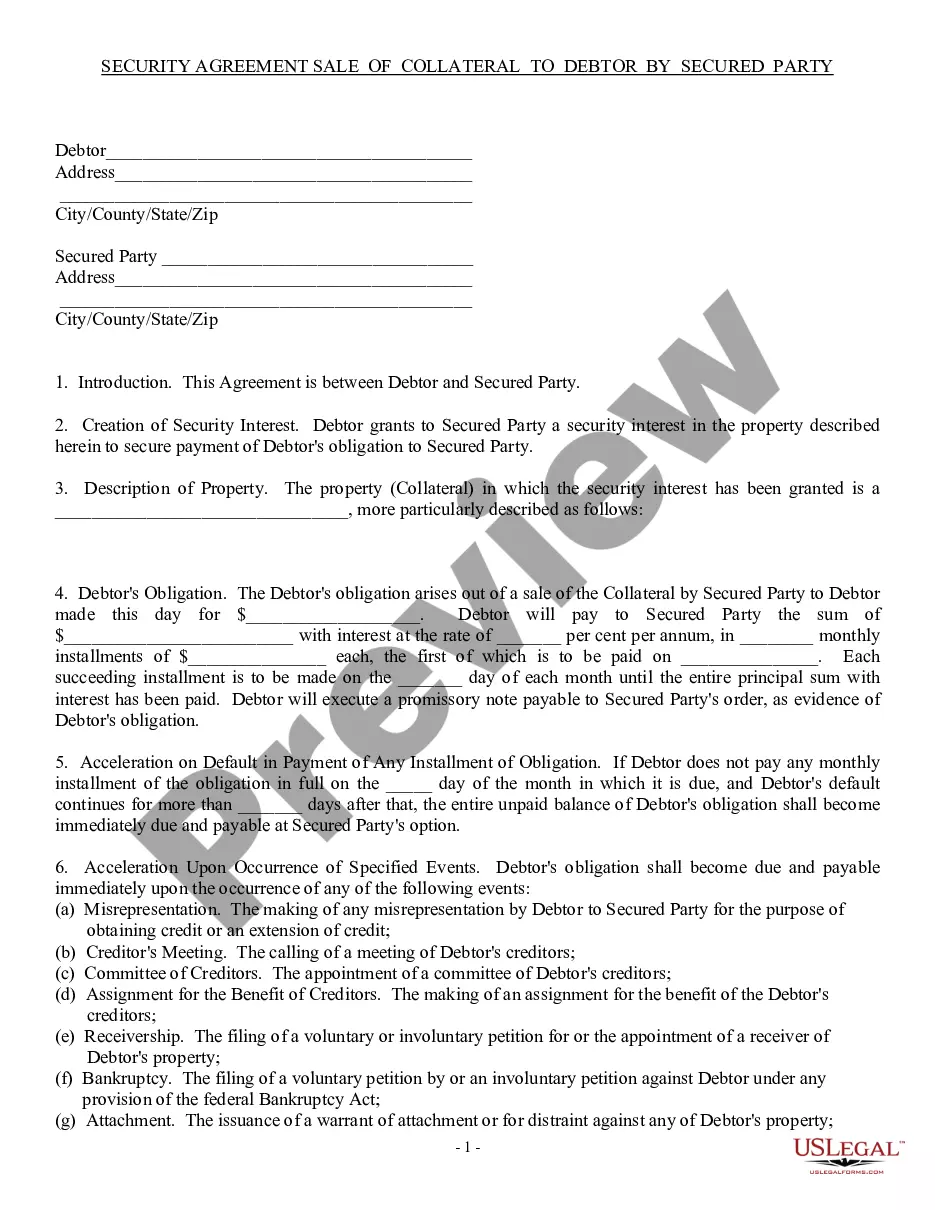

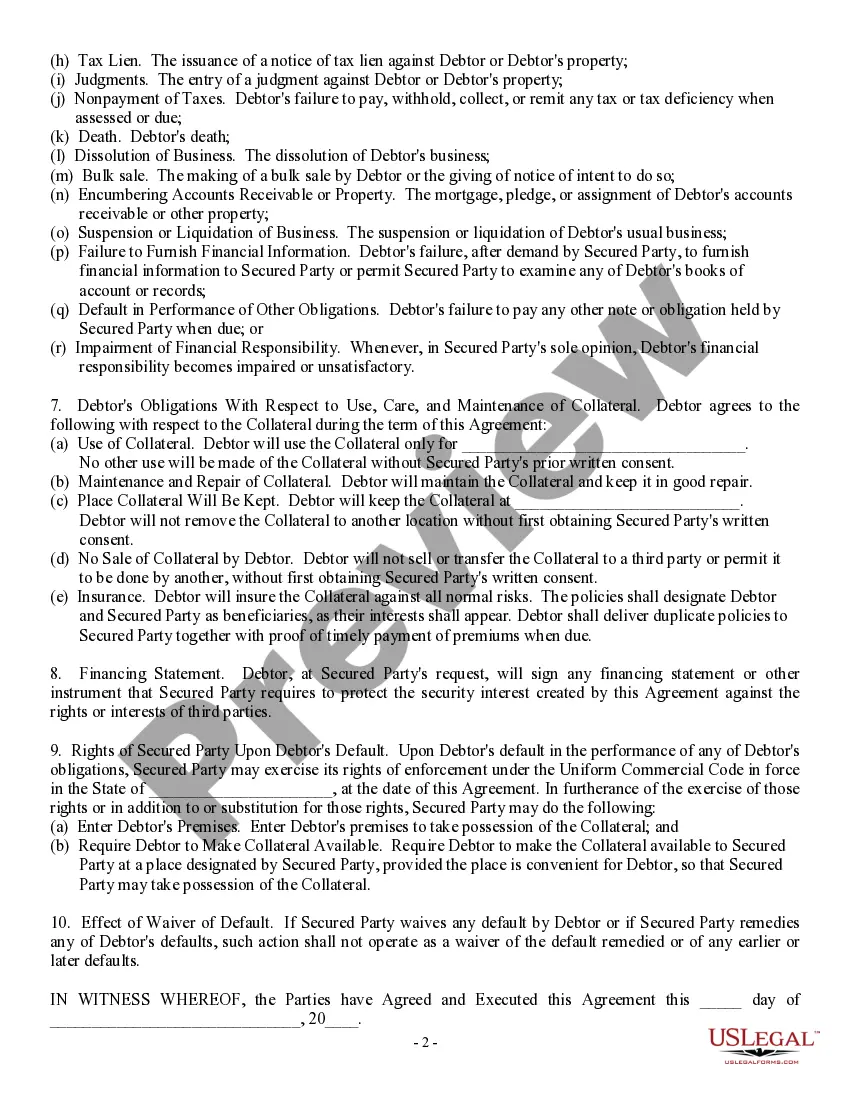

Pennsylvania Security Agreement involving Sale of Collateral by Debtor is a legally binding contract that outlines the terms and conditions for securing a loan or credit transaction. This agreement is often entered between a debtor (the borrower) and a secured party (the lender) to protect the lender's rights in the event of default or non-payment. The primary purpose of the Pennsylvania Security Agreement is to establish a security interest in specific collateral owned by the debtor. Collateral refers to any property, assets, or goods that the debtor pledges as security for the loan, ensuring that the lender has a legal claim to them in case of default. This collateral can include real estate, vehicles, equipment, inventory, accounts receivable, or any other valuable assets. The agreement generally includes the following key components: 1. Identification of the parties: This includes the full legal names and addresses of both the debtor and the secured party. 2. Description of the collateral: A detailed list of the collateral being used to secure the loan. This may include specific identification numbers, serial numbers, descriptions, or other relevant details to clearly identify the collateral. 3. Granting and perfection of the security interest: The debtor grants the secured party a security interest in the collateral. To perfect the security interest, certain requirements under the Uniform Commercial Code (UCC) must be fulfilled, such as filing a financing statement with the appropriate state agency. 4. Obligations of the debtor: This section outlines the responsibilities and duties of the debtor, such as making timely payments, maintaining insurance on the collateral, and not selling or encumbering the collateral without the secured party's consent. 5. Remedies in case of default: The agreement specifies the lender's rights and remedies in case of default, including the ability to seize, sell, or dispose of the collateral to recover the outstanding debt. It may also include provisions for the debtor's right to cure the default and any applicable notification requirements. 