Generally, a contract to employ a certified public accountant need not be in writing.

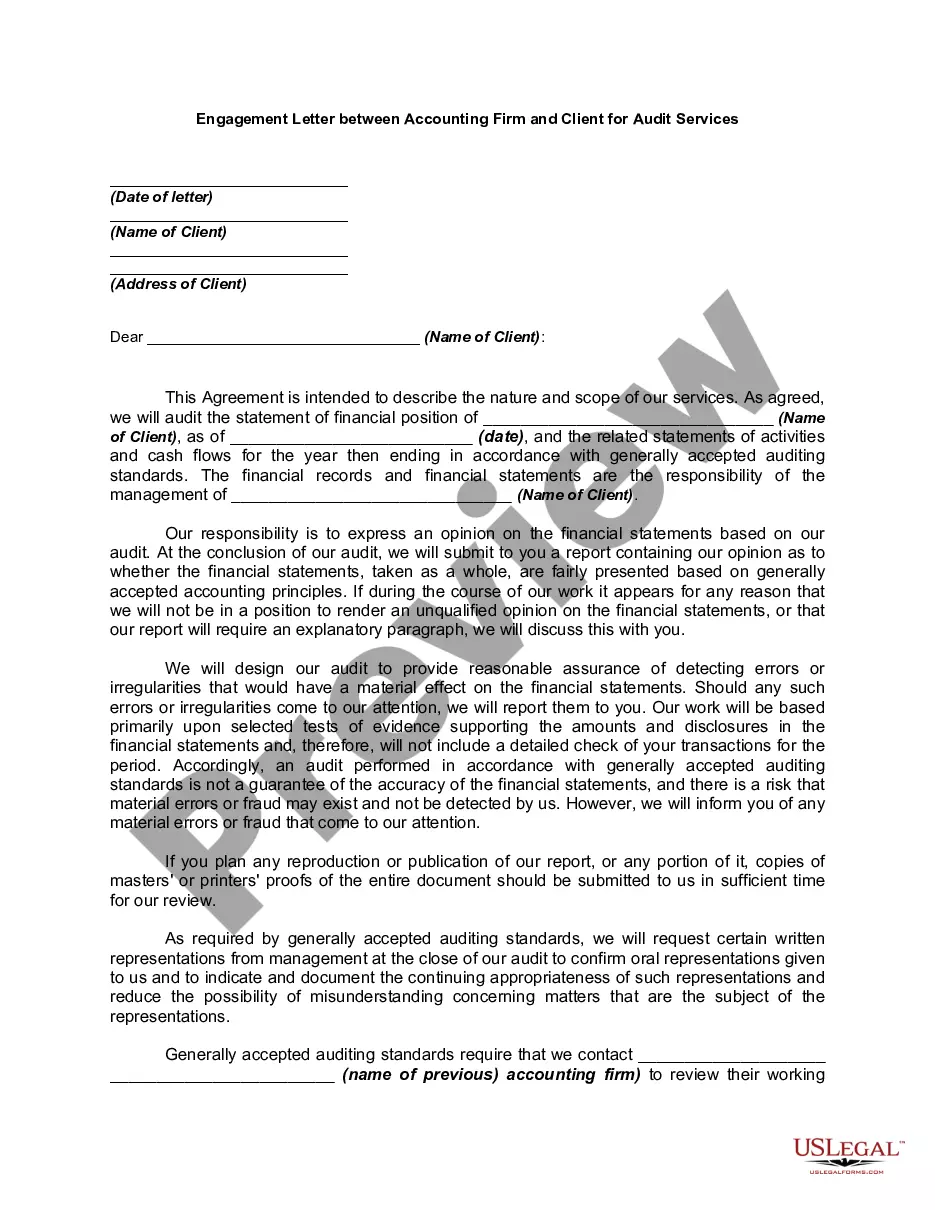

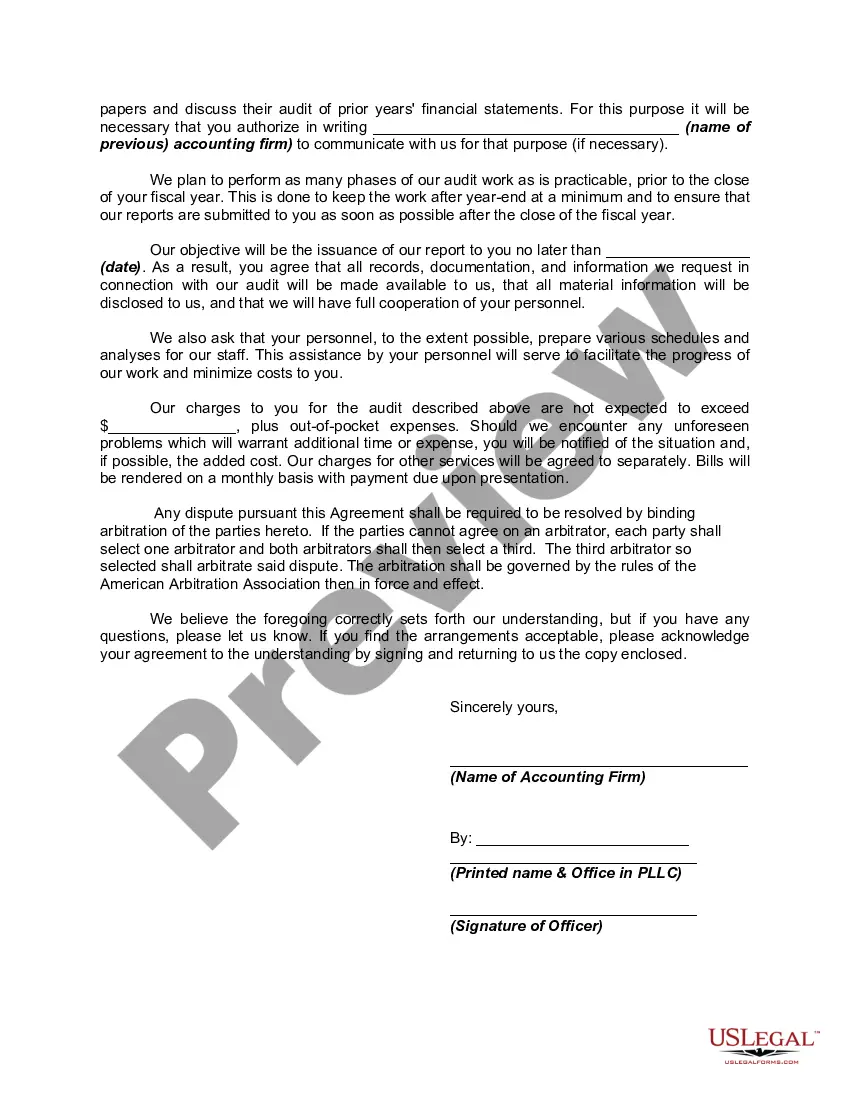

However, such contracts often call for services of a highly complex and technical nature, and hence they should be explicit in their terms, and they should be in writing. In particular, a written employment contract is necessary in order to avoid misunderstanding with the employer regarding the amount of the accountant's fee or compensation and the nature of its computation. As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

A Pennsylvania Engagement Letter between an accounting firm and a client for audit services serves as a formal agreement outlining the terms and conditions of the auditor-client relationship. This document is crucial for establishing mutual understanding and expectations between the parties involved. Here is a detailed description of what this letter typically includes: 1. Introduction: The engagement letter starts by identifying the parties involved, including the accounting firm's name, address, and contact information, followed by the client's information, such as their company name, address, and primary point of contact. 2. Objective and Scope of Engagement: This section outlines the objective of the engagement, which is typically to conduct an audit in accordance with generally accepted auditing standards (GAS), as well as any relevant statutory requirements. The scope of the audit engagement is defined, specifying which financial statements will be audited (e.g., balance sheet, income statement) and the applicable time period. 3. Responsibilities: Both parties' responsibilities are clearly defined to ensure a successful engagement. The accounting firm outlines its responsibilities, such as performing the audit in accordance with professional standards, maintaining independence, and providing a written audit report. The client's responsibilities may include providing access to relevant financial records, ensuring the accuracy of financial statements, and appointing a responsible individual to facilitate the audit process. 