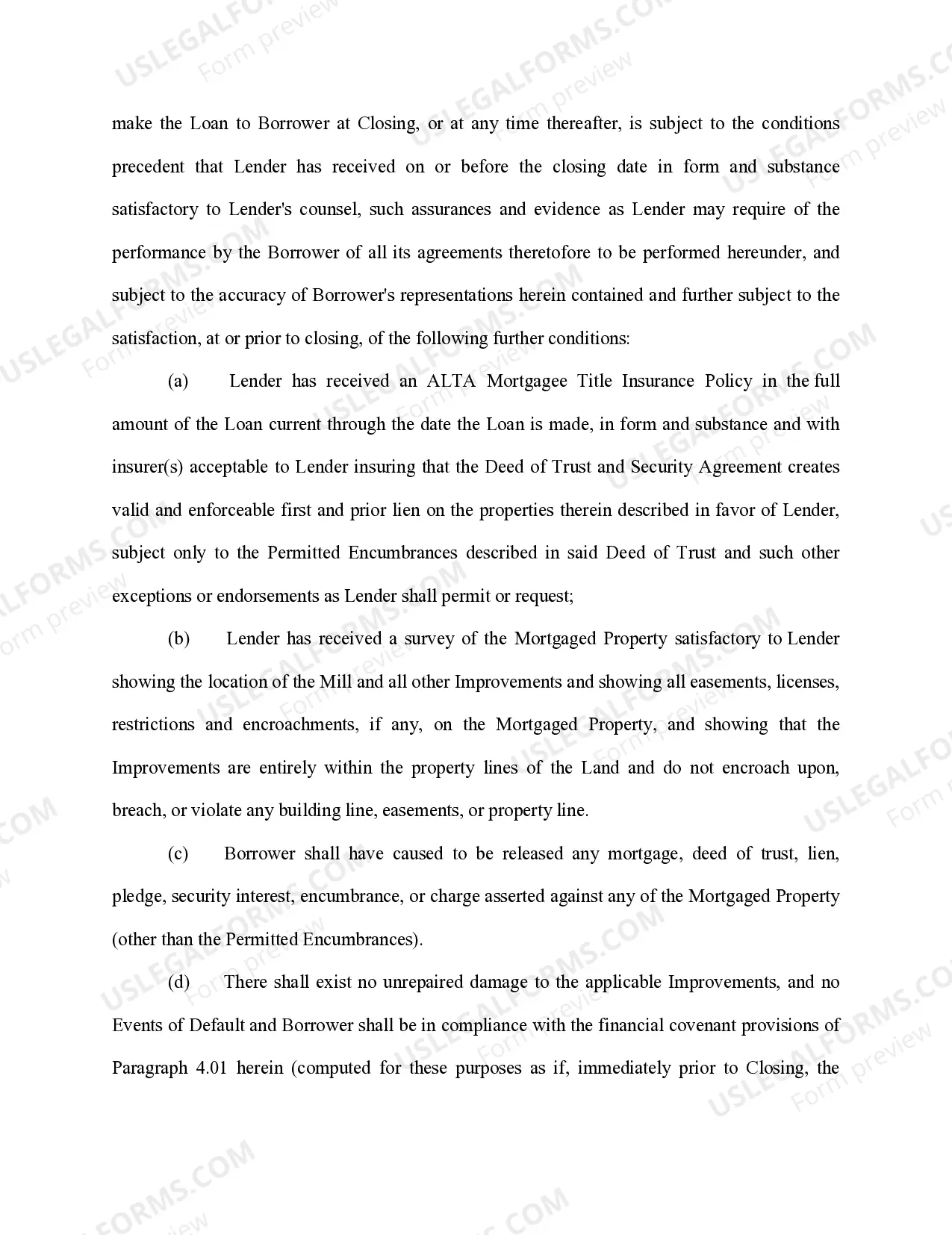

Pennsylvania Loan Agreement for Personal Loan: Explained A Pennsylvania Loan Agreement for Personal Loan refers to a legally binding contract between two parties involved in a personal lending transaction within the state of Pennsylvania. This document outlines the terms and conditions that govern the loan, providing clarity and protection for both the lender and the borrower. Keywords: Pennsylvania, Loan Agreement, Personal Loan, terms and conditions, legally binding contract, lending transaction, clarity, protection, lender, borrower. In Pennsylvania, like in many other states, there could be different types of Loan Agreements for Personal Loans. Some common variations are: 1. Secured Personal Loan Agreement: In this type of agreement, the borrower pledges a valuable asset, such as a car or property, as collateral to secure the loan. This provides the lender with a level of protection, as they can seize the asset in case of default. 2. Unsecured Personal Loan Agreement: Unlike secured loans, this type of loan agreement does not require any collateral. The lender grants the loan solely based on the borrower's creditworthiness. However, since there is no collateral involved, the lender typically charges a higher interest rate to compensate for the risk. 3. Installment Loan Agreement: This form of personal loan agreement divides the repayment into regular installments over a set period. It includes details such as the principal amount, interest rate, installment amount, repayment schedule, and any other applicable fees. 4. Payday Loan Agreement: A payday loan agreement is a short-term loan designed to provide immediate cash to borrowers for unexpected expenses. This type of loan is typically repaid in full, along with interest and fees, on the borrower's next payday. 5. Consolidation Loan Agreement: This agreement is used when a borrower wishes to combine multiple outstanding debts into one loan, consolidating their debt obligations under a single payment plan. It helps simplify the repayment process and potentially lowers the interest rate. Regardless of the type of loan agreement, a Pennsylvania Loan Agreement for Personal Loan commonly includes the following key elements: 1. Identification of the parties involved, including their legal names and contact information. 2. Loan amount: The agreed amount of money the lender provides to the borrower. 3. Interest rate: The percentage charged on the loan amount as a fee for borrowing the funds. It typically depends on the borrower's creditworthiness and the prevailing market rates. 4. Repayment schedule: The loan agreement specifies the duration over which the borrower needs to repay the loan, including the frequency and amount of repayment installments. 5. Late payment penalties: These are outlined in case the borrower fails to make timely payments, including the consequences and fees associated with late or missed payments. 