6. Representations and warranties: Both parties usually provide certain representations and warranties, ensuring that they have the authority to enter into the agreement, that the collateral is owned by the debtor, and that it is free from any liens or encumbrances. 7. Governing law and jurisdiction: The agreement typically states that it will be governed by and interpreted under the laws of Pennsylvania, and any disputes will be resolved through arbitration or litigation within the state's jurisdiction. Types of Pennsylvania Security Agreements involving the Sale of Collateral by the Debtor: 1. Traditional Security Agreement: This is the most common type of security agreement, where the debtor pledges specific collateral to secure a loan or credit transaction. 2. Cross-Collateralization Agreement: In this agreement, the debtor offers multiple assets or properties as collateral to secure a single loan or credit facility. The lender can then seize and sell any of the collateral in case of default. 3. After-Acquired Property Security Agreement: This agreement includes language stating that the security interest extends to any property acquired by the debtor after the agreement is signed. This provides ongoing protection to the lender in case the debtor obtains additional collateral during the term of the agreement. 4. Floating Lien Agreement: A floating lien enables the debtor to use their inventory or accounts receivable as collateral. This type of agreement allows the debtor to sell or replace the collateral as part of normal business operations, with the floating lien attaching to the constantly changing assets. It is crucial for all parties involved to consult legal professionals and review the specific requirements imposed by Pennsylvania law when entering into a Security Agreement involving the Sale of Collateral by the Debtor.

Pennsylvania Security Agreement involving Sale of Collateral by Debtor

Description

