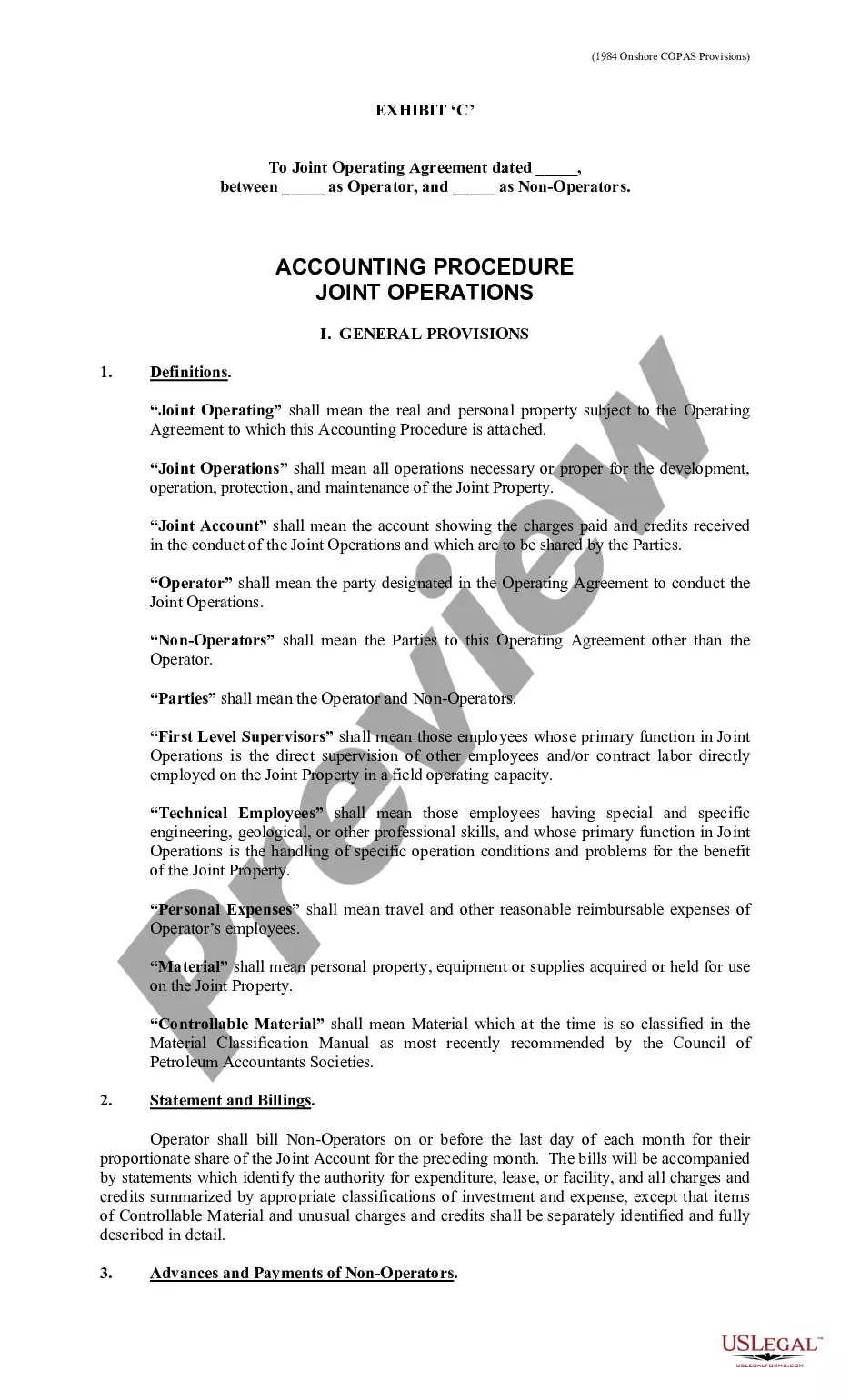

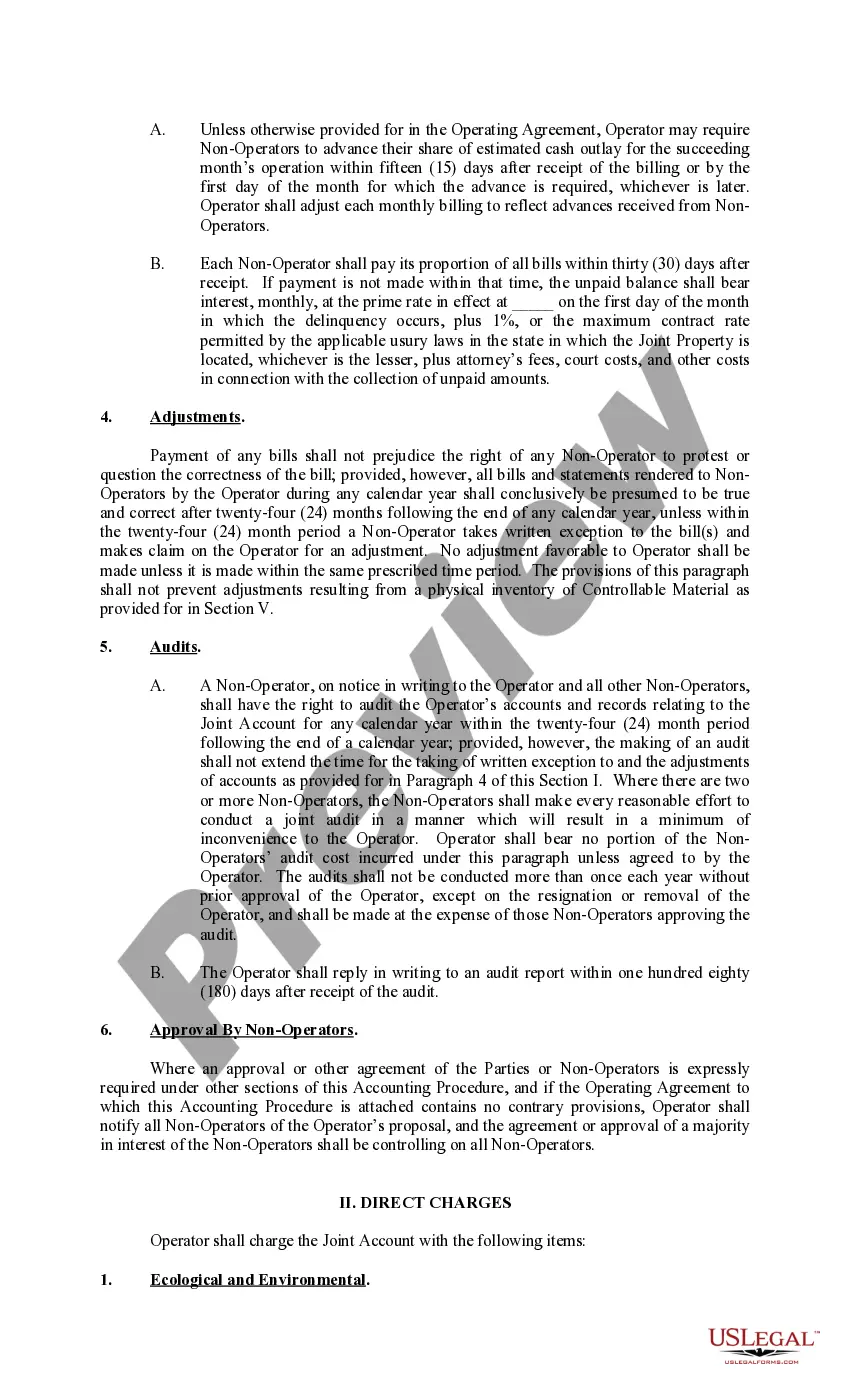

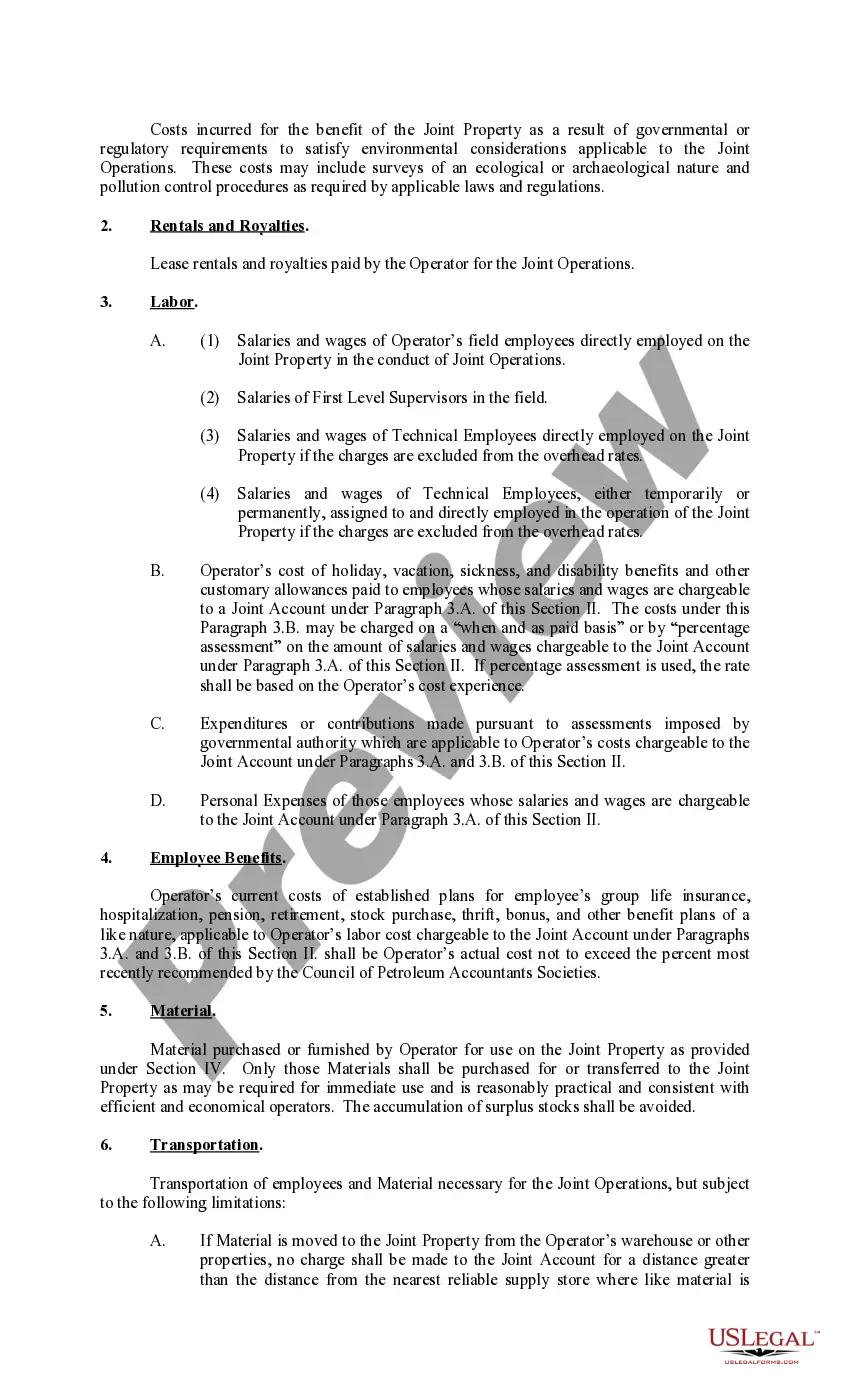

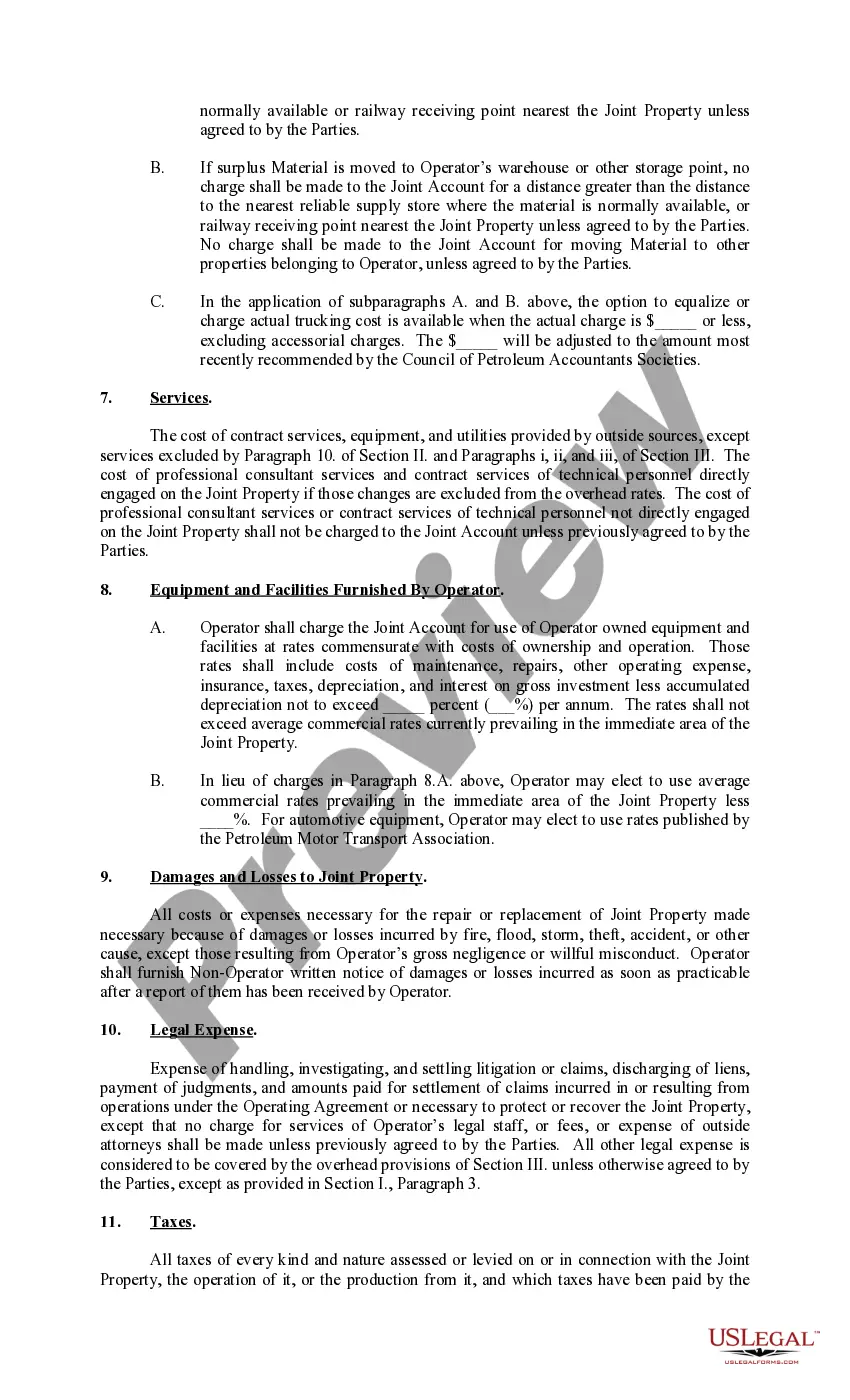

Pennsylvania Exhibit C Accounting Procedure Joint Operations is a specific accounting procedure that encompasses the financial management and reporting requirements for joint operations in the state of Pennsylvania. It outlines the guidelines and regulations necessary for tracking and documenting shared activities between two or more entities. Keywords: Pennsylvania, Exhibit C, accounting procedure, joint operations. This accounting procedure is vital for entities engaging in collaborative ventures such as partnerships, joint ventures, or any other form of joint operation. It provides a standardized framework for identifying, classifying, and recording transactions related to these operations, ensuring transparency, accuracy, and accountability. Different types of Pennsylvania Exhibit C Accounting Procedure Joint Operations include: 1. Partnership Joint Operations: This refers to joint activities involving two