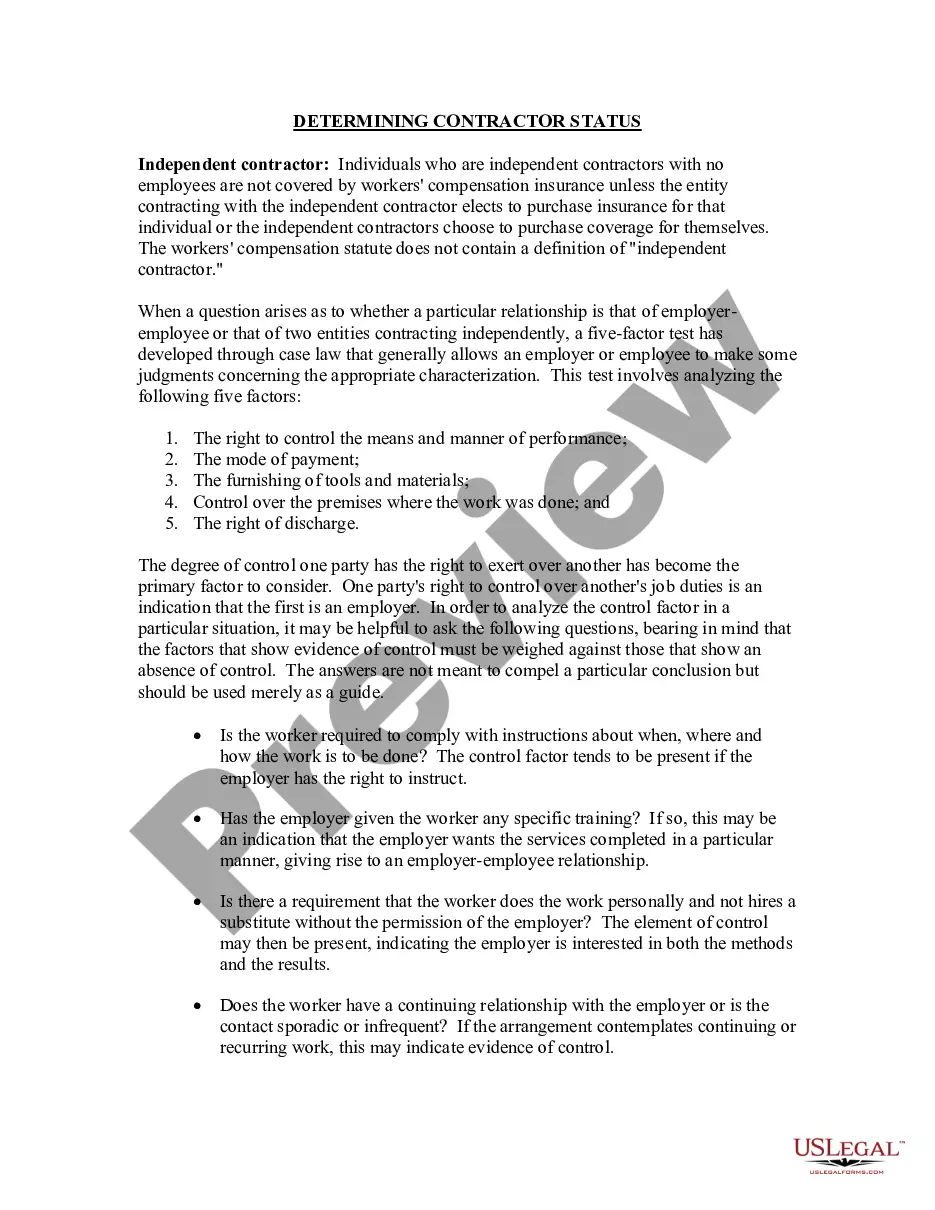

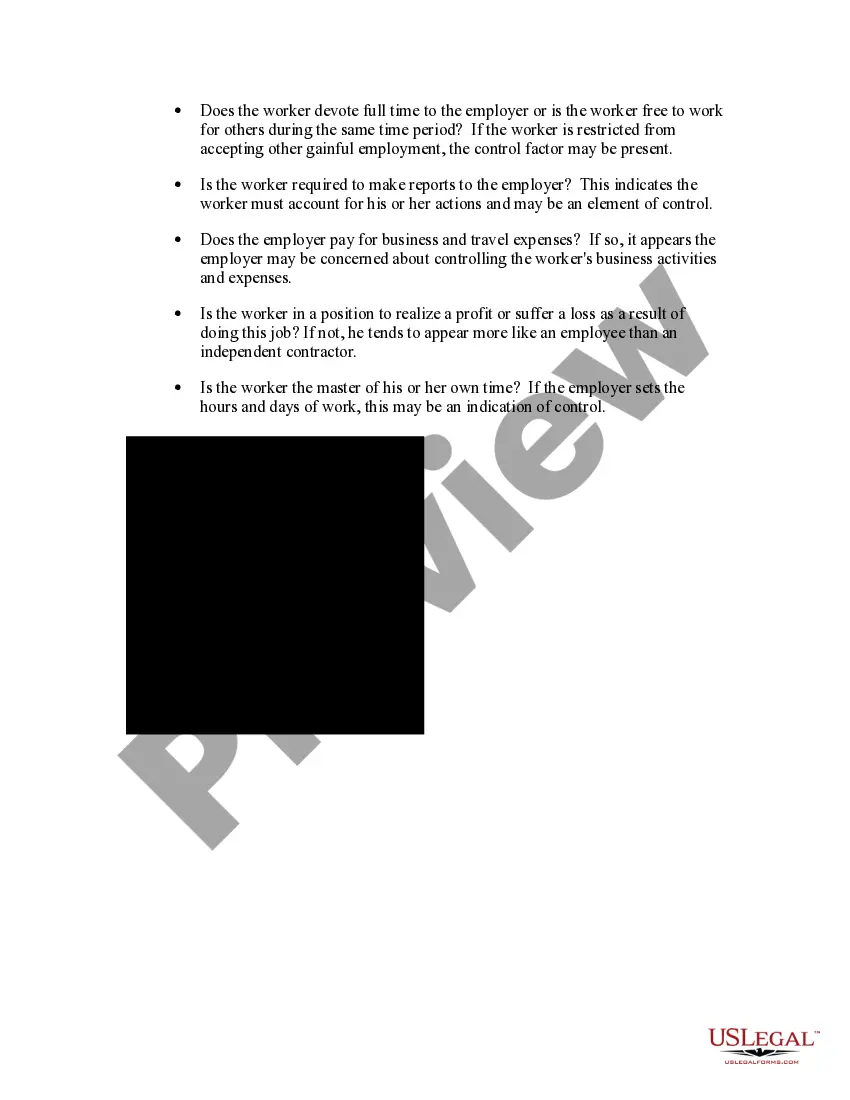

Pennsylvania Determining Self-Employed Contractor Status: A Comprehensive Guide Determining self-employed contractor status in Pennsylvania is essential for both businesses and individuals engaging in independent contractor work. This determination helps establish the appropriate tax obligations, legal rights, and responsibilities for both parties involved. Understanding the criteria and factors considered by the Pennsylvania Department of Labor and Industry (DLI) is crucial in ensuring compliance with state regulations and avoiding misclassification issues. When assessing self-employed contractor status in Pennsylvania, several fundamental factors are considered. These factors help determine the degree of control exercised by the hiring entity over the work performed, the individual's independence, and the overall nature of the working relationship. Key aspects include: 1. Behavioral Control: This involves examining whether the hiring entity has the right to direct and control the individual's work performance. Factors considered include instructions given, training provided, methods of evaluation, and specific job requirements. 2. Financial Control: The financial aspects primarily revolve around analyzing the business aspects of the individual's work. Factors considered include the extent of the individual's investment, opportunity for profit or loss, method of payment, provision of tools and equipment, and reimbursement of business expenses. 3. Relationship Type: The nature of the relationship between the hiring entity and the individual is assessed, focusing on the existence of a written contract, employee benefits, permanency of the working relationship, and the extent to which services are essential to the hiring entity's regular operations. Pennsylvania further distinguishes between various types of self-employed contractors based on the specific industry they operate in. While the core determining factors remain the same, the applications may vary slightly. Some common types of self-employed contractor statuses in Pennsylvania include: 1. Construction Contractors: Pennsylvania classifies individuals working in construction-related fields, such as general contractors, subcontractors, or independent tradespeople, who perform specialized work, e.g., electrical or plumbing, under self-employed contractor status. 2. Professional Service Providers: Individuals providing professional services, such as doctors, lawyers, architects, or engineers, are often considered self-employed contractors. Although their occupation is typically highly specialized and requires advanced education, they frequently operate as independent contractors. 