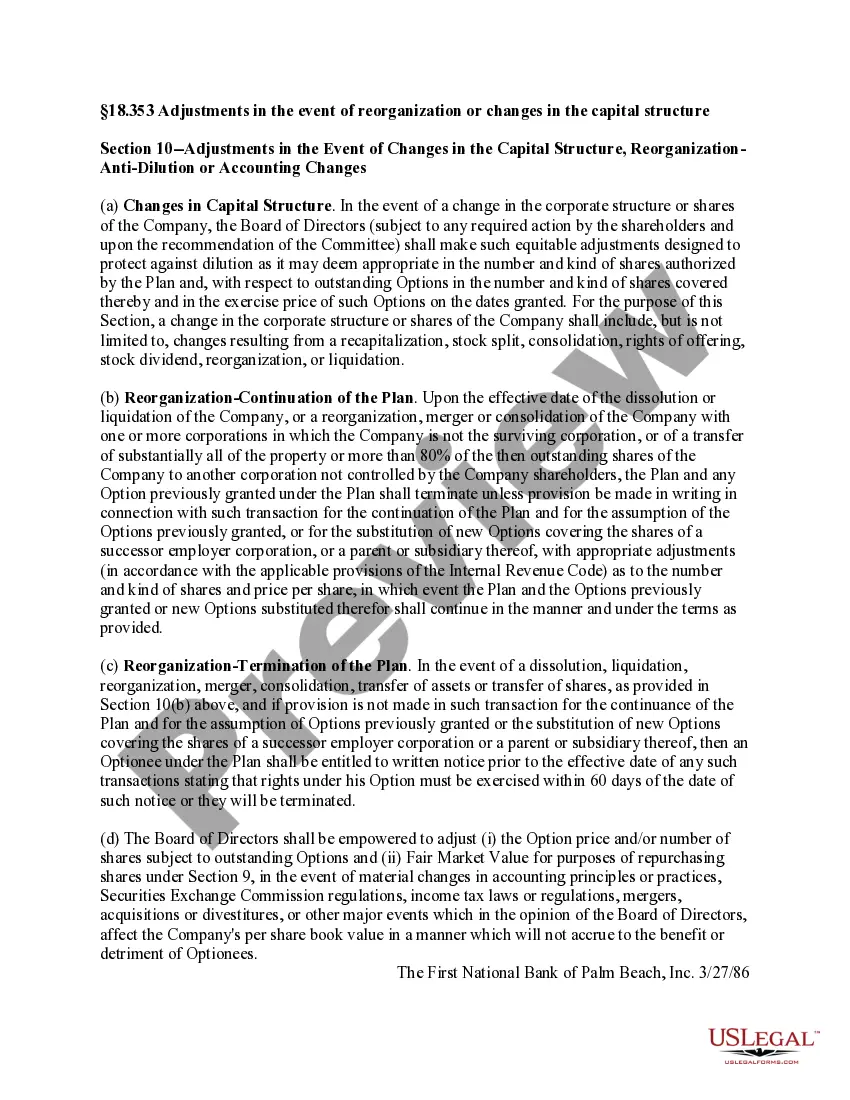

Pennsylvania Adjustments in the Event of Reorganization or Changes in the Capital Structure: Understanding the Mechanics In the context of corporate finance and business operations, Pennsylvania Adjustments play a crucial role in managing reorganizations or changes in a company's capital structure. These adjustments refer to specific actions taken by businesses to comply with regulatory requirements or optimize their financial standing during transformative events. They are key tools employed to ensure transparency, fairness, and stability throughout the process. In this detailed description, we will explore the various types of Pennsylvania Adjustments that organizations may encounter when undergoing reorganizations or changes in their capital structure. 1. Recapitalization Adjustments: Recapitalization refers to the process of restructuring a firm's debt or equity mix, usually aimed at improving the organization's financial health. Pennsylvania Adjustments in this scenario involve altering the firm's capital structure by issuing new securities (such as shares or bonds), buying back existing securities, or altering the terms of existing securities. 2. Debt Restructuring Adjustments: Debt restructuring refers to modifying the terms and conditions of existing debts to alleviate financial distress or enable smoother operations. Pennsylvania Adjustments within this category may include renegotiating interest rates, extending payment terms, deferring principal payment, or converting certain types of debt into equity. 3. Mergers and Acquisitions (M&A) Adjustments: During M&A transactions, businesses may undergo fundamental changes in their capital structure. Pennsylvania Adjustments are essential to ensure proper financing integration and legal compliance. These adjustments can involve aligning the capital structures of merging entities, modifying debt obligations, or revising equity ownership stakes to reflect the new organizational setup. 4. Equity Offerings or Issuance Adjustments: When a company decides to raise additional funds by offering new shares to the public or private investors, Pennsylvania Adjustments may be necessary. These adjustments may involve updating financial statements, calculating new valuation metrics, and ensuring compliance with regulatory frameworks, such as maintaining sufficient financial disclosure requirements. 5. Stock Split or Reverse Stock Split Adjustments: To manage changes in share prices and encourage market participation, organizations may undertake stock splits or reverse stock splits. Pennsylvania Adjustments in these cases include adjusting the capital structure, recalculating equity proportions, and ensuring accurate accounting for the revised number of outstanding shares. 6. Bankruptcy or Insolvency Adjustments: In unfortunate instances, companies facing financial distress might resort to bankruptcy or insolvency procedures. Pennsylvania Adjustments in these scenarios typically focus on apportioning assets, satisfying creditors, and managing reorganization plans while adhering to the relevant bankruptcy laws. These adjustments aim to achieve an equitable distribution of resources among stakeholders and facilitate the company's revival or liquidation. 7. Reporting and Disclosure Adjustments: During any reorganization or changes in the capital structure, Pennsylvania Adjustments may also involve ensuring accurate, transparent, and timely financial reporting. Companies need to disclose the impact of these adjustments on their financial statements, emphasizing any material changes to the capital structure, debt obligations, equity ownership, or financial ratios. Within the vast domain of reorganization or changes in the capital structure, these various types of Pennsylvania Adjustments exemplify the intricacies involved. By appropriately navigating and implementing these adjustments, businesses can effectively manage their financial affairs, optimize stakeholder value, and maintain regulatory compliance. Understanding these adjustments and their implications is crucial for organizations and professionals in the field of corporate finance, ensuring smooth transitions and stability during transformative events.