or more parties formed as a partnership, where the partners contribute resources, expertise, or capital towards a common goal. The accounting procedure governs the financial aspects of such partnerships, including revenue sharing, resource allocation, and expense distribution. 2. Joint Venture Operations: In this type of joint operation, two or more entities combine their resources, skills, and knowledge to undertake a specific project or business venture. The accounting procedure addresses the financial aspects of joint ventures, such as profit or loss sharing, investment tracking, and financial reporting requirements. 3. Cooperative Joint Operations: Cooperative joint operations involve entities pooling their resources and collaborating to achieve common objectives. This could include associations, cooperatives, or organizations aimed at mutual benefit. The accounting procedure outlines the cooperative accounting principles and guidelines to ensure accurate recording of financial transactions, shared expenses, and income distribution. The Pennsylvania Exhibit C Accounting Procedure Joint Operations offers detailed instructions for recording and classifying various financial activities concerning joint operations within the state. It covers aspects such as revenue recognition, expense allocation, profit or loss sharing, intercompany transactions, and reporting requirements. Furthermore, the accounting procedure may encompass guidelines on valuation of joint operation assets, treatment of liabilities, reserves, internal control measures, and the necessary disclosures needed for transparency and compliance with accounting standards. In conclusion, Pennsylvania Exhibit C Accounting Procedure Joint Operations is a comprehensive framework that aims to ensure accurate, transparent, and consistent accounting practices for joint operations taking place within the state. It caters to various types of joint operations, including partnerships, joint ventures, and cooperatives, providing guidelines for financial reporting, revenue, and expense recognition, and profit or loss sharing. This procedure serves as a valuable resource for entities engaging in collaborative ventures, facilitating efficient financial management and accountability.