3. Gig Economy Workers: With the rise of the gig economy, individuals working in app-based services, such as ride-share drivers, food delivery workers, or freelance digital platform operators, can also fall under the self-employed contractor status. Proper classification is crucial in determining their rights and benefits under Pennsylvania law. It is important for businesses and individuals engaging in self-employment arrangements to thoroughly understand Pennsylvania's criteria for determining self-employed contractor status. Misclassification can lead to severe legal and financial consequences, including tax liabilities, labor law violations, and potential lawsuits. Seeking professional advice from legal or tax experts can help ensure compliance and mitigate any risks associated with misclassification. In summary, Pennsylvania's determination of self-employed contractor status involves evaluating several factors related to behavioral and financial control and the overall nature of the working relationship. Construction contractors, professional service providers, and gig economy workers are some common examples of self-employed contractors in the state.

Pennsylvania Determining Self-Employed Contractor Status

Description

How to fill out Pennsylvania Determining Self-Employed Contractor Status?

You can devote hours online trying to find the lawful record web template that suits the federal and state requirements you will need. US Legal Forms provides thousands of lawful forms which can be reviewed by pros. You can actually down load or print out the Pennsylvania Determining Self-Employed Contractor Status from my service.

If you have a US Legal Forms profile, it is possible to log in and then click the Acquire switch. Following that, it is possible to comprehensive, revise, print out, or sign the Pennsylvania Determining Self-Employed Contractor Status. Each and every lawful record web template you purchase is your own property permanently. To get an additional duplicate for any obtained kind, visit the My Forms tab and then click the corresponding switch.

If you are using the US Legal Forms site the very first time, keep to the straightforward directions below:

- Very first, make sure that you have chosen the proper record web template for the county/city of your choice. Look at the kind outline to make sure you have picked the appropriate kind. If readily available, utilize the Review switch to search with the record web template also.

- In order to find an additional variation in the kind, utilize the Research discipline to obtain the web template that meets your needs and requirements.

- When you have discovered the web template you would like, simply click Get now to carry on.

- Pick the rates strategy you would like, key in your accreditations, and sign up for an account on US Legal Forms.

- Complete the deal. You may use your charge card or PayPal profile to cover the lawful kind.

- Pick the structure in the record and down load it for your product.

- Make adjustments for your record if required. You can comprehensive, revise and sign and print out Pennsylvania Determining Self-Employed Contractor Status.

Acquire and print out thousands of record layouts making use of the US Legal Forms web site, which offers the greatest selection of lawful forms. Use professional and state-distinct layouts to deal with your business or specific demands.