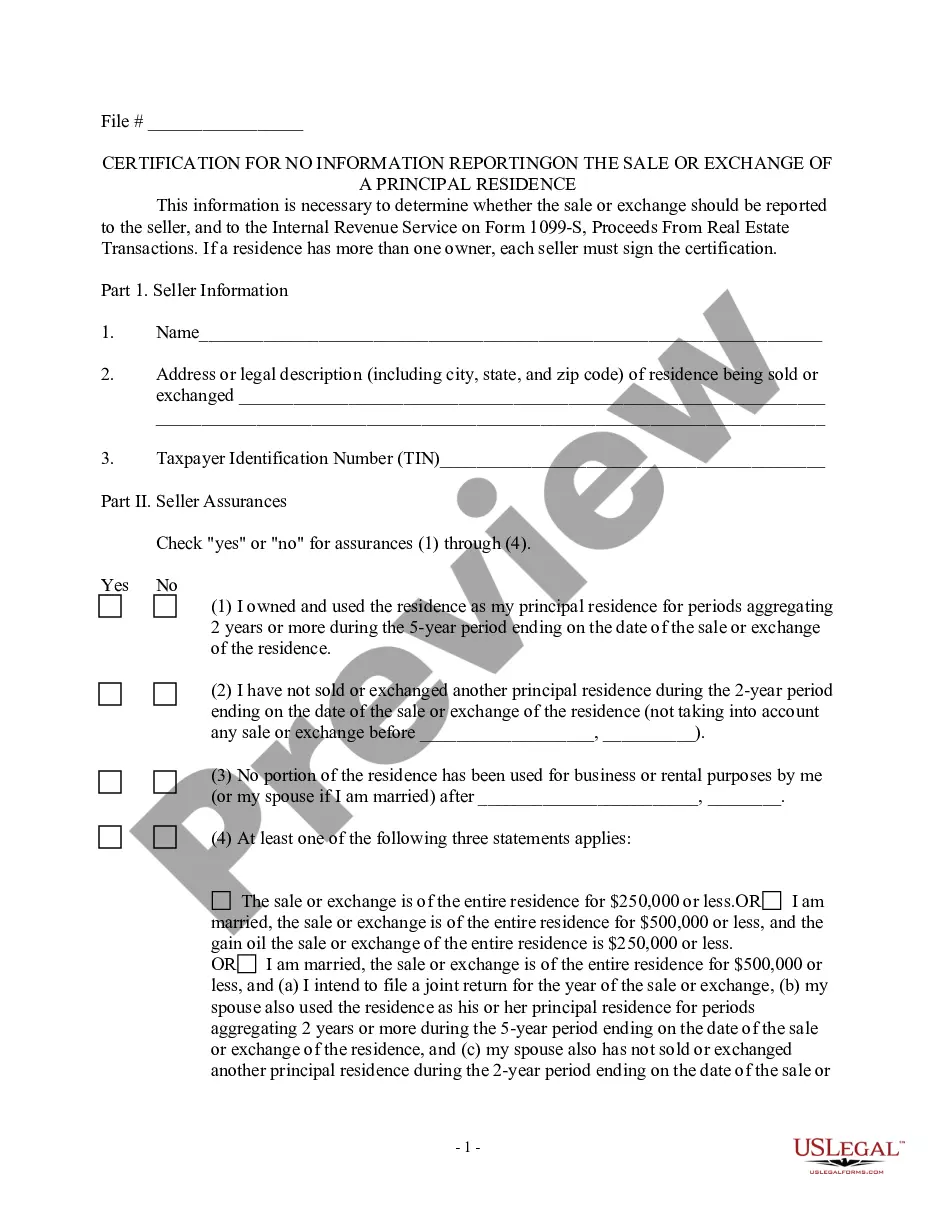

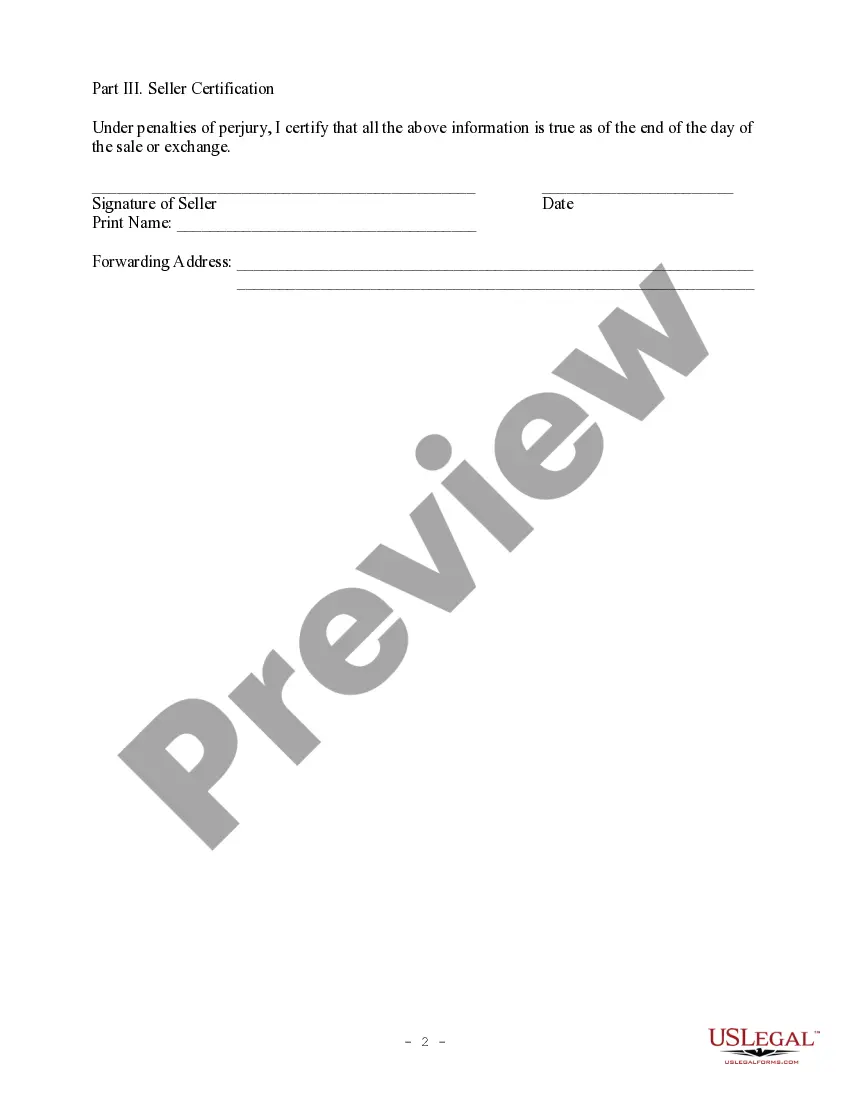

The Puerto Rico Certification of No Information Reporting on Sale or Exchange of Principal Residence — Tax Exemption is a documentation issued by the Puerto Rico Department of Treasury to certify that a taxpayer is eligible for a tax exemption on the sale or exchange of their principal residence. This detailed description will provide an overview of the certification process, its purpose, and any variations of the certification that may exist. The primary purpose of the Puerto Rico Certification of No Information Reporting on Sale or Exchange of Principal Residence — Tax Exemption is to establish eligibility for tax exemption on the sale or exchange of a taxpayer's principal residence in Puerto Rico. This certification proves that the taxpayer has met the necessary requirements set by the tax authorities, allowing them to avoid reporting the transaction and potentially being subject to a tax liability. To obtain this certification, the taxpayer must fulfill specific criteria as determined by the Puerto Rico tax laws. These criteria often include owning and residing in the property for a specified period, such as two years or more, as their principal residence. Additionally, the taxpayer must not have previously claimed this tax exemption within a certain timeframe, typically five years. The documentation required to support the certification may include proof of ownership, residence, and details of the sale or exchange transaction. Different types of Puerto Rico Certification of No Information Reporting on Sale or Exchange of Principal Residence — Tax Exemption may exist depending on the taxpayer's circumstances. These variations may include: 1. Standard Certification: This certification applies to taxpayers who meet all the necessary criteria for the tax exemption on the sale or exchange of their principal residence. 2. Multiple Residence Certification: Some taxpayers may own and reside in multiple properties within Puerto Rico. In such cases, a separate certification for each residence may be required to claim the tax exemption on the sale or exchange of each of these properties. 3. Time-Adjusted Certification: If a taxpayer has not met the minimum ownership and residency requirements due to specific circumstances, such as a job transfer or medical reasons, they may still be eligible for a prorated tax exemption. This variation of the certification takes into account the time spent as the principal residence and adjusts the tax exemption accordingly. 