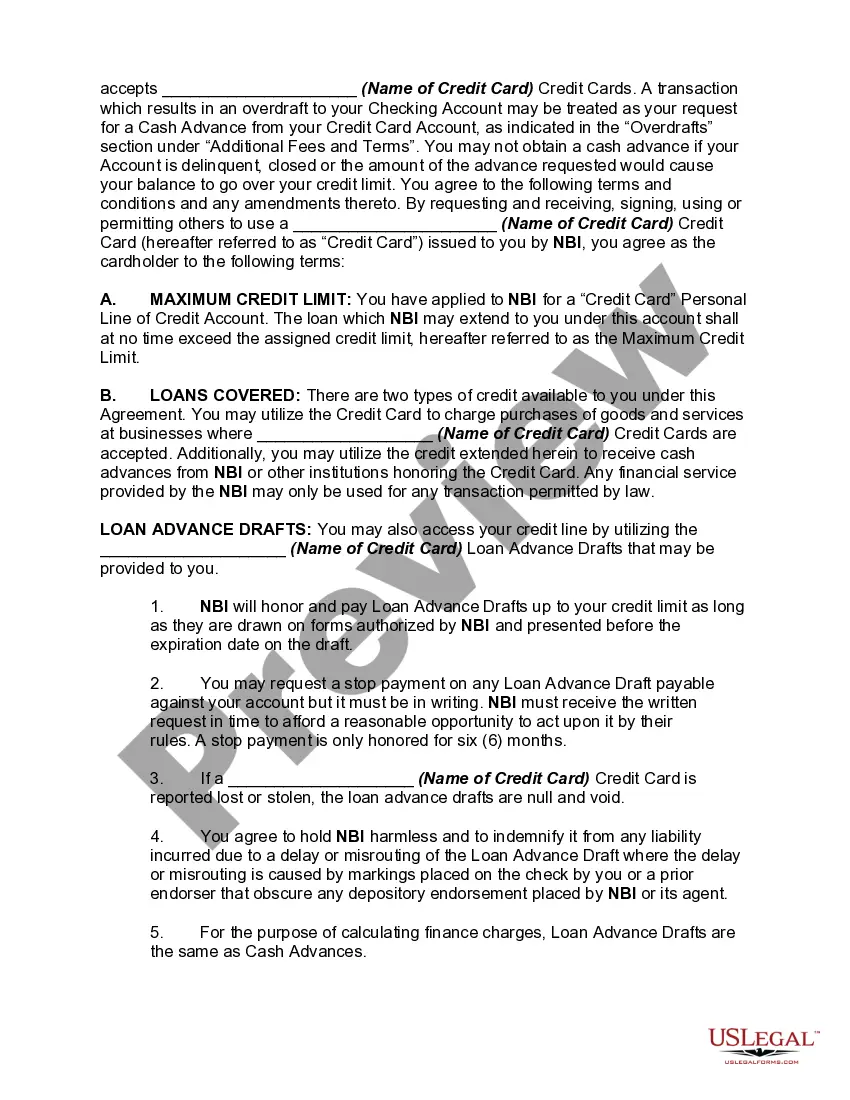

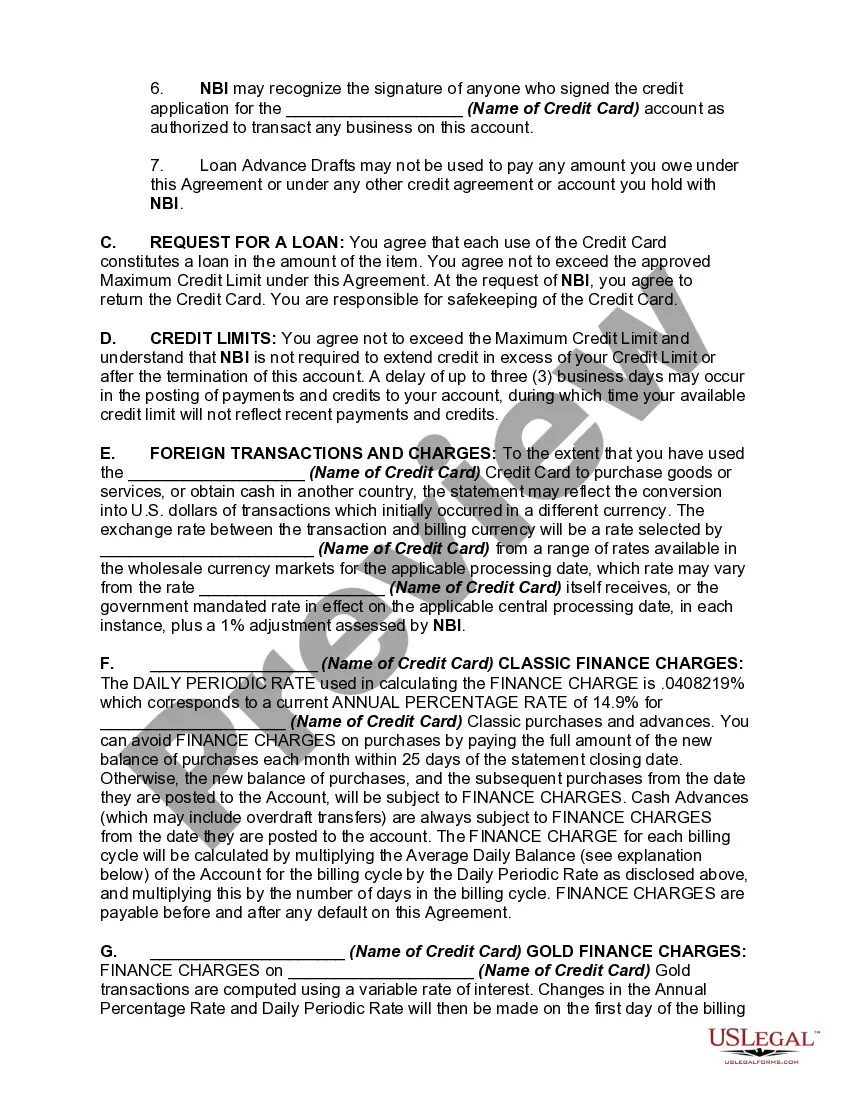

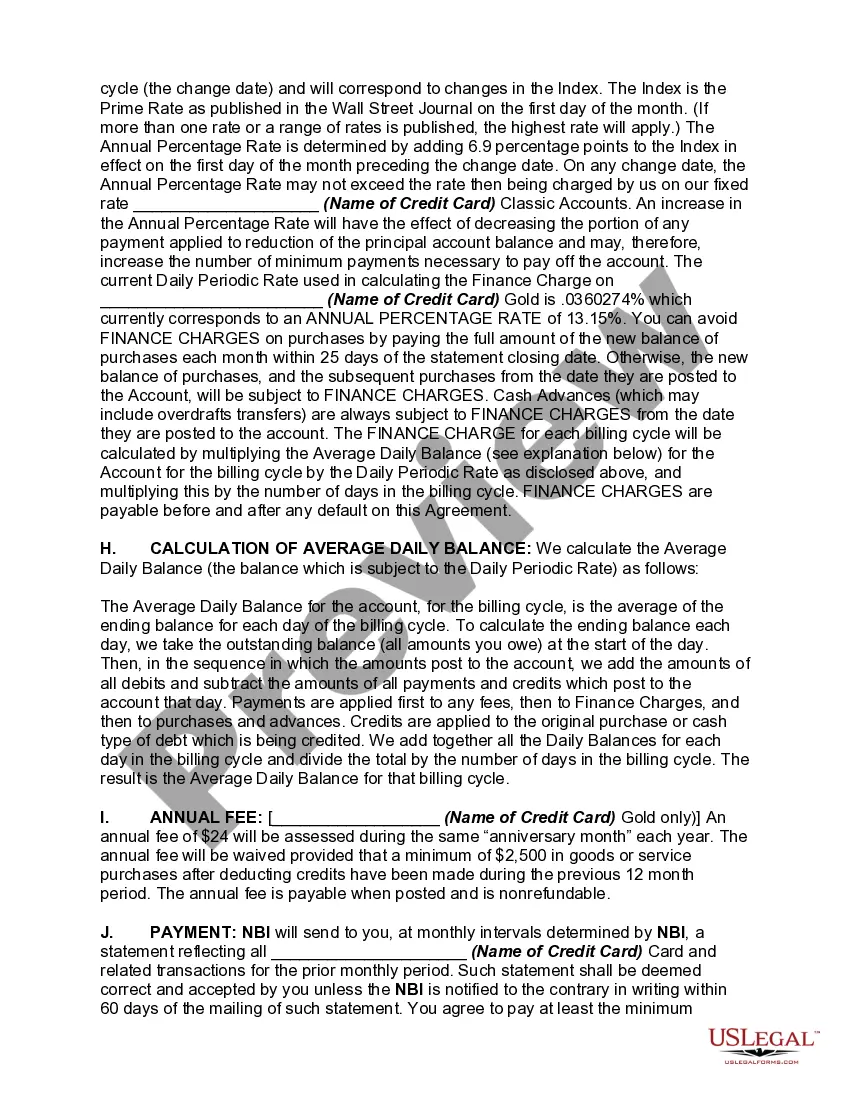

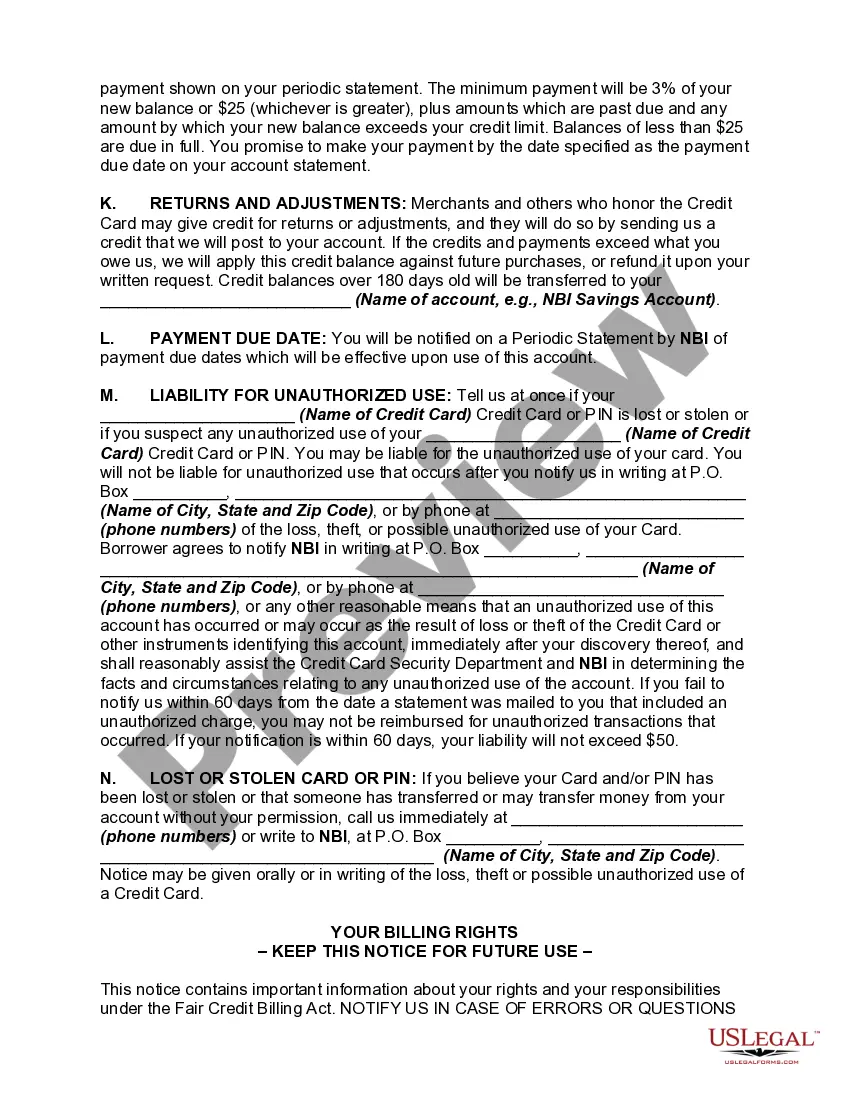

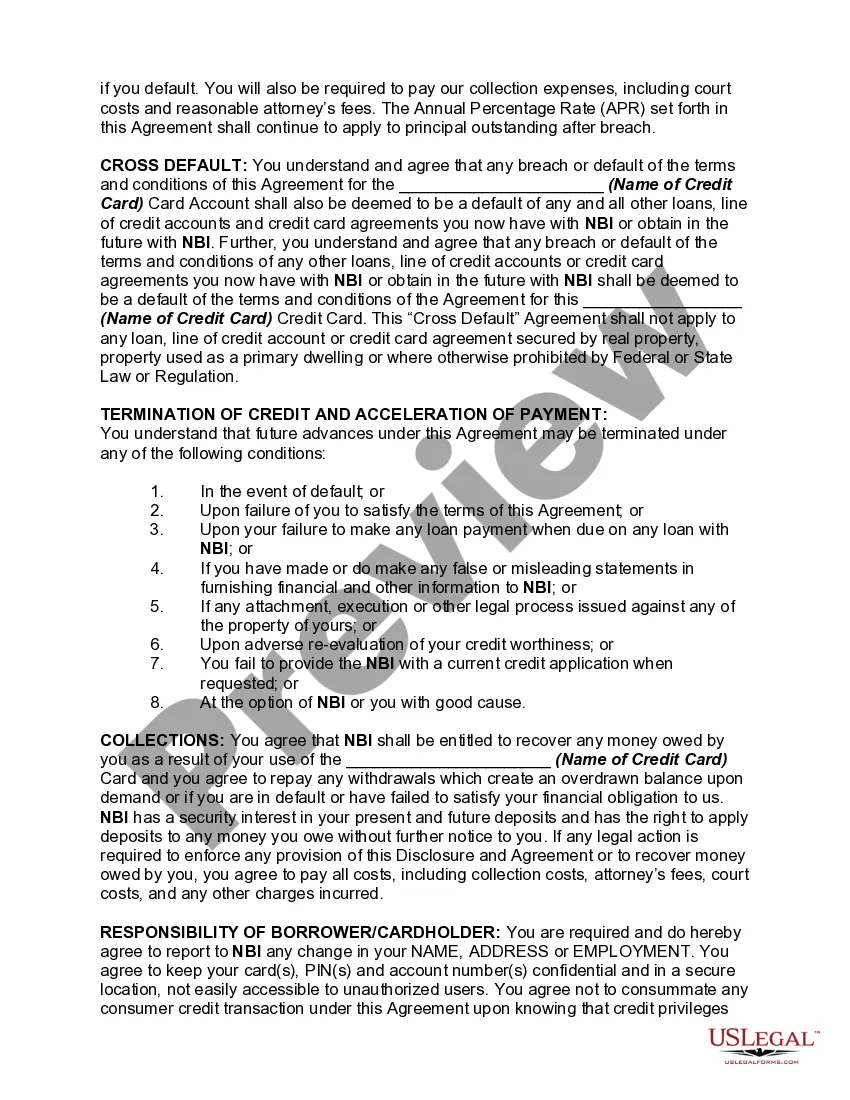

The Pennsylvania Credit Card Agreement and Disclosure Statement is a legal document that outlines the terms and conditions between a credit card issuer and the credit cardholder residing in the state of Pennsylvania. It serves to provide transparency regarding the credit card agreement, including interest rates, fees, and cardholder rights. Compliance with this document is mandatory for credit card issuers operating within the state of Pennsylvania. Within the Pennsylvania Credit Card Agreement and Disclosure Statement, several key components are addressed to protect the cardholder and ensure fair practices. These components include: 1. Interest Rates and Annual Percentage Rate (APR): The agreement specifies the interest rates applicable to various transactions, such as purchases, cash advances, and balance transfers. The APR is also disclosed, representing the annual cost of borrowing on the credit card. 2. Fees and Charges: Various fees associated with the credit card are listed