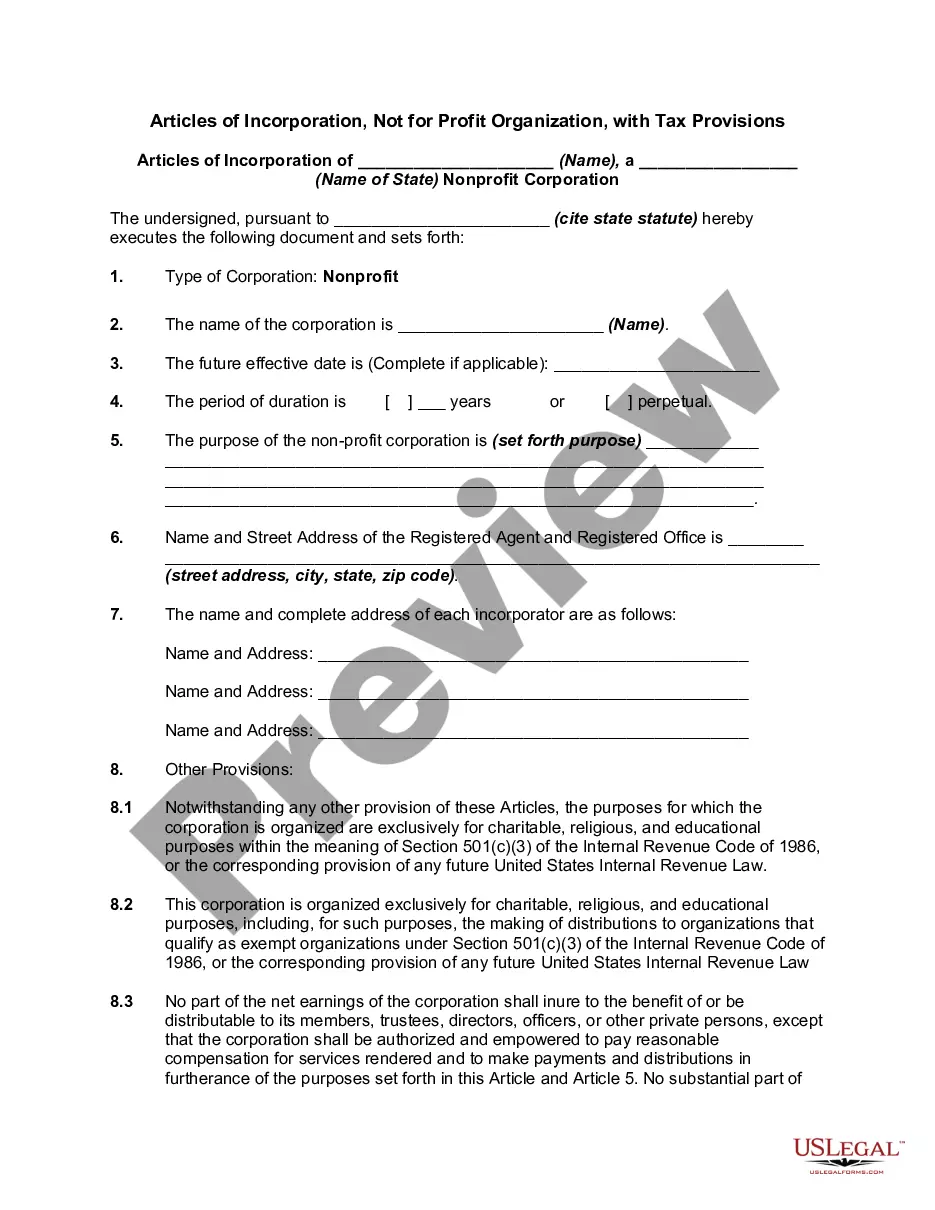

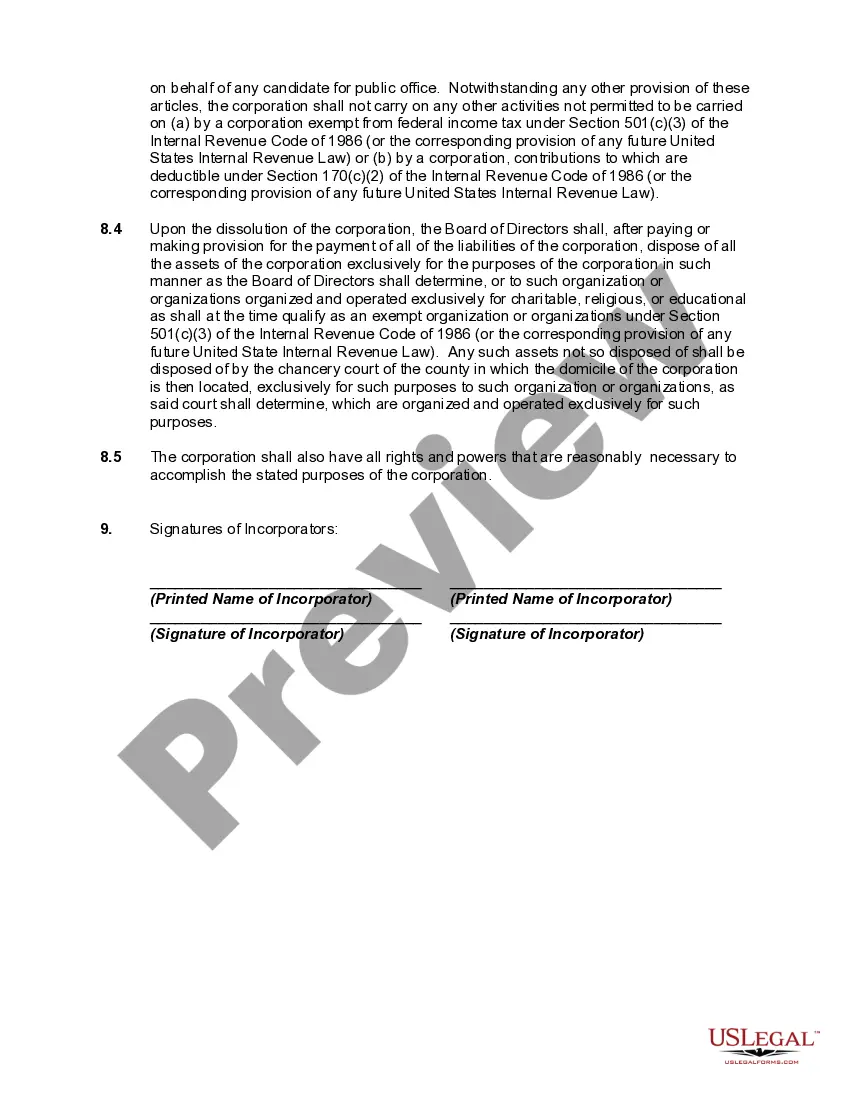

Puerto Rico Articles of Incorporation, Not for Profit Organization, with Tax Provisions When establishing a not-for-profit organization in Puerto Rico, it is vital to understand the process of filing the Articles of Incorporation and the tax provisions associated with such entities. This comprehensive guide will provide an in-depth description of what Puerto Rico Articles of Incorporation for Not-for-Profit Organizations entail, along with relevant keywords and different types of Articles of Incorporation available. 1. Puerto Rico Articles of Incorporation Overview: The Articles of Incorporation serves as a legal document through which a not-for-profit organization is officially formed and recognized in Puerto Rico. It must be filed with the Puerto Rico Department of State, which is responsible for overseeing corporate registrations on the island. 2. Key Elements of Puerto Rico Articles of Incorporation: a. Name of the Organization: Select a unique name for your not-for-profit organization, which complies with Puerto Rico's naming restrictions. b. Purpose and Mission: Clearly define the objectives and mission of your organization. This section should clearly state that the organization is not-for-profit. c. Registered Agent: Appoint a registered agent who will be the point of contact between the organization and the government. d. Membership: Determine whether your organization will have members or whether it will operate as a non-membership organization. e. Duration: Specify whether the organization will exist indefinitely or if it has a specific duration. f. Directors: List the initial directors or the board of directors responsible for managing the organization's affairs. g. Dissolution Clause: Include a dissolution clause that outlines the process and distribution of assets in the event of dissolution. 3. Tax Provisions for Not-for-Profit Organizations: Not-for-profit organizations in Puerto Rico can apply for exemption from certain taxes by obtaining a Determination Letter from the Puerto Rico Treasury Department. The tax provisions include: a. Tax-Exempt Status: Once granted, the organization will be exempt from paying Puerto Rico income tax and municipal license taxes on its activities. b. Donor Deductions: Donations made to tax-exempt organizations are usually tax-deductible for donors, encouraging philanthropic contributions. c. Annual Reports: Not-for-profit organizations are required to submit yearly reports to maintain their tax-exempt status, disclosing financial information and activities. 