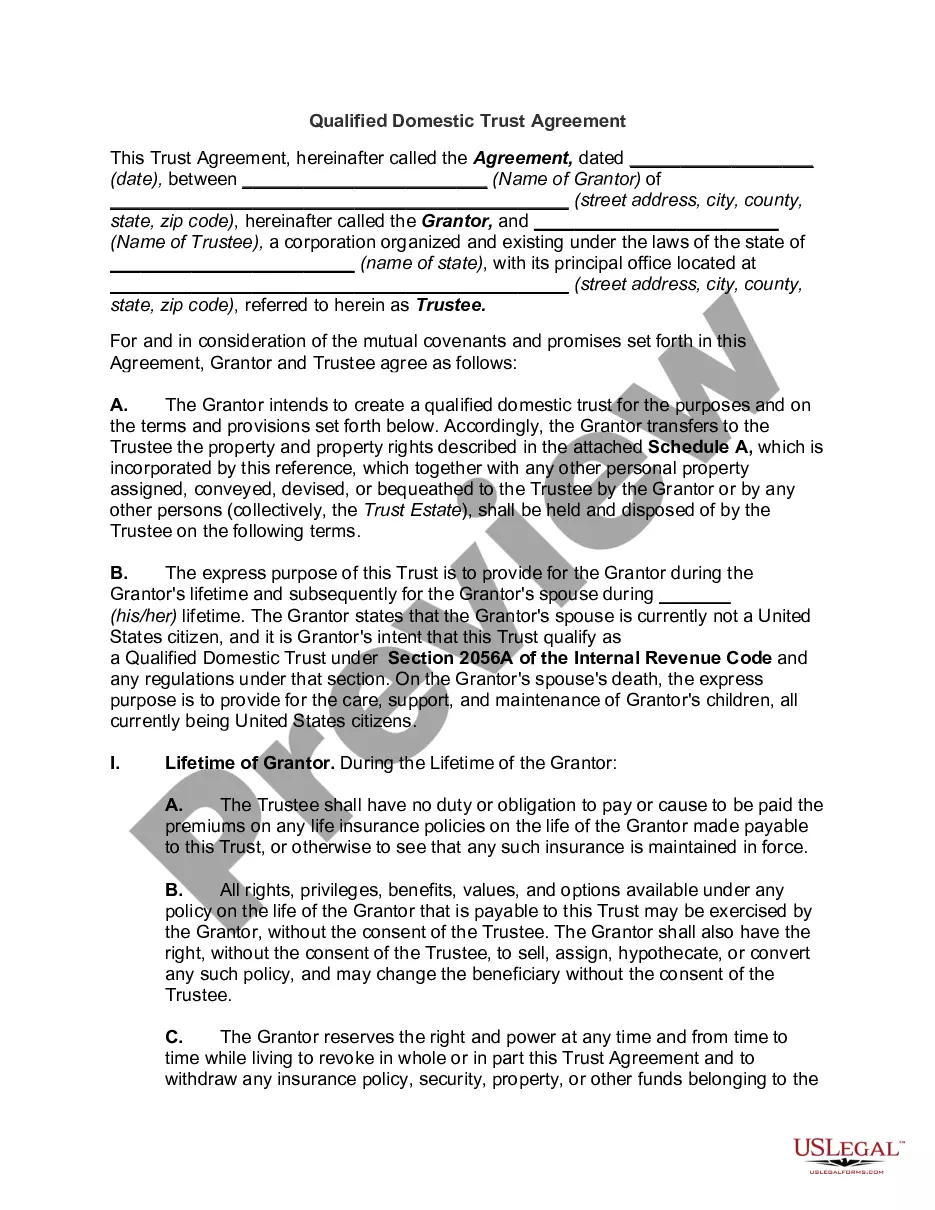

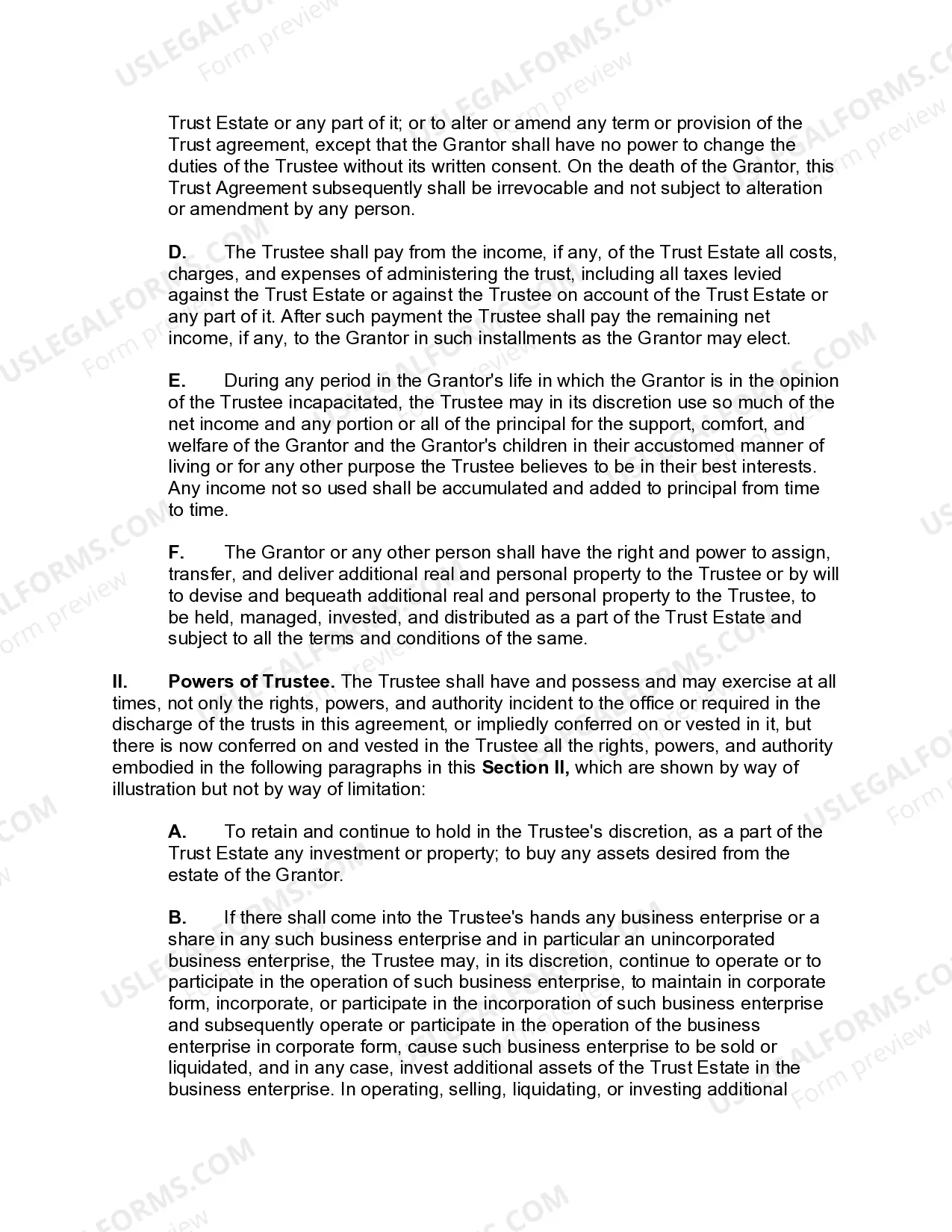

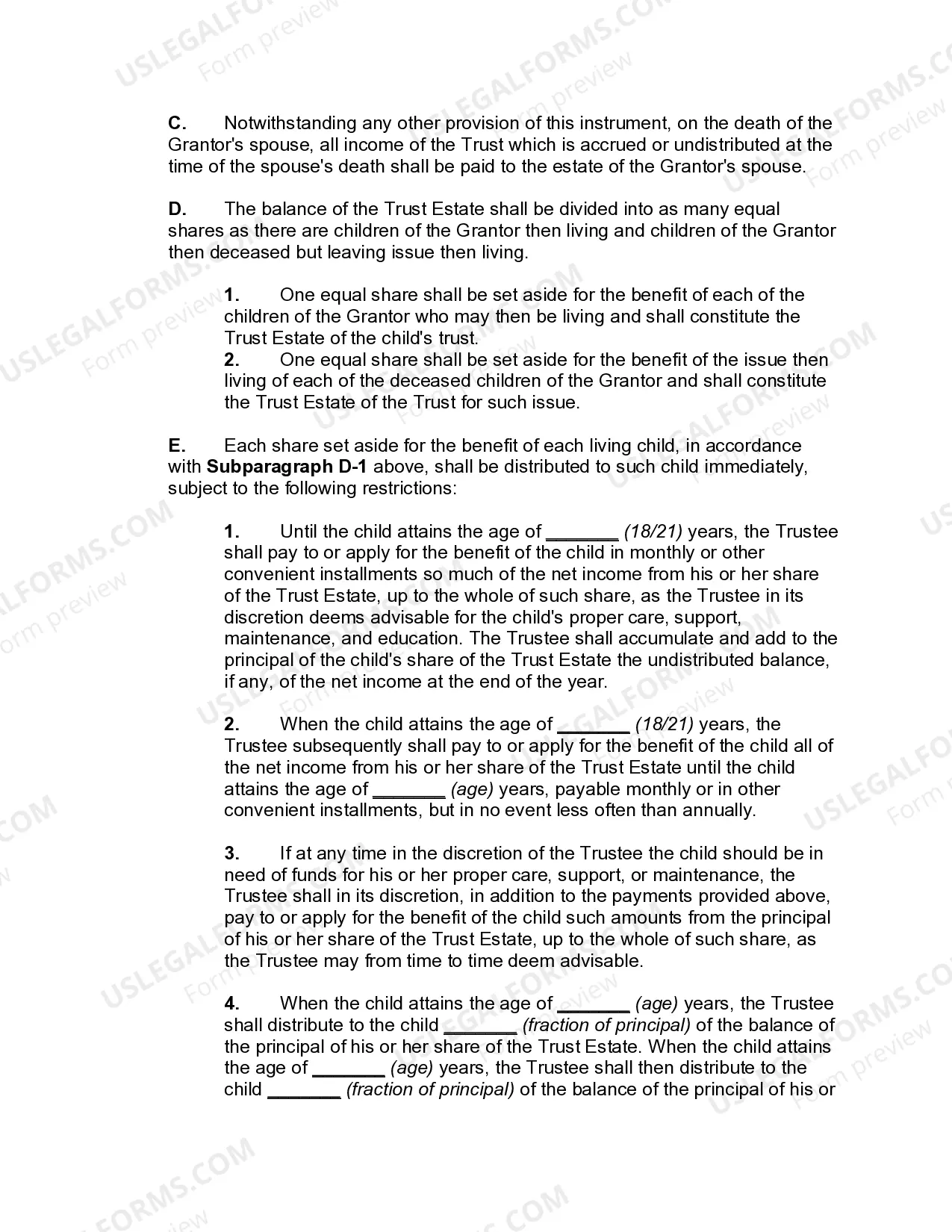

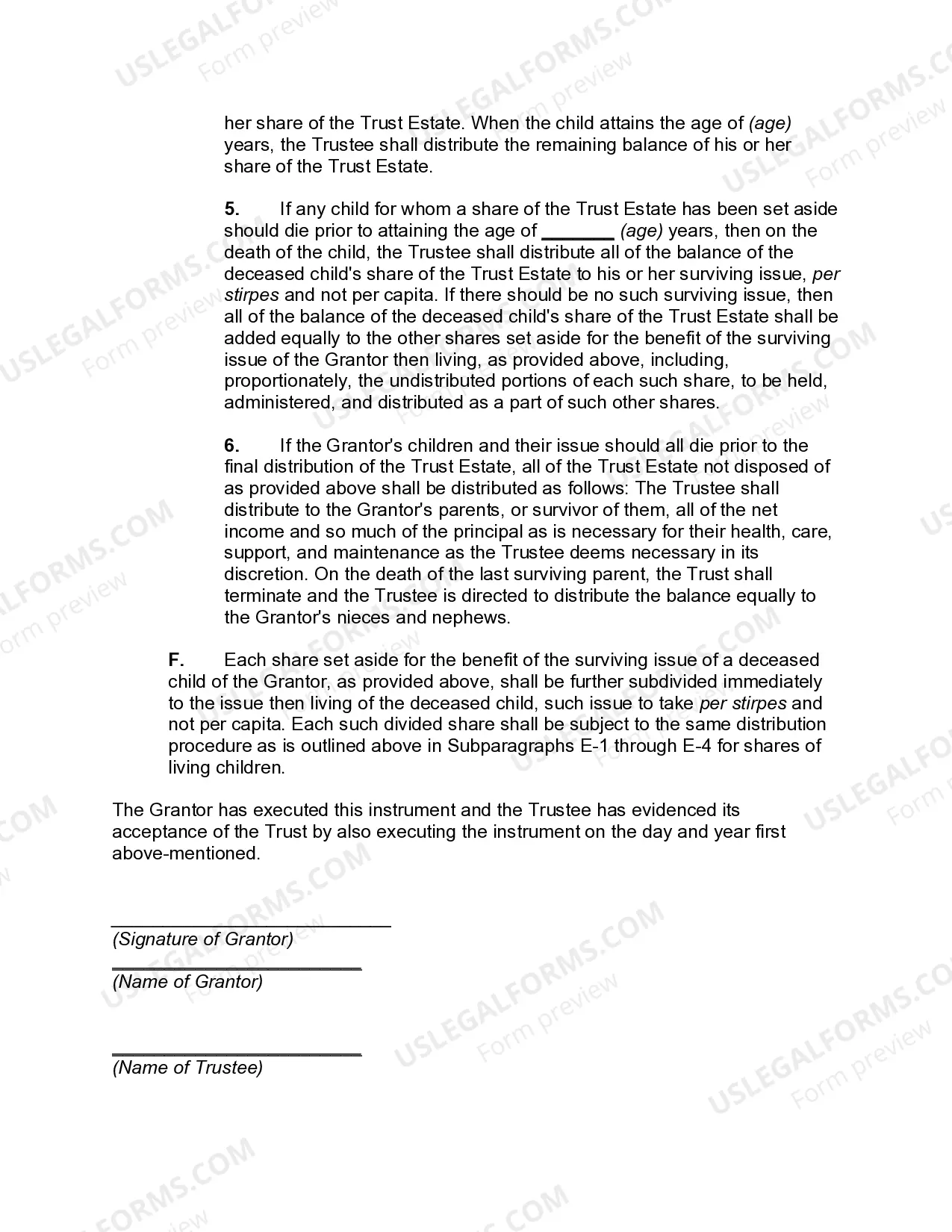

A Pennsylvania Qualified Domestic Trust Agreement (DOT) is a legal instrument designed to minimize estate taxes for non-U.S. citizen spouses residing in the state. Pennsylvania follows federal guidelines when it comes to Dots, which are subject to specific rules and regulations set forth by the Internal Revenue Service (IRS). A DOT serves as a specialized trust that allows a non-U.S. citizen spouse to qualify for the marital deduction in the event of the death of the U.S. citizen spouse. The marital deduction permits the transfer of an unlimited amount of assets from one spouse to another, free from estate and gift taxes. However, under normal circumstances, non-U.S. citizen individuals are not eligible for the marital deduction. To address this issue, the DOT was established, allowing the deferral of estate taxes until distributions are made from the trust. This deferral allows the non-U.S. citizen spouse to continue benefiting from the assets held within the trust during their lifetime. To qualify as a Pennsylvania DOT, certain conditions must be met. Firstly, the trust must