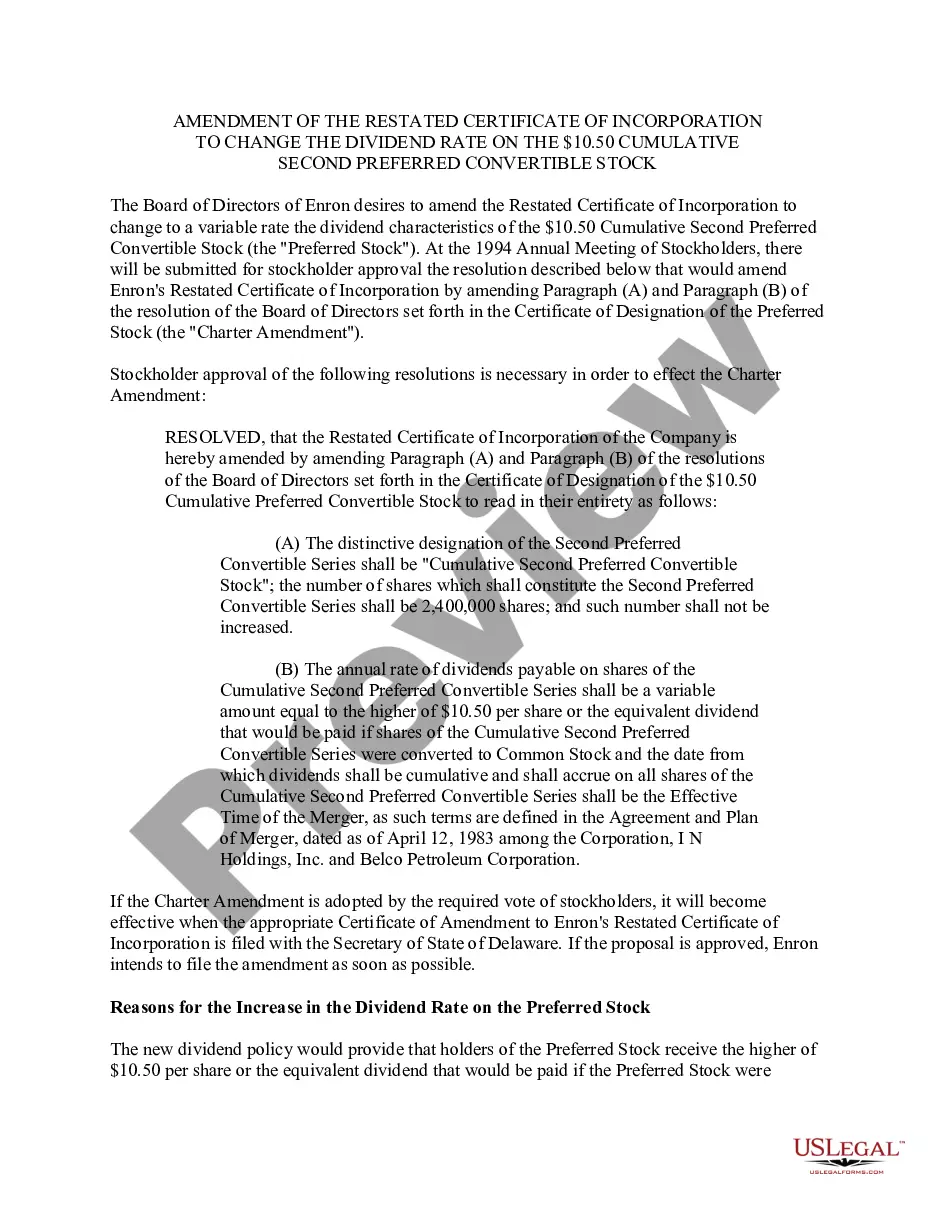

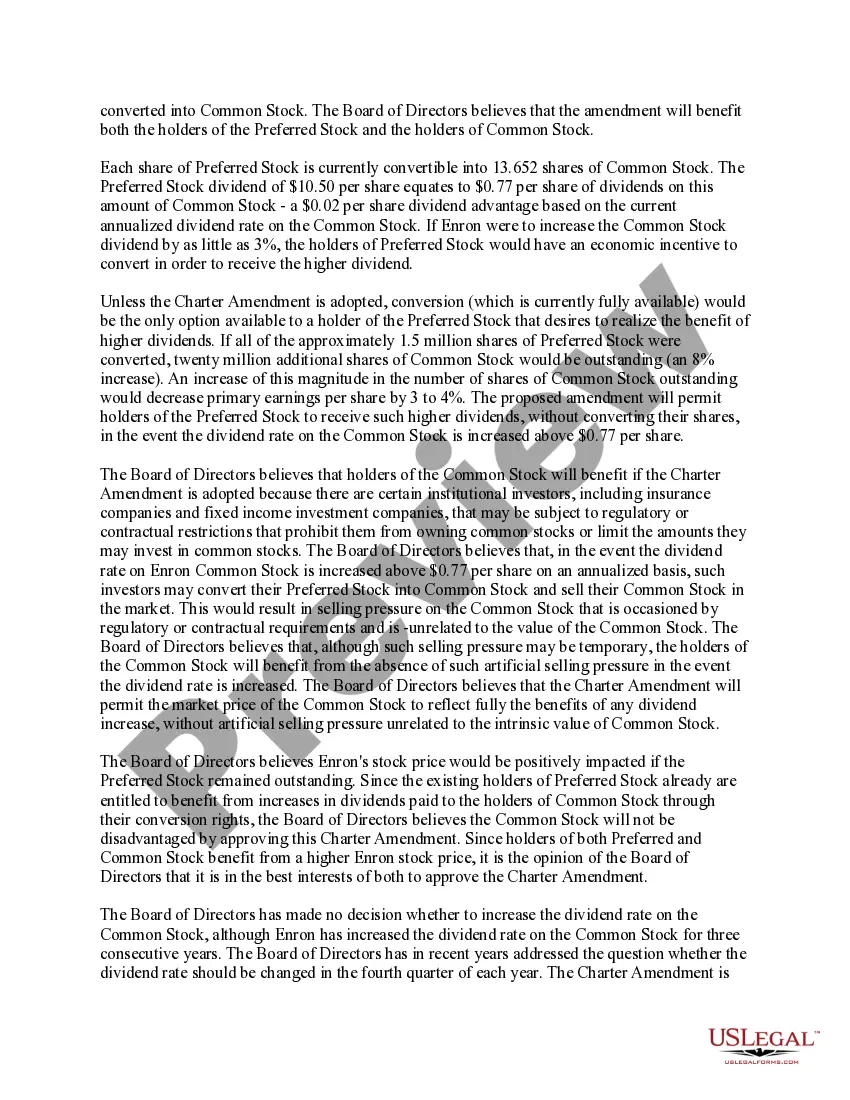

Pennsylvania Amendment of Restated Certificate of Incorporation to Change Dividend Rate on $10.50 Cumulative Second Preferred Convertible Stock The Pennsylvania Amendment of Restated Certificate of Incorporation is a legal document that allows a company incorporated in Pennsylvania to modify its existing corporate charter. One possible modification is to change the dividend rate on the $10.50 cumulative second preferred convertible stock. The $10.50 cumulative second preferred convertible stock is a type of security issued by a corporation, representing ownership in the company. It carries certain privileges and rights, including the payment of dividends. The existing dividend rate on this particular stock can be adjusted through the Pennsylvania Amendment of Restated Certificate of Incorporation. The amendment process involves making changes to the original charter of the company by filing the necessary documentation with the appropriate state authorities. The purpose of modifying the dividend rate on the $10.50 cumulative second preferred convertible stock could be to align it with current market conditions, financial performance, or shareholder expectations. By changing the dividend rate on the $10.50 cumulative second preferred convertible stock, the company may seek to attract more investors, enhance shareholder value, or align its payout policies with its financial capabilities. The specific rationale for amending the dividend rate can vary depending on the company's circumstances and goals. Different types of Pennsylvania Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock may include: 1. Increase in Dividend Rate: This amendment would entail raising the dividend rate on the $10.50 cumulative second preferred convertible stock. It could be driven by the desire to provide investors with higher returns or to stimulate demand for the stock. 2. Decrease in Dividend Rate: Conversely, this type of amendment would involve lowering the dividend rate on the $10.50 cumulative second preferred convertible stock. It may be done in response to changing economic conditions, the need to conserve capital, or to align with industry standards. 3. Adjusting Dividend Rate Formula: Instead of specifying a fixed rate, the amendment could introduce a formula or mechanism for determining the dividend rate on the $10.50 cumulative second preferred convertible stock. This approach allows for flexibility and can consider factors such as the company's profitability or market performance. 