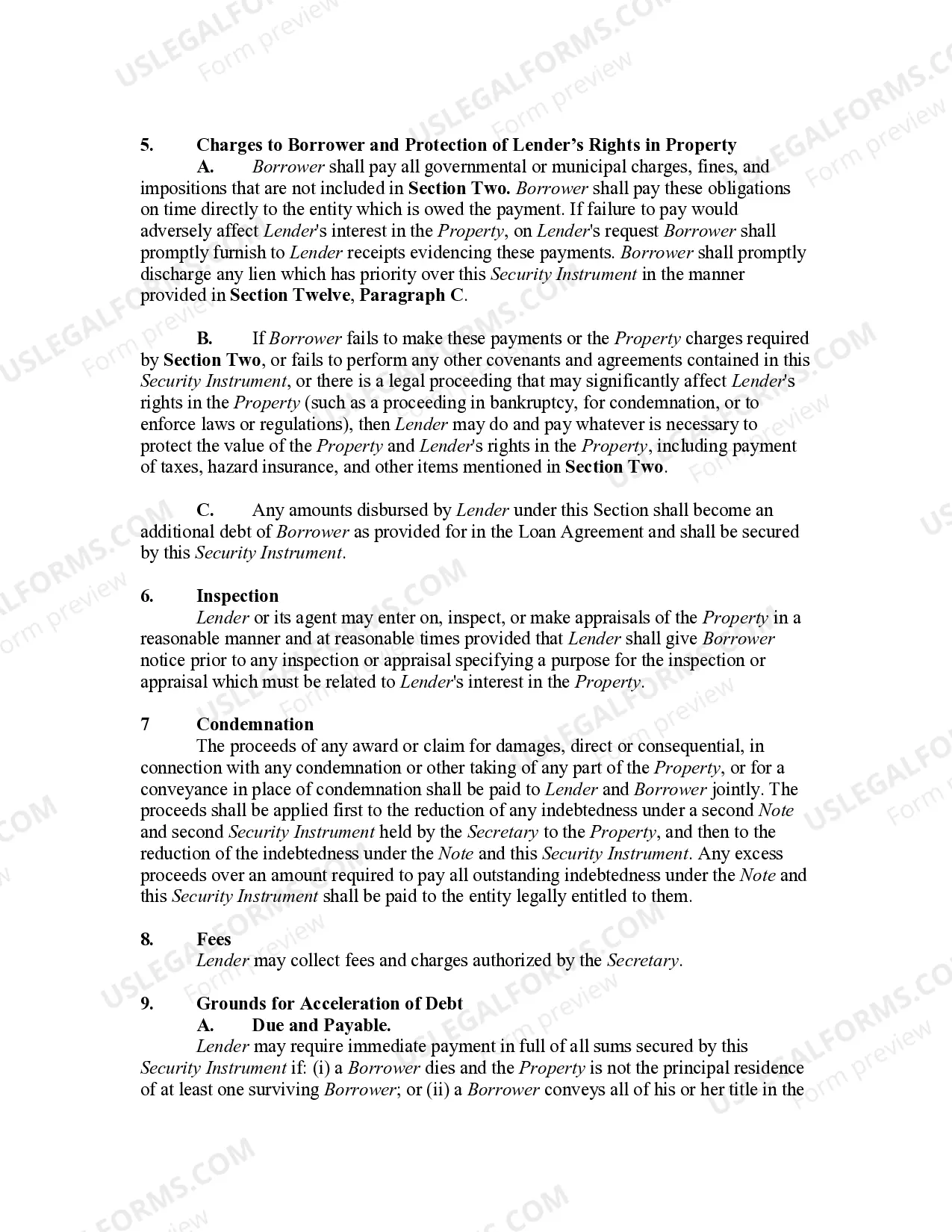

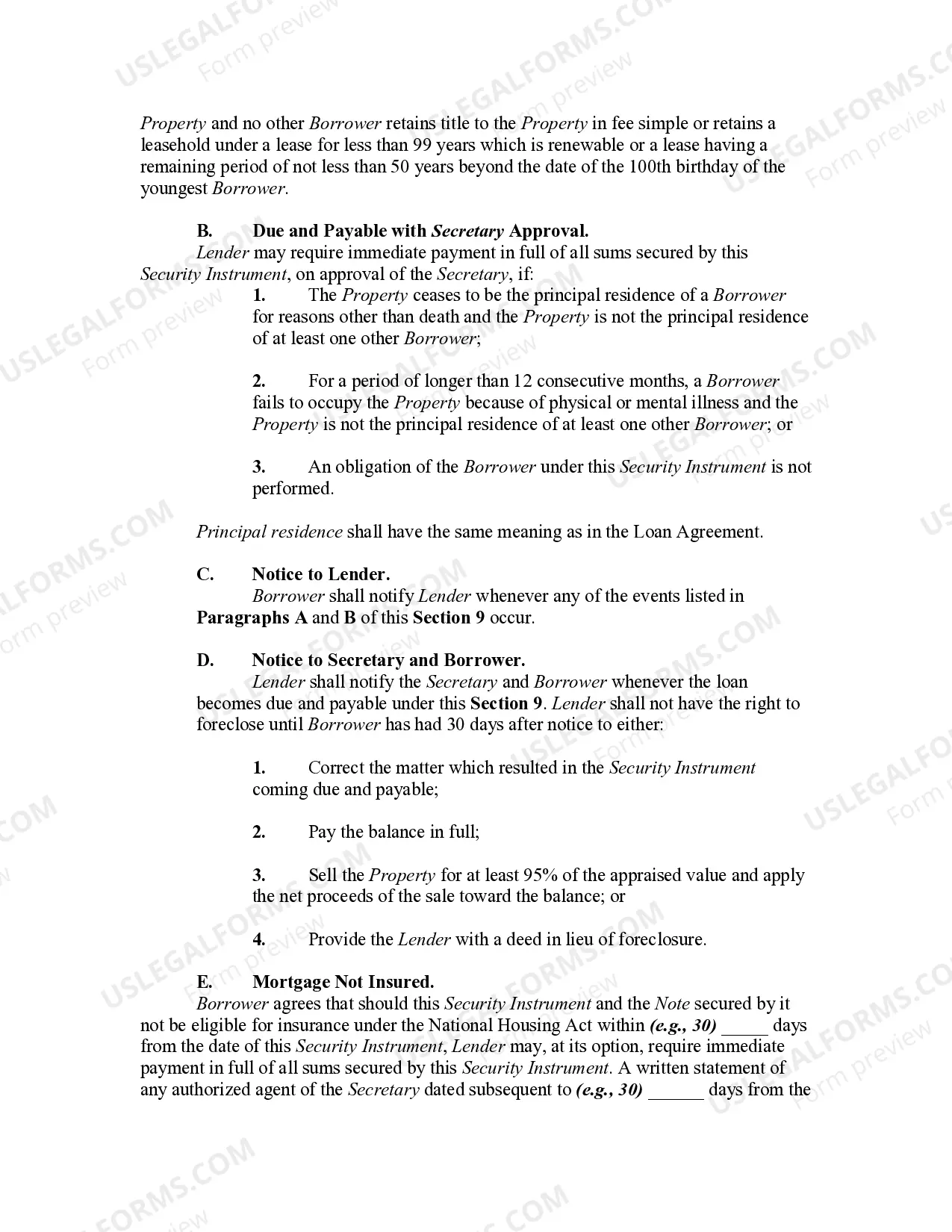

A reverse mortgage is a loan from the U.S. Government for 50% to 75% of the value of a home owned by a homeowner aged 62 and older. Instead of making monthly payments to a lender, as with a regular mortgage, a lender makes payments to the homeowner. The funds from a reverse mortgage are tax-free. The loan doesn't have to be repaid in the homeowner's lifetime, however, when the homeowner dies, the money received plus approximately 4% interest is repaid by their estate. The loan is repaid when the homeowner ceases to occupy the home as a principal residence, due to the homeowner (the last remaining spouse, in cases of couples) passing away, selling the home, or permanently moving out.

A Pennsylvania Home Equity Conversion Mortgage, commonly known as a reverse mortgage, is a specialized financial product designed for homeowners aged 62 or older. This type of mortgage allows eligible individuals to convert a portion of their home's equity into tax-free funds, without the need to sell their property or make monthly mortgage payments. Here are different types of Pennsylvania Home Equity Conversion Mortgage — Reverse Mortgage: 1. Home Equity Conversion Mortgage (HELM): The most common type of reverse mortgage, insured by the Federal Housing Administration (FHA) and regulated by the Department of Housing and Urban Development (HUD). Available through participating lenders, Helms offer a range of payment options and provide various protections for borrowers. 2. HELM for Purchase: This reverse mortgage variant is specifically designed to help seniors purchase a new home using only the proceeds from the reverse mortgage loan. Seniors can downsize or move closer to family without using a significant portion of their retirement savings. 