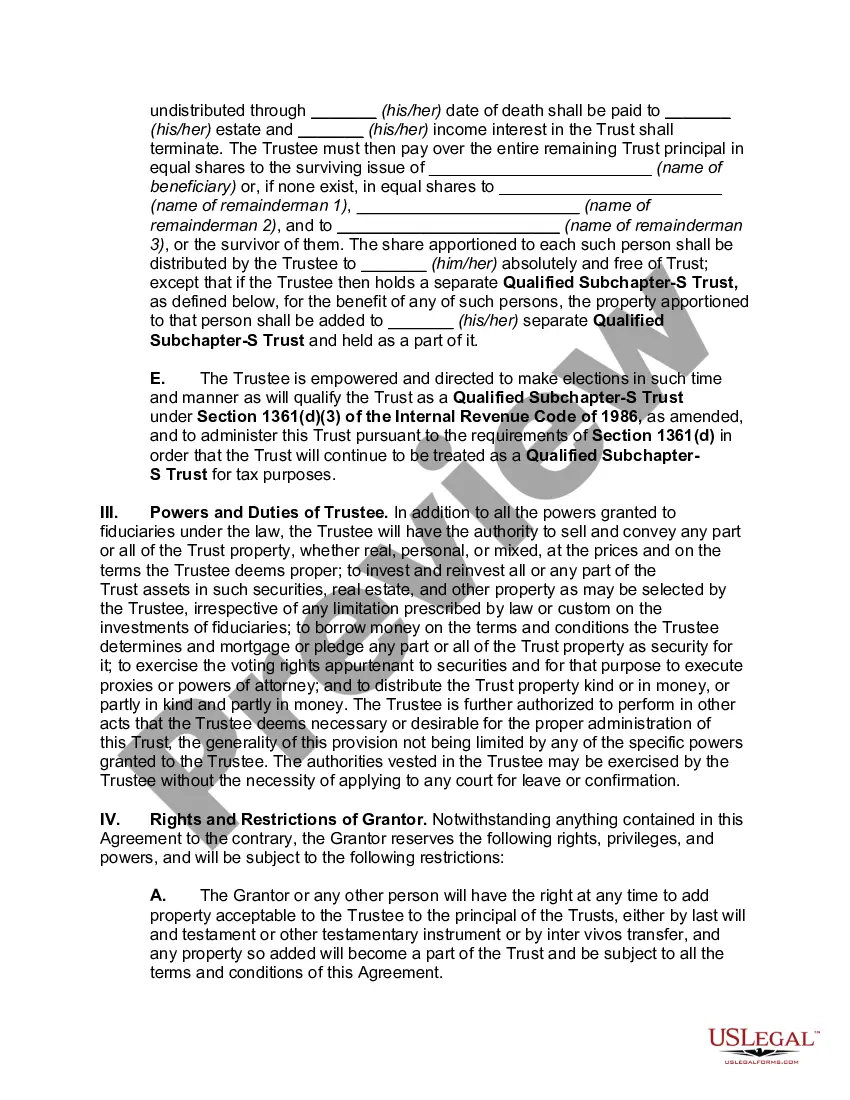

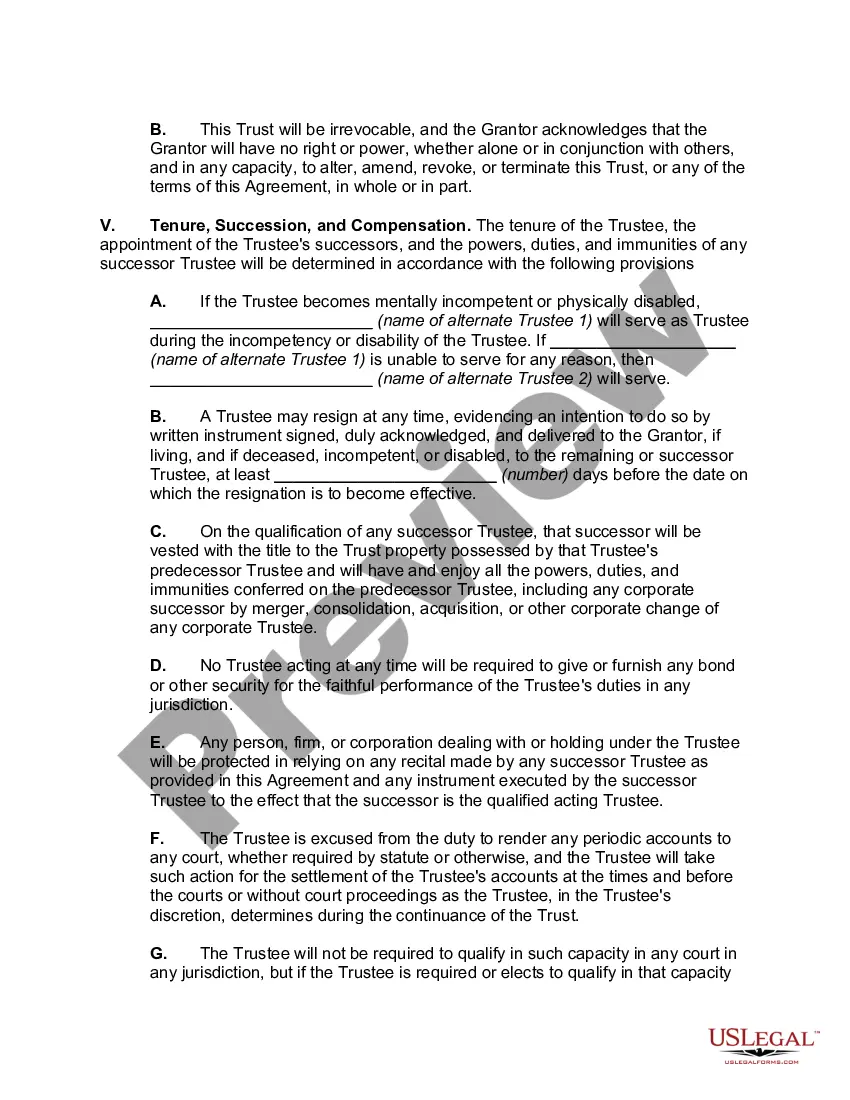

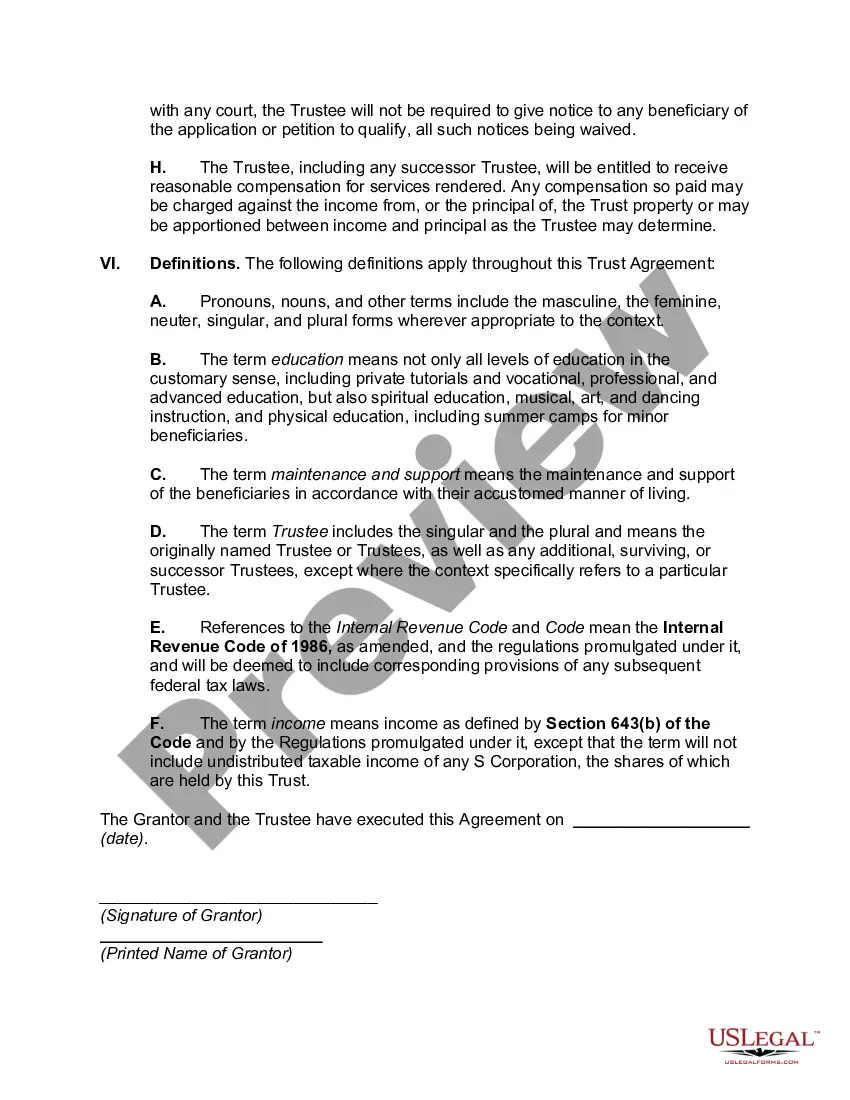

A Pennsylvania Irrevocable Trust, also known as a Qualifying Subchapter-S Trust (SST), is a type of trust established in the state of Pennsylvania that meets specific criteria set forth by the Internal Revenue Code (IRC). It is designed to provide tax advantages for beneficiaries who are shareholders of an S Corporation. Under the IRC, an SST must satisfy certain conditions to qualify for tax treatment as an S Corporation shareholder. The trust must be irrevocable, meaning it cannot be changed or revoked once established. Additionally, the trust must have only one primary beneficiary who is an individual and holds a current income interest in the trust. It is crucial to note that in Pennsylvania, there is currently no specific designation for an SST as per the state laws. However, to comply with federal tax regulations, Pennsylvania residents may establish a trust that meets the SST requirements outlined by the IRC. There are no distinct variations of Pennsylvania Irrevocable/Qualifying Subchapter-S Trusts, as any trust that meets the criteria set by the IRC can be considered a qualifying SST. The main objective of such trusts is to facilitate the transfer of shares in an S Corporation to eligible beneficiaries while mitigating certain tax obligations. By creating an SST, the trust creator (granter) can ensure that the income generated by the S Corporation is passed through to the trust beneficiary and taxed at their