A nonprofit corporation is one that is organized for charitable or benevolent purposes. These corporations include certain hospitals, universities, churches, and other religious organizations. A nonprofit entity does not have to be a nonprofit corporation, however. Nonprofit corporations do not have shareholders, but have members or a perpetual board of directors or board of trustees.

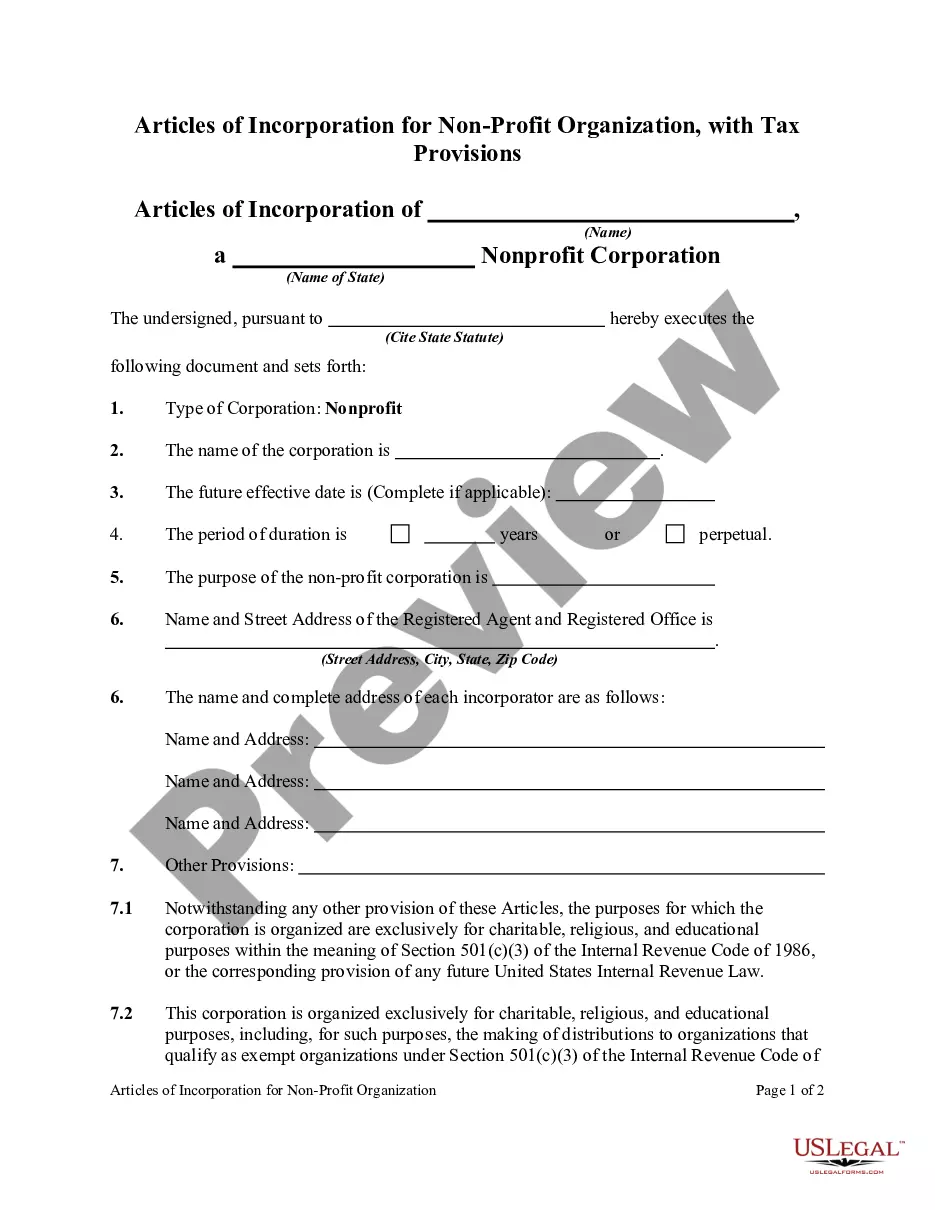

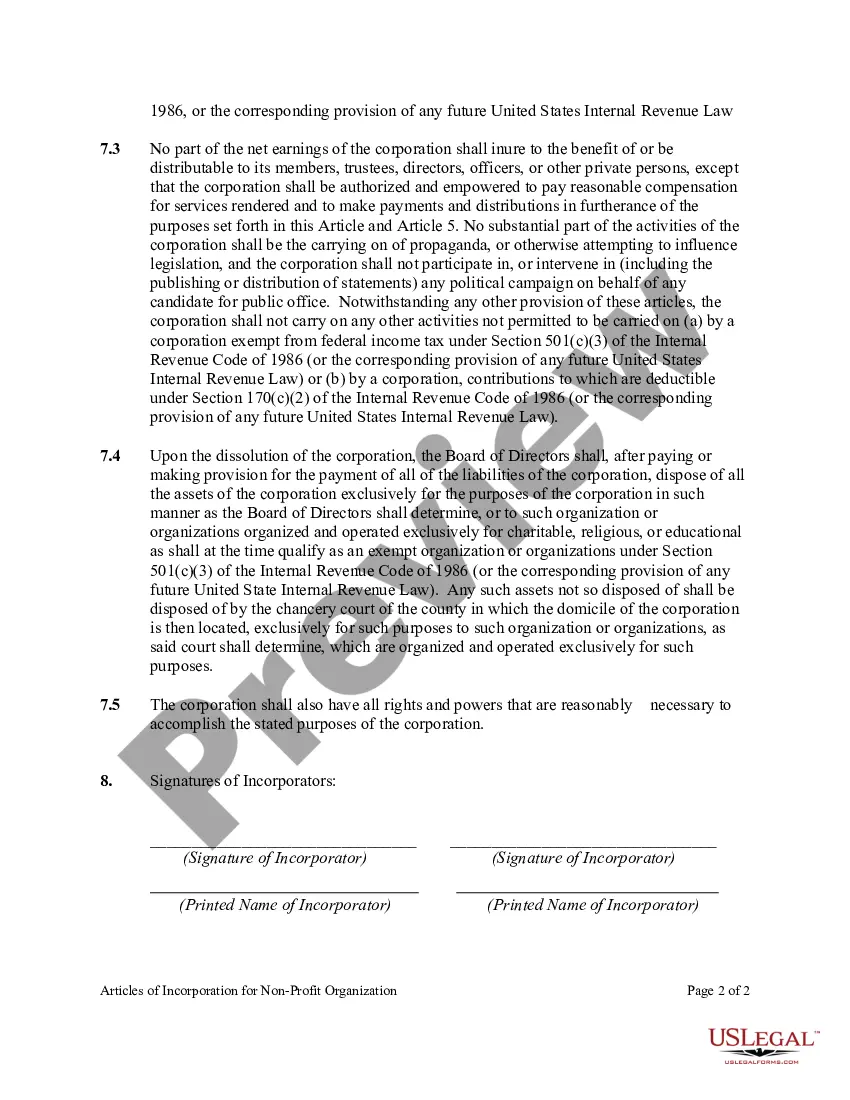

The Pennsylvania Articles of Incorporation for Non-Profit Organization with Tax Provisions is a legal document required by the Pennsylvania Department of State for the incorporation of a non-profit organization in the state. These articles outline essential information about the organization's formation, purpose, structure, and tax provisions. In Pennsylvania, there are primarily two types of Articles of Incorporation for Non-Profit Organizations with Tax Provisions: the Regular Articles of Incorporation and the Specific Purpose Articles of Incorporation. The Regular Articles of Incorporation are used by non-profit organizations seeking to establish themselves as 501(c)(3) tax-exempt entities under the Internal Revenue Code. These organizations typically have broad purposes, such as charitable, educational, religious, or scientific activities. The Regular Articles of Incorporation detail the organization's name, purpose, registered office and agent, duration, and initial board of directors. The Specific Purpose Articles of Incorporation, on the other hand, are designed for non-profit organizations with a narrow, defined purpose that may not fall under the typical 501(c)(3) tax-exempt categories. These organizations include professional associations, trade organizations, and business leagues. The Specific Purpose Articles of Incorporation identify the organization's name, specific purpose, registered office and agent, duration, and initial board of directors. Both types of Pennsylvania Article of Incorporation for Non-Profit Organization with Tax Provisions include provisions related to tax exemption. They outline the non-profit organization's commitment to operating exclusively for charitable, educational, or other exempt purposes. Furthermore, they specify that no part of the organization's earnings shall benefit any individual or private shareholder. To ensure compliance with federal and state tax laws, non-profit organizations must include specific language in their Articles of Incorporation related to tax-exempt status and limitations on lobbying and political activities. These tax provisions are crucial to maintaining the organization's exemption from federal income tax and allow donors to make tax-deductible contributions. In conclusion, the Pennsylvania Articles of Incorporation for Non-Profit Organization with Tax Provisions is a vital legal document for establishing a non-profit organization in Pennsylvania. Whether using the Regular or Specific Purpose Articles, it is essential to include specific tax provisions that guarantee compliance with federal and state tax laws, as well as confirm the organization's commitment to its charitable or exempt purposes.