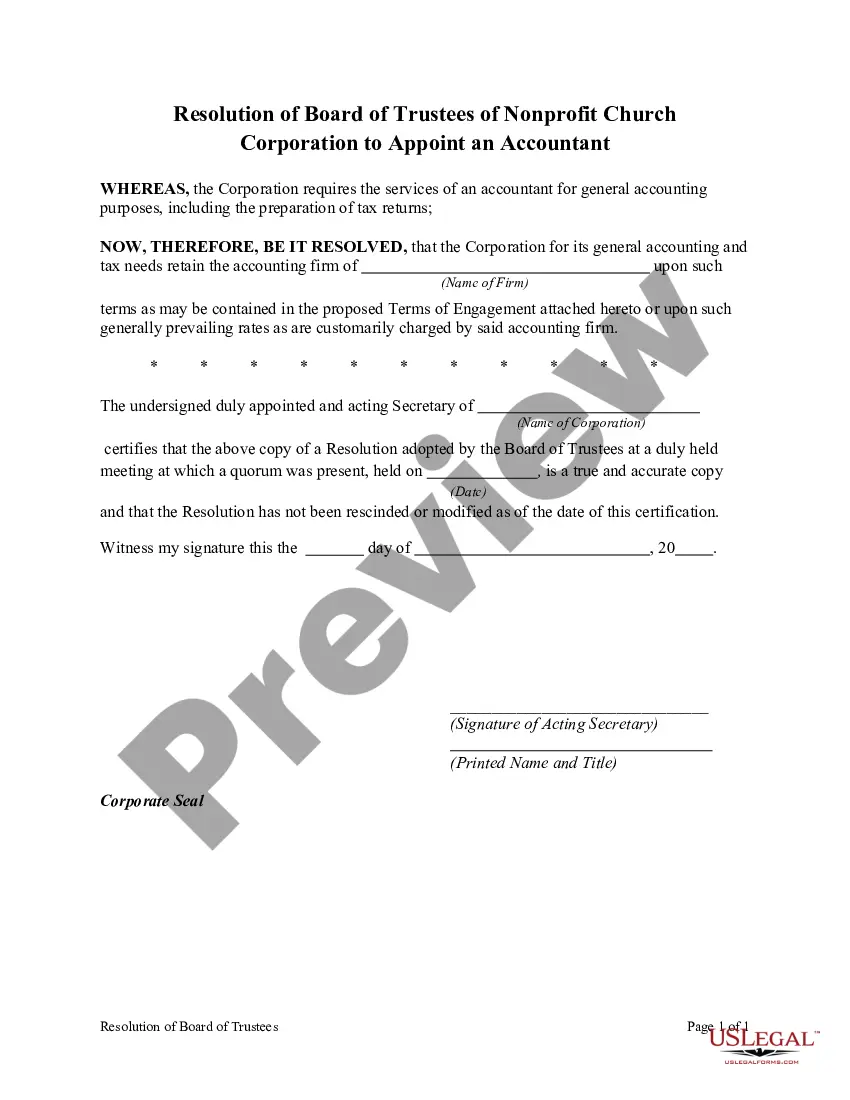

Nonprofit Church Corporate resolutions are generally formal actions and decisions of a corporation, approved by the Board of Trustees or Elders. They are formalized statements that have been voted upon and approved by the corporate trustees, typically authorizing a specific corporate action.