individual tax rate. This approach can be advantageous, particularly for beneficiaries who are in lower tax brackets compared to the trust's original creator. In summary, a Pennsylvania Irrevocable Trust, or SST, is a trust designed to meet the IRC requirements for tax treatment as an S Corporation shareholder. Although there are no specific variations of this trust under Pennsylvania law, individuals residing in the state can create an irrevocable trust that satisfies the SST criteria outlined by the IRS. This trust structure allows for efficient transfer of S Corporation shares and potential tax advantages for beneficiaries.

Pennsylvania Irrevocable Trust which is a Qualifying Subchapter-S Trust

Description

How to fill out Pennsylvania Irrevocable Trust Which Is A Qualifying Subchapter-S Trust?

US Legal Forms - one of many largest libraries of legitimate kinds in America - offers a wide array of legitimate papers layouts you may acquire or print out. While using internet site, you will get a large number of kinds for company and personal functions, sorted by classes, claims, or keywords.You will find the latest variations of kinds like the Pennsylvania Irrevocable Trust which is a Qualifying Subchapter-S Trust within minutes.

If you already possess a membership, log in and acquire Pennsylvania Irrevocable Trust which is a Qualifying Subchapter-S Trust from the US Legal Forms catalogue. The Acquire option will show up on every single type you see. You have access to all formerly downloaded kinds inside the My Forms tab of the account.

If you wish to use US Legal Forms initially, allow me to share easy instructions to help you get started off:

- Be sure to have chosen the right type for your metropolis/region. Go through the Review option to review the form`s information. Browse the type explanation to ensure that you have selected the correct type.

- In the event the type does not fit your specifications, use the Research industry at the top of the screen to get the one which does.

- When you are satisfied with the shape, verify your selection by visiting the Purchase now option. Then, select the costs program you prefer and supply your credentials to register for an account.

- Process the financial transaction. Utilize your bank card or PayPal account to finish the financial transaction.

- Choose the file format and acquire the shape on your own system.

- Make adjustments. Complete, change and print out and indicator the downloaded Pennsylvania Irrevocable Trust which is a Qualifying Subchapter-S Trust.

Each and every format you added to your money does not have an expiration particular date and is your own for a long time. So, if you want to acquire or print out another backup, just go to the My Forms area and then click about the type you require.

Get access to the Pennsylvania Irrevocable Trust which is a Qualifying Subchapter-S Trust with US Legal Forms, probably the most comprehensive catalogue of legitimate papers layouts. Use a large number of specialist and condition-distinct layouts that fulfill your small business or personal requires and specifications.