4. Terms and Fee Structure: This section outlines the duration of the engagement, whether it is for a specific fiscal year or a shorter/longer period, as well as the billing cycle (e.g., hourly, monthly, or fixed fee). The engagement letter may also mention any additional expenses the client is responsible for, such as travel expenses or additional requested services. 5. Confidentiality: Both parties are typically required to maintain the confidentiality of any information obtained during the audit engagement, in compliance with applicable laws and professional standards. 6. Limitation of Liability: This section often includes an agreement where the accounting firm's liability is limited to a certain extent or disclaimed altogether, except in cases of gross negligence or willful misconduct. 7. Termination: The engagement letter may outline the circumstances under which either party can terminate the engagement, such as non-payment, breach of contract, or mutual agreement. Different types of Pennsylvania Engagement Letters for Audit Services may include: a) Initial Engagement: This is the first engagement letter that establishes the relationship between the accounting firm and the client for a specific audit engagement. b) Renewal Engagement: When the audit engagement extends beyond the initial engagement period, the parties may opt for a renewal engagement letter, which updates the terms and conditions while maintaining the overall agreement. c) Amendment Engagement: If certain agreed-upon terms need to be modified during the engagement, an amendment engagement letter is used to formally record the changes. d) Limited Scope Engagement: Sometimes, an engagement letter may be used for limited scope audits, where only specific aspects of an organization's financial statements or operations are reviewed rather than a comprehensive audit. It is important to note that while this content provides an overview of the typical elements of a Pennsylvania Engagement Letter Between Accounting Firm and Client For Audit Services, specific requirements may vary, and it is advisable to consult with legal and accounting professionals for drafting appropriate engagement letters.