in detail, including late payment fees, over-limit fees, cash advance fees, and foreign transaction fees. The agreement provides transparency about when these fees may be imposed and their respective amounts. 3. Grace Period: The agreement outlines the length of the grace period, which is the time given to the cardholder to pay the balance in full without incurring interest charges. This period usually ranges from 21 to 25 days, allowing cardholders to avoid interest if the outstanding balance is paid within this timeframe. 4. Billing and Payment Information: The agreement explains how the billing cycle operates, the due dates for payment, and the accepted methods of payment. It also specifies the consequences of late or missed payments, including penalties and potential damage to the cardholder's credit score. 5. Credit Limits: The agreement states the credit limit allotted to the cardholder. It ensures that cardholders understand their maximum borrowing capacity and that exceeding the limit may result in additional fees or declined transactions. 6. Dispute Resolution and Legal Rights: This section of the agreement outlines the cardholder's rights in the event of a dispute, including the process for filing a complaint or arbitration. It also ensures compliance with relevant Pennsylvania state laws, such as the Fair Credit Billing Act and the Truth in Lending Act. Types of Pennsylvania Credit Card Agreement and Disclosure Statements may vary based on factors such as the credit card issuer, specific card program, or card type. Some examples of credit card that may have their own respective Pennsylvania Credit Card Agreement and Disclosure Statement include: 1. General Consumer Credit Cards: These credit cards are designed for everyday use, providing a variety of benefits and rewards to the cardholder. 2. Business Credit Cards: Aimed at entrepreneurs and business owners, these credit cards offer features specifically tailored to meet business needs, such as expense tracking and reporting tools. 3. Student Credit Cards: Geared towards students, these credit cards often have lower credit limits and provide features like cashback rewards or educational resources to help students build credit responsibly. 