How to fill out Pennsylvania Security Agreement Involving Sale Of Collateral By Debtor?

Choosing the best authorized papers web template might be a have difficulties. Needless to say, there are plenty of themes accessible on the Internet, but how will you find the authorized develop you will need? Use the US Legal Forms site. The services provides thousands of themes, such as the Pennsylvania Security Agreement involving Sale of Collateral by Debtor, that can be used for organization and personal demands. All of the types are checked out by professionals and meet up with federal and state requirements.

Should you be presently listed, log in to your bank account and click the Obtain button to find the Pennsylvania Security Agreement involving Sale of Collateral by Debtor. Utilize your bank account to check from the authorized types you may have bought formerly. Proceed to the My Forms tab of your own bank account and get an additional copy of your papers you will need.

Should you be a brand new consumer of US Legal Forms, allow me to share simple instructions so that you can follow:

- Initially, be sure you have selected the correct develop to your area/area. It is possible to check out the shape while using Preview button and study the shape outline to guarantee this is the best for you.

- When the develop fails to meet up with your preferences, use the Seach discipline to get the proper develop.

- Once you are certain the shape is acceptable, select the Purchase now button to find the develop.

- Opt for the costs program you would like and enter in the necessary details. Build your bank account and pay money for the order with your PayPal bank account or credit card.

- Opt for the file formatting and down load the authorized papers web template to your system.

- Total, edit and print out and indicator the acquired Pennsylvania Security Agreement involving Sale of Collateral by Debtor.

US Legal Forms is the largest library of authorized types that you can see various papers themes. Use the company to down load expertly-made paperwork that follow state requirements.