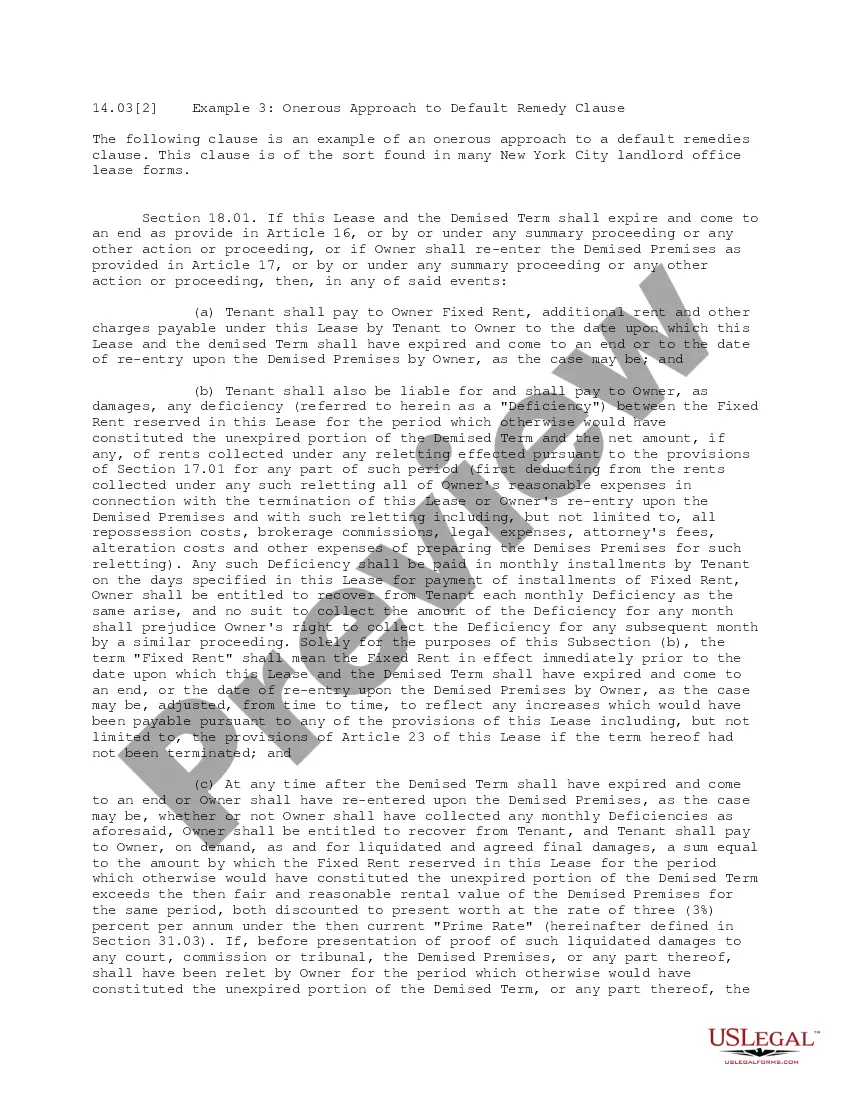

This office lease form is a standard default remedy clause, providing for the collection of the difference between the rent due and owing under the lease and the rents collected in the event of mitigation.

Pennsylvania Default Remedy Clause

Category:

State:

Multi-State

Control #:

US-OL14031

Format:

Word;

PDF

Instant download

Description

How to fill out Default Remedy Clause?

You may spend hours on-line looking for the lawful record template that fits the federal and state specifications you require. US Legal Forms offers a large number of lawful kinds that are analyzed by experts. You can easily down load or printing the Pennsylvania Default Remedy Clause from our services.

If you already have a US Legal Forms bank account, you are able to log in and click the Down load key. After that, you are able to full, change, printing, or signal the Pennsylvania Default Remedy Clause. Each and every lawful record template you purchase is the one you have for a long time. To have another version of any acquired type, proceed to the My Forms tab and click the related key.

If you are using the US Legal Forms web site initially, follow the easy guidelines under:

- Initial, be sure that you have chosen the proper record template for your area/city that you pick. See the type information to ensure you have chosen the appropriate type. If readily available, make use of the Preview key to search through the record template as well.

- If you would like discover another version of your type, make use of the Look for discipline to get the template that meets your needs and specifications.

- After you have located the template you would like, just click Acquire now to continue.

- Pick the prices strategy you would like, type your accreditations, and register for a merchant account on US Legal Forms.

- Comprehensive the purchase. You may use your bank card or PayPal bank account to purchase the lawful type.

- Pick the formatting of your record and down load it for your system.

- Make alterations for your record if necessary. You may full, change and signal and printing Pennsylvania Default Remedy Clause.

Down load and printing a large number of record layouts using the US Legal Forms Internet site, which offers the greatest variety of lawful kinds. Use specialist and state-particular layouts to handle your company or personal requires.

Form popularity

FAQ

No. Many Pennsylvania courts have said your landlord cannot evict you by self-help, meaning such things as padlocking your door, shutting off your utilities, using force to evict you, or using any eviction method other than going to court.

Pennsylvania law does not provide a set period for backing out of a signed lease. It's crucial to discuss your situation with the landlord promptly and attempt to reach an agreement regarding early termination. Be prepared for potential penalties based on the conditions stated within your lease.

Grace Period: There is no required grace period in Pennsylvania. NSF/Bounced Check Fee Maximum: If the tenant's rent check bounces, the landlord may charge a returned check fee of $50 unless they are charged more by their financial institution, in which case the landlord may charge that amount (18 PS § 4105e).

For example, if the rental property is in need of a critical repair, such as fixing the heat, a landlord must fix it within 24 hours. When it comes to non-critical emergencies, a landlord has 14 days to make the repair.

Under the right to a safe and habitable home, a landlord cannot force a tenant to move into a home or unit ?as-is? and cannot demand that the tenant be responsible for repairs. To be safe, and habitable, a unit or home should have: Working smoke alarms. Working hot water.

Early termination contract refers to the dissolution of a contract before the term of that contract has concluded. This will usually occur due to breach of contract, which involves a party failing to uphold the terms of the contract they signed.

Provide your landlord as much notice as possible and write a sincere letter explaining why you need to leave early. Ideally, you can offer your landlord a qualified replacement tenant with good credit and references, to sign a new lease.