6. Default provisions: These stipulate the actions that can be taken by the lender in case of default, such as charging higher interest rates, demanding immediate repayment, or taking legal action. 7. Governing law: The loan agreement should state that it is governed by and subject to the laws of Pennsylvania. 8. Signatures: Both the lender and the borrower must sign the agreement to indicate their understanding and acceptance of the terms. It is important to note that while this article provides a general overview, seeking legal advice or consultation from a professional is highly recommended when drafting or entering into a Pennsylvania Loan Agreement for Personal Loan.

Pennsylvania Loan Agreement for Personal Loan

Description

How to fill out Pennsylvania Loan Agreement For Personal Loan?

If you want to complete, obtain, or printing lawful papers templates, use US Legal Forms, the most important collection of lawful kinds, which can be found on-line. Use the site`s simple and handy search to get the documents you require. Numerous templates for organization and person reasons are sorted by groups and suggests, or keywords. Use US Legal Forms to get the Pennsylvania Loan Agreement for Personal Loan in just a handful of clicks.

Should you be previously a US Legal Forms consumer, log in for your account and click the Acquire key to have the Pennsylvania Loan Agreement for Personal Loan. Also you can entry kinds you previously delivered electronically in the My Forms tab of your respective account.

If you are using US Legal Forms for the first time, refer to the instructions under:

- Step 1. Be sure you have chosen the shape to the right town/land.

- Step 2. Utilize the Review option to check out the form`s content material. Never overlook to see the information.

- Step 3. Should you be not satisfied together with the form, use the Lookup field on top of the display to get other variations of the lawful form template.

- Step 4. After you have located the shape you require, click the Get now key. Pick the pricing program you like and add your accreditations to sign up for the account.

- Step 5. Approach the transaction. You should use your bank card or PayPal account to finish the transaction.

- Step 6. Find the structure of the lawful form and obtain it on the gadget.

- Step 7. Complete, modify and printing or indicator the Pennsylvania Loan Agreement for Personal Loan.

Every lawful papers template you acquire is your own for a long time. You might have acces to every form you delivered electronically with your acccount. Select the My Forms portion and choose a form to printing or obtain once again.

Contend and obtain, and printing the Pennsylvania Loan Agreement for Personal Loan with US Legal Forms. There are thousands of specialist and condition-certain kinds you may use for your organization or person requires.