4. Secured Credit Cards: Ideal for individuals with limited or poor credit history, secured credit cards require a security deposit and allow cardholders to establish or rebuild their credit. Please note, the specific names and variations of Pennsylvania Credit Card Agreement and Disclosure Statements may differ based on the issuing bank and credit card program.

Pennsylvania Credit Card Agreement and Disclosure Statement

Description

How to fill out Pennsylvania Credit Card Agreement And Disclosure Statement?

You are able to devote time on the Internet trying to find the lawful papers template that meets the state and federal specifications you will need. US Legal Forms provides 1000s of lawful varieties which can be analyzed by experts. You can actually down load or print out the Pennsylvania Credit Card Agreement and Disclosure Statement from my support.

If you already possess a US Legal Forms accounts, you are able to log in and click the Download key. Following that, you are able to complete, change, print out, or indication the Pennsylvania Credit Card Agreement and Disclosure Statement. Every single lawful papers template you get is the one you have permanently. To obtain yet another version of the bought develop, go to the My Forms tab and click the related key.

If you use the US Legal Forms site for the first time, stick to the easy instructions beneath:

- First, make certain you have chosen the correct papers template for your state/metropolis of your liking. Look at the develop information to ensure you have picked the appropriate develop. If available, utilize the Preview key to search from the papers template as well.

- In order to get yet another edition of your develop, utilize the Research field to discover the template that fits your needs and specifications.

- Upon having found the template you desire, just click Buy now to continue.

- Choose the prices program you desire, type in your qualifications, and register for a free account on US Legal Forms.

- Complete the deal. You should use your charge card or PayPal accounts to fund the lawful develop.

- Choose the format of your papers and down load it to the gadget.

- Make adjustments to the papers if necessary. You are able to complete, change and indication and print out Pennsylvania Credit Card Agreement and Disclosure Statement.

Download and print out 1000s of papers templates while using US Legal Forms website, that offers the most important variety of lawful varieties. Use professional and condition-particular templates to take on your company or specific needs.