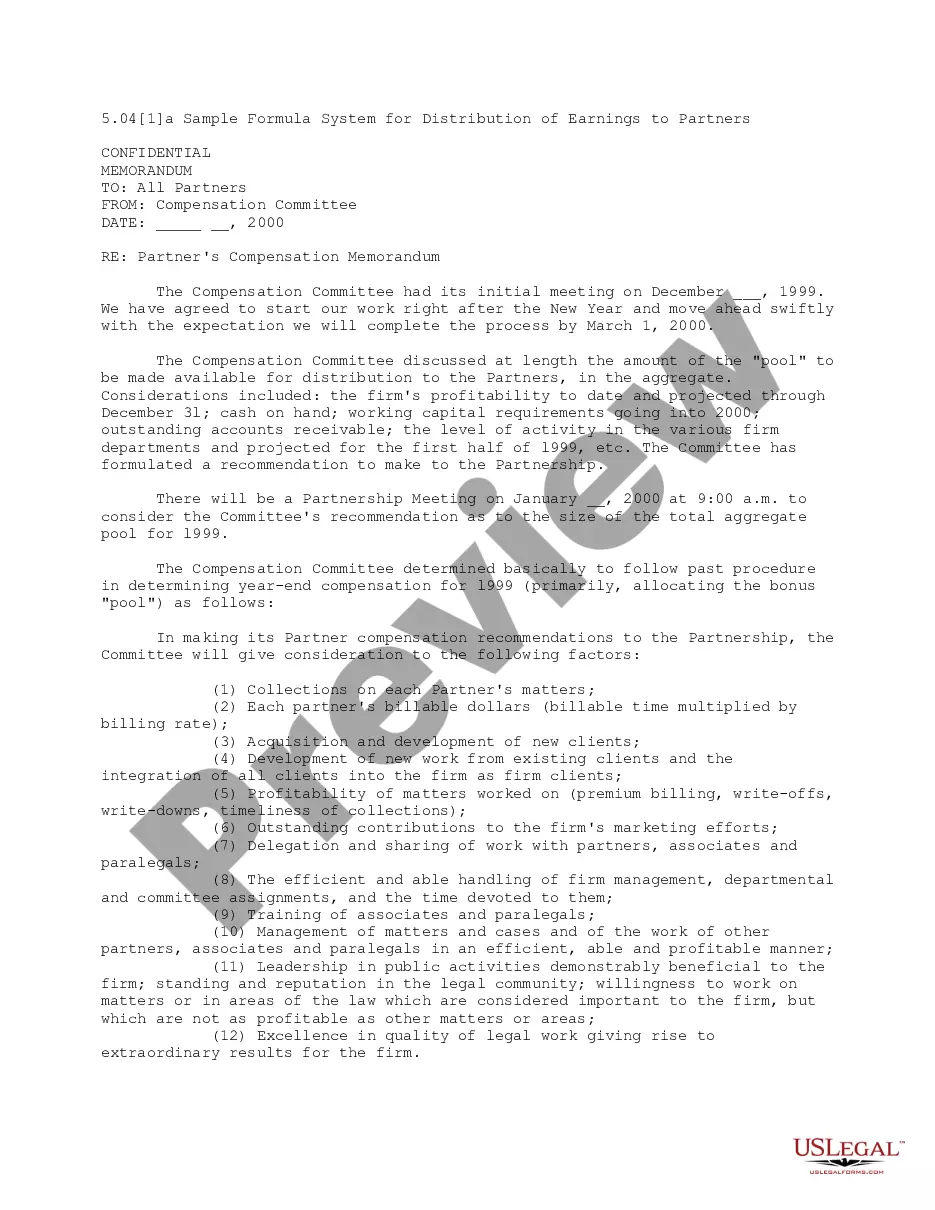

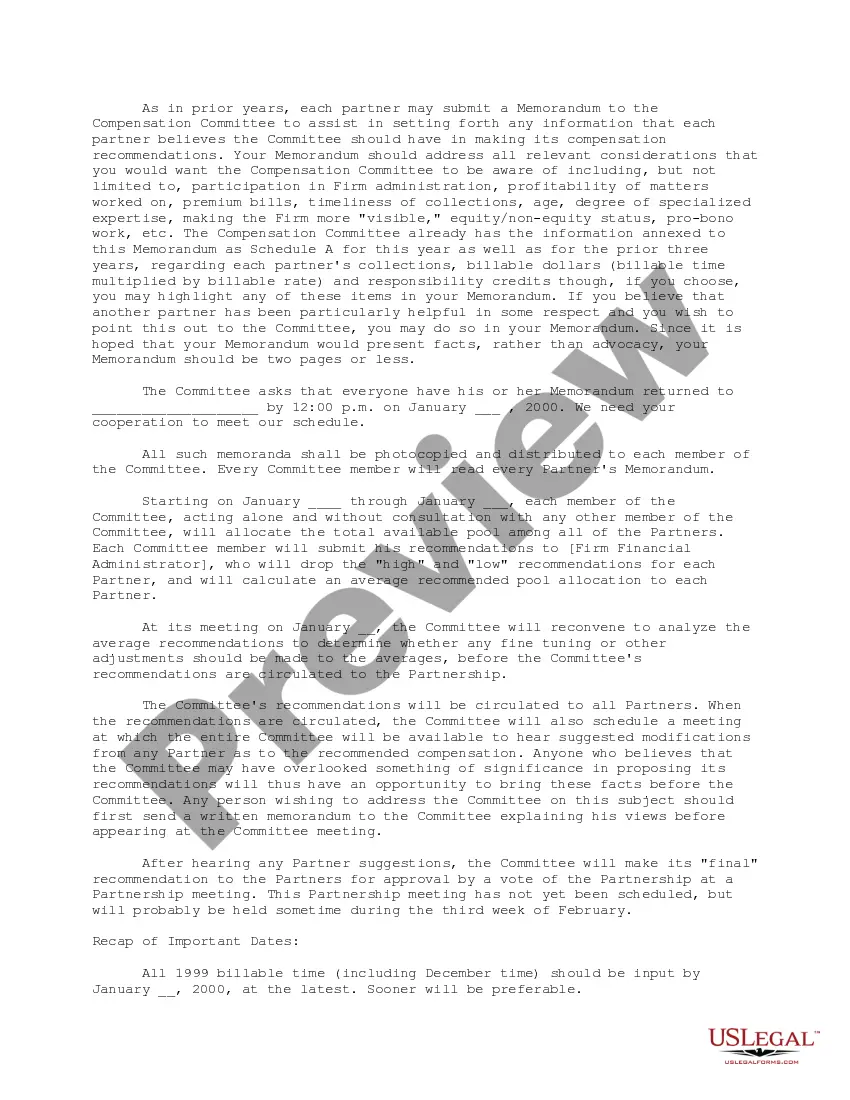

This Formula System for Distribution of Earnings to Partners provides a list of provisions to conside when making partner distribution recommendations. Some of the factors to consider are: Collections on each partner's matters, acquisition and development of new clients, profitablity of matters worked on, training of associates and paralegals, contributions to the firm's marketing practices, and others.

The Pennsylvania Formula System for Distribution of Earnings to Partners is a specific method utilized by partnerships in Pennsylvania to distribute profits among partners. This method takes into account various factors to ensure a fair and equitable distribution. The Pennsylvania Formula System considers factors such as capital contributions, time and effort invested by each partner, and the terms agreed upon in the partnership agreement. This system is designed to prevent any undue advantages or disadvantages for partners based on their individual circumstances. There are different types of Pennsylvania Formula System for Distribution of Earnings to Partners, including: 1. Equal Share Method: In this method, partners receive an equal percentage of the profits, regardless of their capital contributions or efforts invested. Each partner receives an equal share of the overall earnings. 2. Proportional Capital Method: This method distributes profits to partners based on their capital contributions. Partners who have contributed more capital receive a higher percentage of the profits. 3. Effort-based Method: This method considers the time and effort invested by each partner in the partnership's operations. Partners who contribute more time and effort receive a larger portion of the earnings. 4. Hybrid Method: Some partnerships may utilize a combination of factors to determine the distribution of earnings. This hybrid method could consider factors such as capital contributions, time and effort invested, and a fixed percentage distribution. The Pennsylvania Formula System for Distribution of Earnings to Partners aims to create transparency and fairness in profit distribution. It ensures that partners are rewarded proportionately to their contributions and efforts, fostering a sense of equality within the partnership. By considering various factors, this system provides partners with a clear understanding of how profits are distributed, minimizing potential disputes and disagreements.