4. Retroactive Certification: In certain situations where a taxpayer fails to obtain the certification before the sale or exchange of their principal residence, they may be required to obtain a retroactive certification. This type of certification allows them to claim the tax exemption retrospectively after meeting the necessary requirements. It is important for taxpayers to ensure they fulfill all the eligibility criteria and provide accurate documentation when applying for the Puerto Rico Certification of No Information Reporting on Sale or Exchange of Principal Residence — Tax Exemption. Failure to comply with the requirements may result in the denial of the tax exemption or potential penalties from the Puerto Rico tax authorities.

Puerto Rico Certification of No Information Reporting on Sale or Exchange of Principal Residence - Tax Exemption

Description

How to fill out Puerto Rico Certification Of No Information Reporting On Sale Or Exchange Of Principal Residence - Tax Exemption?

Finding the right legal record format could be a battle. Of course, there are a variety of layouts available on the Internet, but how do you discover the legal type you will need? Utilize the US Legal Forms site. The service provides a large number of layouts, such as the Puerto Rico Certification of No Information Reporting on Sale or Exchange of Principal Residence - Tax Exemption, which can be used for organization and private demands. Each of the kinds are checked by experts and meet up with federal and state specifications.

Should you be currently authorized, log in to your account and then click the Obtain option to have the Puerto Rico Certification of No Information Reporting on Sale or Exchange of Principal Residence - Tax Exemption. Make use of your account to check with the legal kinds you have acquired formerly. Proceed to the My Forms tab of your own account and obtain an additional copy of the record you will need.

Should you be a brand new end user of US Legal Forms, listed here are easy guidelines so that you can comply with:

- Very first, make sure you have selected the right type for your city/area. It is possible to check out the form making use of the Review option and browse the form description to ensure this is the right one for you.

- If the type will not meet up with your requirements, use the Seach industry to discover the right type.

- Once you are sure that the form is acceptable, click the Purchase now option to have the type.

- Pick the costs program you want and type in the necessary details. Make your account and pay for an order with your PayPal account or credit card.

- Pick the submit formatting and obtain the legal record format to your product.

- Total, change and print out and sign the received Puerto Rico Certification of No Information Reporting on Sale or Exchange of Principal Residence - Tax Exemption.

US Legal Forms is the most significant library of legal kinds for which you will find a variety of record layouts. Utilize the company to obtain expertly-produced papers that comply with status specifications.