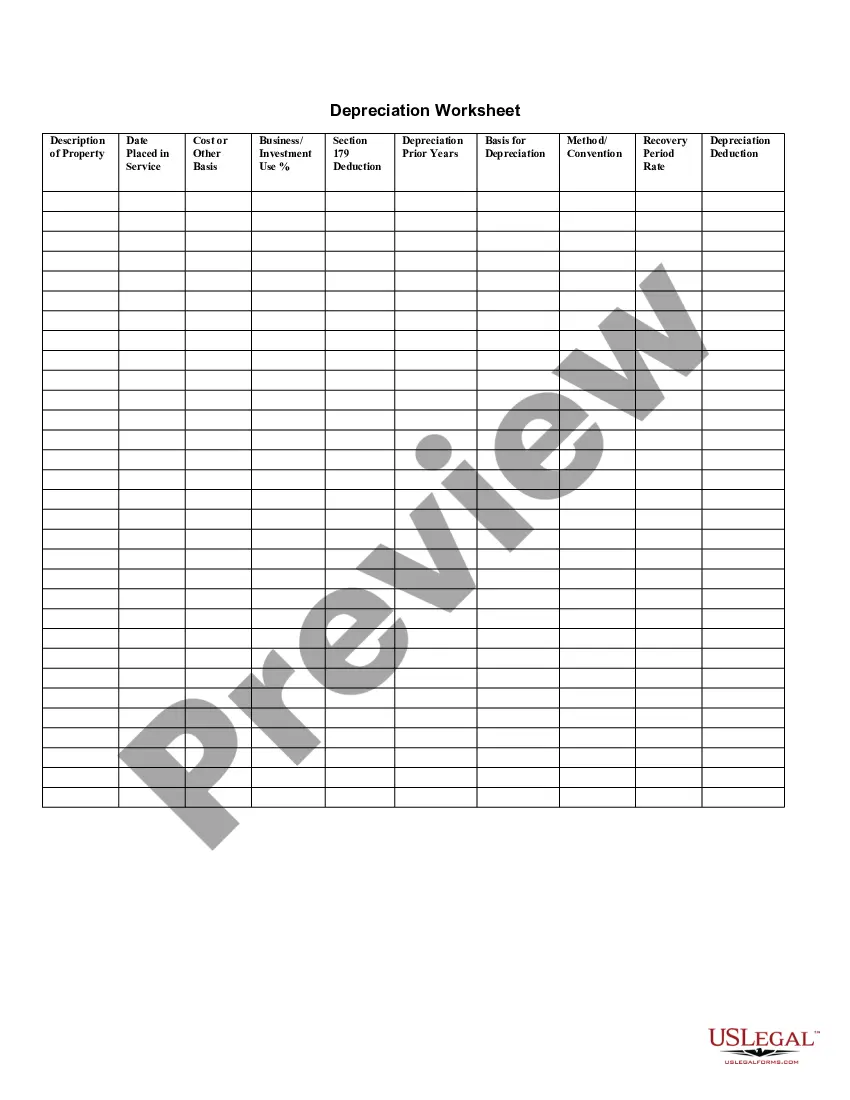

Pennsylvania Depreciation Schedule

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Depreciation Schedule?

Selecting the appropriate authorized document format can be challenging.

Clearly, there are numerous templates accessible online, but how can you find the legal form you need.

Utilize the US Legal Forms website. This service offers thousands of templates, including the Pennsylvania Depreciation Schedule, suitable for both business and personal use.

You can review the form using the Review button and examine the form description to confirm it is the right one for you.

- All forms are reviewed by experts and comply with state and federal regulations.

- If you are already registered, sign in to your account and click the Obtain button to download the Pennsylvania Depreciation Schedule.

- Use your account to view the legal forms you have previously purchased.

- Visit the My documents section of your account to download another copy of the documents you need.

- If you are a new user of US Legal Forms, here are simple steps for you to follow.

- First, ensure you have selected the correct form for your region/county.

Form popularity

FAQ

State Conformity with Federal Section 179Forty-six states allow Section 179 deductions. Of the remaining four, three do not levy corporate income taxes and the fourth (Ohio) does not make allowances for federal expense deductions against its gross receipts tax.

By statute, Pennsylvania does not conform to federal bonus depreciation under IRC § 168(k). Rather, Pennsylvania decouples from federal bonus depreciation by making additions to and subtractions from taxable income.

For Pennsylvania personal income tax purposes, taxpayer has an allowable Section 179 deduction of $20,000 in Tax Year 1. The $5,000 in unused Section 179 expense creates a PIT loss, and is not carried forward to future tax years.

By statute, Pennsylvania does not conform to federal bonus depreciation under IRC § 168(k). Rather, Pennsylvania decouples from federal bonus depreciation by making additions to and subtractions from taxable income.

No loss: Stricken by the Pennsylvania Supreme Court, the NOL deduction nevertheless is allowed.

The Pennsylvania Department of Revenue does not follow the federal tax benefit rule. For tax benefit rules, Pennsylvania law requires depreciation to be computed under the straight-line method even if the depreciation did not provide any tax benefit.

Pennsylvania Governor Tom Wolf signed Act 72 of 2018 (available here) into law yesterday. Act 72 will allow Pennsylvania corporate net income tax (CNIT) taxpayers to use the federal Modified Accelerated Cost Recovery System (MACRS), but not federal bonus depreciation.

PA Schedule C - Profit or Loss from Business or Profession (Sole Proprietorship) (PA-40 C)

Yes. The calculation of PA Corporate Net Income begins with taxable income as reported to the IRS, on a separate company basis, or would have been reported to IRS had the taxpayer been required to...

Use Schedule C (Form 1040) to report income or loss from a business you operated or a profession you practiced as a sole proprietor. An activity qualifies as a business if: Your primary purpose for engaging in the activity is for income or profit. You are involved in the activity with continuity and regularity.