meet the federal requirements outlined in the Internal Revenue Code Section 2056A. Some of these requirements include appointing a U.S. trustee or an executor responsible for overseeing the trust's administration and ensuring compliance with IRS regulations. Additionally, the DOT must maintain at least one U.S. based trustee or executor throughout its existence. This trustee must have the power to withhold and pay any applicable estate taxes on behalf of the trust and the non-U.S. citizen beneficiary. Furthermore, the trust must distribute only income to the non-U.S. citizen spouse during their lifetime, with no principal distributions unless certain exceptions apply. Pennsylvania provides a framework for two primary types of DOT arrangements. The first type is the Immediate DOT, which comes into effect immediately upon the death of the U.S. citizen spouse. The second type is the Look back DOT, which serves as an option for those who don't create an Immediate DOT but decide to establish one within six months of the U.S. citizen spouse's death. Both types aim to provide the necessary tax benefits and protection for the non-U.S. citizen spouse. In conclusion, a Pennsylvania Qualified Domestic Trust Agreement is a crucial estate planning tool for non-U.S. citizen spouses residing in Pennsylvania to minimize estate taxes upon the death of their U.S. citizen spouse. By adhering to federal regulations and appointing a U.S. trustee, a DOT allows the non-U.S. citizen spouse to qualify for the marital deduction and defer estate taxes. The two primary types of DOT arrangements in Pennsylvania are Immediate Dots and Look back Dots.

Pennsylvania Qualified Domestic Trust Agreement

Description

How to fill out Pennsylvania Qualified Domestic Trust Agreement?

Choosing the best lawful document design might be a struggle. Obviously, there are a lot of web templates available on the net, but how would you discover the lawful form you require? Take advantage of the US Legal Forms internet site. The services offers a huge number of web templates, including the Pennsylvania Qualified Domestic Trust Agreement, which you can use for organization and personal demands. All the forms are checked out by professionals and meet up with federal and state specifications.

If you are currently listed, log in in your bank account and then click the Download option to obtain the Pennsylvania Qualified Domestic Trust Agreement. Utilize your bank account to search with the lawful forms you may have purchased earlier. Check out the My Forms tab of your own bank account and get one more duplicate in the document you require.

If you are a new end user of US Legal Forms, allow me to share basic recommendations for you to comply with:

- Initially, make certain you have selected the correct form for your personal city/region. You may check out the shape making use of the Review option and study the shape explanation to guarantee it is the best for you.

- If the form will not meet up with your preferences, make use of the Seach industry to find the proper form.

- When you are certain the shape is suitable, click on the Purchase now option to obtain the form.

- Pick the rates strategy you would like and enter the needed information and facts. Create your bank account and pay money for the transaction using your PayPal bank account or Visa or Mastercard.

- Select the submit format and obtain the lawful document design in your product.

- Complete, revise and produce and sign the received Pennsylvania Qualified Domestic Trust Agreement.

US Legal Forms is the largest library of lawful forms that you can find numerous document web templates. Take advantage of the company to obtain expertly-produced documents that comply with express specifications.