Pennsylvania Adjustments in the event of reorganization or changes in the capital structure

Description

How to fill out Pennsylvania Adjustments In The Event Of Reorganization Or Changes In The Capital Structure?

US Legal Forms - one of many largest libraries of legal types in the States - delivers a variety of legal record layouts you can obtain or printing. Making use of the site, you can get thousands of types for business and specific functions, categorized by classes, suggests, or key phrases.You will find the latest models of types like the Pennsylvania Adjustments in the event of reorganization or changes in the capital structure within minutes.

If you already possess a subscription, log in and obtain Pennsylvania Adjustments in the event of reorganization or changes in the capital structure in the US Legal Forms library. The Obtain button will appear on each and every form you view. You have access to all previously saved types inside the My Forms tab of your own account.

If you wish to use US Legal Forms for the first time, allow me to share straightforward directions to obtain started out:

- Make sure you have picked the best form to your area/state. Click on the Preview button to analyze the form`s articles. See the form explanation to actually have chosen the proper form.

- If the form does not fit your demands, take advantage of the Lookup industry towards the top of the display to get the the one that does.

- Should you be pleased with the shape, verify your option by clicking on the Buy now button. Then, choose the pricing strategy you prefer and offer your credentials to sign up for the account.

- Process the deal. Make use of credit card or PayPal account to perform the deal.

- Select the file format and obtain the shape on your product.

- Make alterations. Fill up, revise and printing and signal the saved Pennsylvania Adjustments in the event of reorganization or changes in the capital structure.

Every single design you included with your bank account does not have an expiration date and is also your own permanently. So, if you want to obtain or printing one more duplicate, just visit the My Forms portion and click on about the form you will need.

Gain access to the Pennsylvania Adjustments in the event of reorganization or changes in the capital structure with US Legal Forms, the most extensive library of legal record layouts. Use thousands of specialist and state-specific layouts that fulfill your company or specific demands and demands.

Form popularity

FAQ

Capital losses may be used to offset capital gains. If the losses exceed the gains, up to $3,000 of those losses may be used to offset the taxes on other kinds of income.

--Unless otherwise restricted in the bylaws, any action required or permitted to be taken at a meeting of the shareholders or of a class of shareholders of a business corporation may be taken without a meeting if a consent or consents to the action in record form are signed, before, on or after the effective date of ...

PA also does not allow you to offset other income with a capital loss. (Can't offset wages with capital loss). So you report it, but if the total of all gains & losses is a negative, the loss does not effect your taxes. However, if the total of all capital gains & losses is a positive (gain), it is taxable by PA.

If you have an overall net capital loss for the year, you can deduct up to $3,000 of that loss against other kinds of income, including your salary and interest income.

(b) Action by consent. --Unless otherwise restricted in the bylaws, any action required or permitted to be approved at a meeting of the directors may be approved without a meeting by a consent or consents to the action in record form.

If you suffer a loss on the sale of an asset (a capital loss), you can set this loss off against any profits made on the sale of other assets (capital profits) in the same tax year. You may also be able to set this loss off against capital profits made in future years.

If your capital losses are greater than your capital gains, or if you make a capital loss in a financial year in which you don't make a capital gain, you can generally carry the capital loss forward and deduct it against any capital gains you make in future years.

Title 15 - CORPORATIONS AND UNINCORPORATED ASSOCIATIONS.