Pennsylvania Exhibit C Accounting Procedure Joint Operations

Description

How to fill out Pennsylvania Exhibit C Accounting Procedure Joint Operations?

Are you presently in the place where you need to have papers for sometimes enterprise or individual reasons virtually every day time? There are a variety of lawful document templates available on the net, but finding kinds you can depend on isn`t simple. US Legal Forms delivers 1000s of kind templates, such as the Pennsylvania Exhibit C Accounting Procedure Joint Operations, which are created to satisfy state and federal needs.

When you are currently familiar with US Legal Forms internet site and also have a merchant account, just log in. After that, you may download the Pennsylvania Exhibit C Accounting Procedure Joint Operations design.

Unless you offer an accounts and want to begin using US Legal Forms, abide by these steps:

- Discover the kind you will need and make sure it is for your proper town/county.

- Make use of the Review key to review the form.

- Look at the outline to ensure that you have chosen the appropriate kind.

- In case the kind isn`t what you`re trying to find, make use of the Lookup industry to obtain the kind that meets your needs and needs.

- When you obtain the proper kind, click Buy now.

- Select the costs program you desire, fill out the desired details to create your money, and pay for the transaction with your PayPal or bank card.

- Select a hassle-free file format and download your version.

Find every one of the document templates you possess purchased in the My Forms menus. You may get a further version of Pennsylvania Exhibit C Accounting Procedure Joint Operations whenever, if possible. Just click the required kind to download or print out the document design.

Use US Legal Forms, probably the most substantial variety of lawful kinds, to save time and steer clear of faults. The service delivers professionally made lawful document templates which can be used for a selection of reasons. Generate a merchant account on US Legal Forms and start producing your life a little easier.