Keywords: Pennsylvania, Resolution, Board of Trustees, Nonprofit Church Corporation, Appoint, Accountant Title: Understanding the Pennsylvania Resolution of Board of Trustees of Nonprofit Church Corporation to Appoint an Accountant Introduction: In the state of Pennsylvania, nonprofit church corporations have specific guidelines to follow when appointing an accountant. The Pennsylvania Resolution of Board of Trustees plays a crucial role in this appointment process. This resolution ensures transparency, accountability, and efficient financial management within the organization. Let's delve deeper into the details of this resolution and its various types. Types of Pennsylvania Resolutions of Board of Trustees for Appointing an Accountant: 1. Annual Appointment Resolution: The annual appointment resolution is one type of Pennsylvania Resolution of Board of Trustees for nonprofit church corporations. It designates a specific accountant or accounting firm to handle the financial affairs of the organization for a specific fiscal year. This resolution is typically enacted at the annual meeting of the board of trustees. 2. Special Appointment Resolution: The special appointment resolution is another type of Pennsylvania Resolution of Board of Trustees that is used when a nonprofit church corporation needs to appoint an accountant for a specific purpose or event. For example, if the organization is undergoing an audit or facing complex financial issues, the board of trustees may pass a special appointment resolution to engage an accountant with specific expertise in the relevant area. Details of the Pennsylvania Resolution of Board of Trustees: A Pennsylvania Resolution of Board of Trustees for nonprofit church corporations to appoint an accountant generally includes the following components: 1. Resolution Introduction: The resolution begins by outlining the purpose, authority, and the specific meeting where the resolution is being proposed. It may cite the relevant section of the corporation's bylaws or any applicable state regulations governing the appointment of an accountant. 2. Appointment Process: The resolution describes the steps involved in the appointment process. This includes identifying the criteria for selecting an accountant or accounting firm, evaluating qualifications and experience, and setting a timeline for the selection process. It may also mention any required approvals from external entities, such as the church congregation or an oversight committee. 3. Designation of Accountant: The resolution clearly states the name of the accountant or accounting firm who is being appointed, along with their contact details and qualifications. It may also highlight any specific responsibilities or tasks assigned to the accountant, such as auditing, financial reporting, or tax compliance. 4. Term of Appointment: The resolution specifies the duration of the accountant's appointment, whether it is for a single fiscal year or a defined period under special circumstances. It may also address the possibility of renewal or termination of the accountant's contract. 5. Reporting and Oversight: The resolution includes provisions for regular reporting and oversight of the accountant's work. It may outline reporting intervals, such as monthly, quarterly, or annually, as well as the responsibility of the board of trustees to review and approve financial reports. Conclusion: The Pennsylvania Resolution of Board of Trustees of Nonprofit Church Corporation to Appoint an Accountant is a critical instrument for ensuring the efficient management of financial affairs within nonprofit church corporations. By understanding the different types of resolutions and their key components, boards of trustees can fulfill their fiduciary duties and safeguard the organization's financial well-being.Keywords: Pennsylvania, Resolution, Board of Trustees, Nonprofit Church Corporation, Appoint, Accountant Title: Understanding the Pennsylvania Resolution of Board of Trustees of Nonprofit Church Corporation to Appoint an Accountant Introduction: In the state of Pennsylvania, nonprofit church corporations have specific guidelines to follow when appointing an accountant. The Pennsylvania Resolution of Board of Trustees plays a crucial role in this appointment process. This resolution ensures transparency, accountability, and efficient financial management within the organization. Let's delve deeper into the details of this resolution and its various types. Types of Pennsylvania Resolutions of Board of Trustees for Appointing an Accountant: 1. Annual Appointment Resolution: The annual appointment resolution is one type of Pennsylvania Resolution of Board of Trustees for nonprofit church corporations. It designates a specific accountant or accounting firm to handle the financial affairs of the organization for a specific fiscal year. This resolution is typically enacted at the annual meeting of the board of trustees. 2. Special Appointment Resolution: The special appointment resolution is another type of Pennsylvania Resolution of Board of Trustees that is used when a nonprofit church corporation needs to appoint an accountant for a specific purpose or event. For example, if the organization is undergoing an audit or facing complex financial issues, the board of trustees may pass a special appointment resolution to engage an accountant with specific expertise in the relevant area. Details of the Pennsylvania Resolution of Board of Trustees: A Pennsylvania Resolution of Board of Trustees for nonprofit church corporations to appoint an accountant generally includes the following components: 1. Resolution Introduction: The resolution begins by outlining the purpose, authority, and the specific meeting where the resolution is being proposed. It may cite the relevant section of the corporation's bylaws or any applicable state regulations governing the appointment of an accountant. 2. Appointment Process: The resolution describes the steps involved in the appointment process. This includes identifying the criteria for selecting an accountant or accounting firm, evaluating qualifications and experience, and setting a timeline for the selection process. It may also mention any required approvals from external entities, such as the church congregation or an oversight committee. 3. Designation of Accountant: The resolution clearly states the name of the accountant or accounting firm who is being appointed, along with their contact details and qualifications. It may also highlight any specific responsibilities or tasks assigned to the accountant, such as auditing, financial reporting, or tax compliance. 4. Term of Appointment: The resolution specifies the duration of the accountant's appointment, whether it is for a single fiscal year or a defined period under special circumstances. It may also address the possibility of renewal or termination of the accountant's contract. 5. Reporting and Oversight: The resolution includes provisions for regular reporting and oversight of the accountant's work. It may outline reporting intervals, such as monthly, quarterly, or annually, as well as the responsibility of the board of trustees to review and approve financial reports. Conclusion: The Pennsylvania Resolution of Board of Trustees of Nonprofit Church Corporation to Appoint an Accountant is a critical instrument for ensuring the efficient management of financial affairs within nonprofit church corporations. By understanding the different types of resolutions and their key components, boards of trustees can fulfill their fiduciary duties and safeguard the organization's financial well-being.