4. Elimination of Dividend: In some cases, a company may decide to eliminate dividends entirely on the $10.50 cumulative second preferred convertible stock. This decision could be driven by financial challenges or the need to prioritize other investment opportunities. Whatever the specific nature of the Pennsylvania Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock, it should comply with state law and be approved by the company's board of directors and shareholders. This process ensures transparency, fairness, and adherence to legal requirements.

Pennsylvania Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock

Description

How to fill out Pennsylvania Amendment Of Restated Certificate Of Incorporation To Change Dividend Rate On $10.50 Cumulative Second Preferred Convertible Stock?

Choosing the right legitimate papers web template can be quite a have difficulties. Of course, there are plenty of templates available on the net, but how can you find the legitimate type you require? Utilize the US Legal Forms site. The services delivers a large number of templates, like the Pennsylvania Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock, which can be used for enterprise and private needs. All of the varieties are inspected by pros and fulfill state and federal demands.

In case you are currently registered, log in to the account and click the Obtain switch to find the Pennsylvania Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock. Use your account to appear throughout the legitimate varieties you might have purchased earlier. Go to the My Forms tab of your respective account and obtain yet another copy of the papers you require.

In case you are a fresh consumer of US Legal Forms, listed here are straightforward instructions that you should stick to:

- Initially, ensure you have selected the appropriate type for your city/region. It is possible to examine the form making use of the Preview switch and browse the form description to guarantee this is basically the right one for you.

- In the event the type will not fulfill your requirements, make use of the Seach area to get the correct type.

- Once you are certain the form is proper, select the Buy now switch to find the type.

- Select the costs prepare you would like and enter the essential info. Design your account and pay for the transaction utilizing your PayPal account or credit card.

- Opt for the document structure and download the legitimate papers web template to the system.

- Comprehensive, change and print and indicator the received Pennsylvania Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock.

US Legal Forms will be the biggest catalogue of legitimate varieties where you can see numerous papers templates. Utilize the company to download expertly-produced papers that stick to status demands.