Pennsylvania Qualified Personal Residence Trust One Term Holder

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Qualified Personal Residence Trust One Term Holder?

It is feasible to spend numerous hours online trying to locate the legal document template that meets the federal and state requirements you need.

US Legal Forms offers a vast selection of legal documents that are reviewed by experts.

You can conveniently download or print the Pennsylvania Qualified Personal Residence Trust One Term Holder from the service.

Read the form description to ensure you have chosen the right document. If available, utilize the Review button to examine the document template as well.

- If you already possess a US Legal Forms account, you can Log In and then click the Download button.

- Next, you can complete, modify, print, or sign the Pennsylvania Qualified Personal Residence Trust One Term Holder.

- Every legal document template you acquire is yours permanently.

- To obtain another copy of any purchased document, go to the My documents section and click the appropriate button.

- If you are visiting the US Legal Forms website for the first time, follow the straightforward instructions outlined below.

- First, verify that you have selected the correct document template for the area or city you choose.

Form popularity

FAQ

Because there's no limit on how long the QPRT must run, it's not uncommon to see QPRTs that were created 10 to 15 years ago finally expire today.

Unwinding a QPRT All you have to do is enter into a lease agreement that pays fair market rent. After the QPRT expiration term, the grantor must pay rent if they continue to reside in the property.

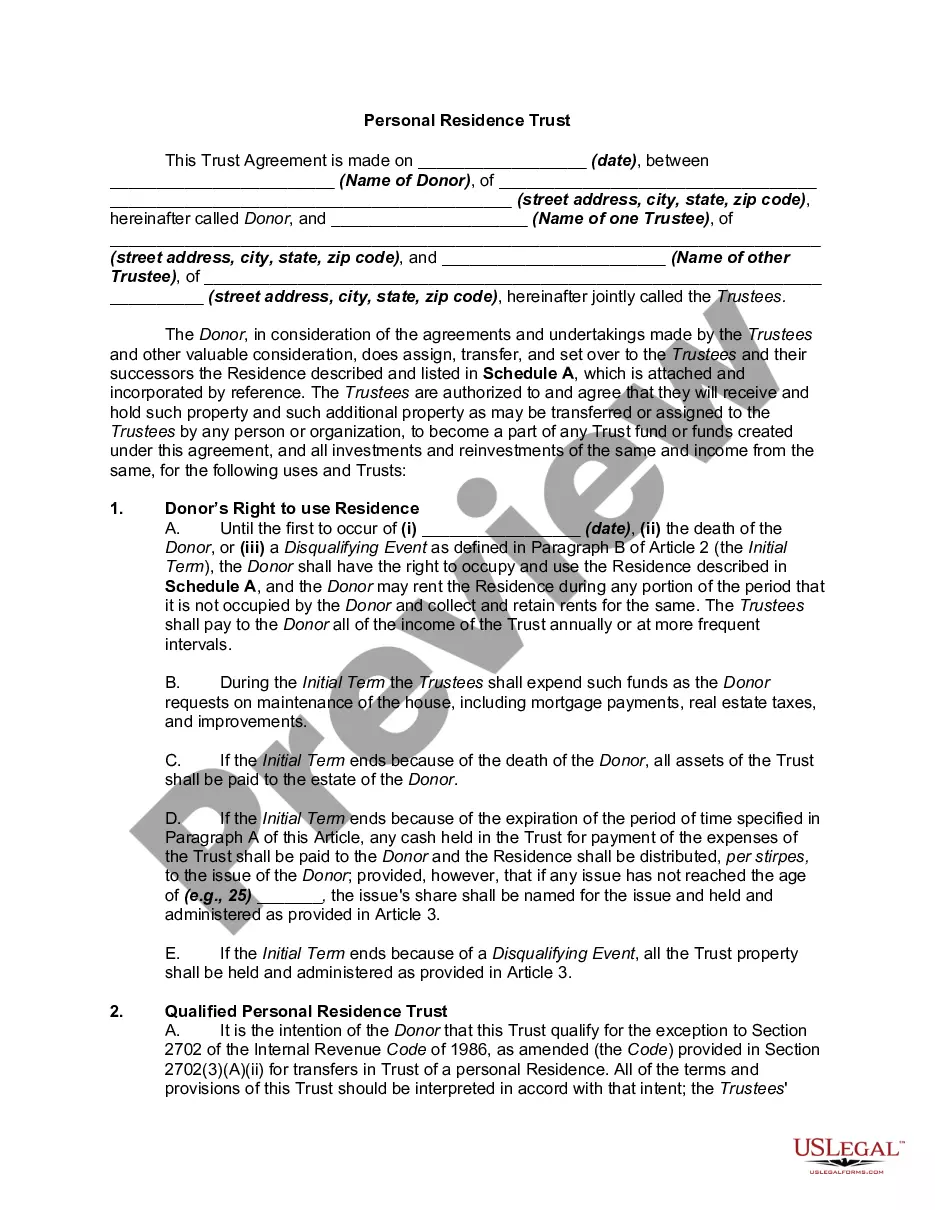

The Qualified Personal Residence Trust offers the benefits of a trust to protect a residence. At the same time, the owner can still live in the house while the trust is in effect. This means while the residence is held within the QPRT it is protected from judgments and creditors.

The biggest benefit of a QPRT is that it removes the value of your primary or second home and its appreciation from your taxable estate. Continued use of the property. With your home in a QPRT, you can still live in the property rent-free and enjoy any income tax deductions associated with it. Gift tax benefits.

A qualified personal residence trust (QPRT) is a trust to which a person (called the settlor, donor, or grantor) transfers his personal residence. The grantor reserves the right to live in the house for a period of years; this retained interest reduces the current value of the gift for gift tax purposes.

There are two options upon early termination. The trust agreement may allow that the trust will terminate and the property or its sales proceeds be given back to you.

The biggest benefit of a QPRT is that it removes the value of your primary or second home and its appreciation from your taxable estate. Continued use of the property. With your home in a QPRT, you can still live in the property rent-free and enjoy any income tax deductions associated with it.

One of the most important steps for the trustee to follow at the end of the QPRT term is to transfer title and ownership of the residence into the names of the remainder beneficiaries to ensure the correct titling and insuring of the asset.

What are the Disadvantages of a Trust?Costs. When a decedent passes with only a will in place, the decedent's estate is subject to probate.Record Keeping. It is essential to maintain detailed records of property transferred into and out of a trust.No Protection from Creditors.

A qualified personal residence trust (QPRT) is a specific type of irrevocable trust that allows its creator to remove a personal home from their estate for the purpose of reducing the amount of gift tax that is incurred when transferring assets to a beneficiary.