3. Jumbo Reverse Mortgage: Certain borrowers with high-value homes may opt for a jumbo reverse mortgage, which allows them to access larger loan amounts beyond the standard HELM loan limits. Jumbo reverse mortgages offer more flexibility in providing substantial funds while following the general reverse mortgage principles. 4. Single-Purpose Reverse Mortgage: Unlike Helms, single-purpose reverse mortgages are typically offered by state or local government agencies and some non-profit organizations. These mortgages can be used for specific purposes, such as home repairs or property taxes, but are not as widely available. 5. Proprietary Reverse Mortgage: Some private lenders offer proprietary reverse mortgages, which are tailor-made for higher-value homes and borrowers with unique financial circumstances. Proprietary reverse mortgages are not federally insured like Helms, but they often provide larger loan amounts. 6. Reverse Mortgage Line of Credit: This type of reverse mortgage allows borrowers to establish a line of credit that grows over time. The borrower can access funds from the line of credit whenever needed, but they only accrue interest on the amount they use. A Pennsylvania Home Equity Conversion Mortgage — Reverse Mortgage can help seniors access their home equity and supplement their retirement income, cover medical expenses, or fund necessary home improvements. Before considering a reverse mortgage, it is essential to consult with a HUD-approved reverse mortgage counselor to understand the specific terms, costs, and potential implications.