4. Different Types of Puerto Rico Articles of Incorporation for Not-for-Profit Organizations: a. Public Benefit Corporations: Focus primarily on public or community welfare, with a clear mission of benefiting the public. b. Religious Corporations: Specific to religious or faith-based organizations that fulfill social, educational, or philanthropic purposes. c. Professional Associations: These organizations are formed to represent the interests of professionals in a particular field. d. Social Advocacy Organizations: Address specific concerns or advocate for particular causes within society. e. Charitable Organizations: Primarily operate to provide charitable services, such as supporting the needy, funding education, or aiding disaster relief efforts. Understanding the process and requirements related to Puerto Rico Articles of Incorporation for Not-for-Profit Organizations, along with the tax provisions available, is crucial for establishing and maintaining a successful not-for-profit entity on the island. Ensure compliance with local laws and seek professional advice when necessary to navigate these intricacies effectively.

Puerto Rico Articles of Incorporation, Not for Profit Organization, with Tax Provisions

Description

How to fill out Puerto Rico Articles Of Incorporation, Not For Profit Organization, With Tax Provisions?

Are you within a place the place you require papers for possibly enterprise or specific functions nearly every day? There are a variety of legal papers themes accessible on the Internet, but finding types you can trust is not effortless. US Legal Forms provides thousands of form themes, like the Puerto Rico Articles of Incorporation, Not for Profit Organization, with Tax Provisions, which can be published to meet federal and state needs.

When you are already informed about US Legal Forms site and also have your account, just log in. Following that, you can download the Puerto Rico Articles of Incorporation, Not for Profit Organization, with Tax Provisions template.

Should you not come with an profile and would like to start using US Legal Forms, adopt these measures:

- Find the form you will need and ensure it is to the correct area/state.

- Take advantage of the Preview option to check the shape.

- See the information to ensure that you have chosen the right form.

- When the form is not what you are looking for, utilize the Look for area to discover the form that fits your needs and needs.

- Once you find the correct form, click on Acquire now.

- Select the costs program you desire, fill in the specified information to produce your money, and purchase the transaction with your PayPal or Visa or Mastercard.

- Choose a handy file structure and download your version.

Locate all the papers themes you might have bought in the My Forms menu. You can aquire a more version of Puerto Rico Articles of Incorporation, Not for Profit Organization, with Tax Provisions whenever, if possible. Just go through the needed form to download or printing the papers template.

Use US Legal Forms, the most extensive assortment of legal forms, in order to save efforts and prevent faults. The services provides professionally manufactured legal papers themes which can be used for a range of functions. Produce your account on US Legal Forms and initiate creating your life a little easier.