The Pennsylvania Formula System for Distribution of Earnings to Partners is a specific method utilized by partnerships in Pennsylvania to distribute profits among partners. This method takes into account various factors to ensure a fair and equitable distribution. The Pennsylvania Formula System considers factors such as capital contributions, time and effort invested by each partner, and the terms agreed upon in the partnership agreement. This system is designed to prevent any undue advantages or disadvantages for partners based on their individual circumstances. There are different types of Pennsylvania Formula System for Distribution of Earnings to Partners, including: 1. Equal Share Method: In this method, partners receive an equal percentage of the profits, regardless of their capital contributions or efforts invested. Each partner receives an equal share of the overall earnings. 2. Proportional Capital Method: This method distributes profits to partners based on their capital contributions. Partners who have contributed more capital receive a higher percentage of the profits. 3. Effort-based Method: This method considers the time and effort invested by each partner in the partnership's operations. Partners who contribute more time and effort receive a larger portion of the earnings. 4. Hybrid Method: Some partnerships may utilize a combination of factors to determine the distribution of earnings. This hybrid method could consider factors such as capital contributions, time and effort invested, and a fixed percentage distribution. The Pennsylvania Formula System for Distribution of Earnings to Partners aims to create transparency and fairness in profit distribution. It ensures that partners are rewarded proportionately to their contributions and efforts, fostering a sense of equality within the partnership. By considering various factors, this system provides partners with a clear understanding of how profits are distributed, minimizing potential disputes and disagreements.