Puerto Rico Jury Instruction - 10.10.6 Section 6672 Penalty

Description

How to fill out Jury Instruction - 10.10.6 Section 6672 Penalty?

If you wish to total, down load, or printing legitimate document templates, use US Legal Forms, the largest collection of legitimate varieties, which can be found on-line. Use the site`s easy and handy search to discover the files you require. Different templates for company and individual uses are sorted by types and claims, or keywords and phrases. Use US Legal Forms to discover the Puerto Rico Jury Instruction - 10.10.6 Section 6672 Penalty with a handful of click throughs.

Should you be presently a US Legal Forms customer, log in in your profile and then click the Obtain switch to get the Puerto Rico Jury Instruction - 10.10.6 Section 6672 Penalty. You can also accessibility varieties you formerly delivered electronically from the My Forms tab of the profile.

If you are using US Legal Forms initially, follow the instructions under:

- Step 1. Make sure you have selected the form for your right town/land.

- Step 2. Utilize the Preview choice to look over the form`s articles. Don`t forget about to read through the description.

- Step 3. Should you be unsatisfied with the develop, take advantage of the Search discipline towards the top of the monitor to discover other models of your legitimate develop format.

- Step 4. After you have found the form you require, go through the Get now switch. Pick the rates strategy you favor and include your references to sign up on an profile.

- Step 5. Process the purchase. You should use your charge card or PayPal profile to finish the purchase.

- Step 6. Find the formatting of your legitimate develop and down load it on your own gadget.

- Step 7. Comprehensive, change and printing or sign the Puerto Rico Jury Instruction - 10.10.6 Section 6672 Penalty.

Each and every legitimate document format you purchase is your own forever. You possess acces to each develop you delivered electronically with your acccount. Go through the My Forms section and choose a develop to printing or down load once more.

Contend and down load, and printing the Puerto Rico Jury Instruction - 10.10.6 Section 6672 Penalty with US Legal Forms. There are thousands of specialist and condition-particular varieties you can utilize for your personal company or individual demands.

Form popularity

FAQ

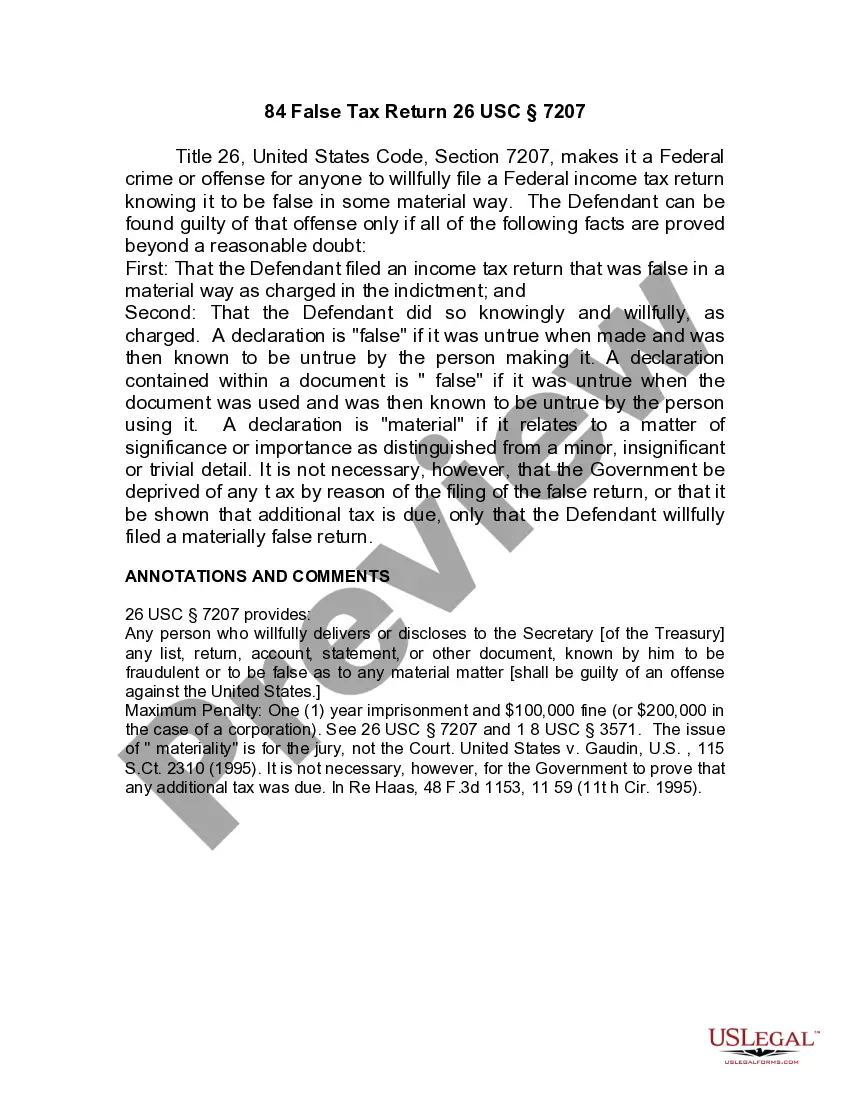

Any person required to collect, truthfully account for, and pay over any tax imposed by this title who willfully fails to collect such tax, or truthfully account for and pay over such tax, or willfully attempts in any manner to evade or defeat any such tax or the payment thereof, shall, in addition to other penalties ...

The IRS generally has 10 years ? from the date your tax was assessed ? to collect the tax and any associated penalties and interest from you. This time period is called the Collection Statute Expiration Date (CSED). Your account can include multiple tax assessments, each with their own CSED.

The amount of the penalty is equal to the unpaid balance of the trust fund tax. The penalty is computed based on: The unpaid income taxes withheld, plus. The employee's portion of the withheld FICA taxes.

A responsible person for this purpose can be an officer of a corporation, a partner, a sole proprietor, or an employee of any form of business. A trustee or agent with authority over the funds of the business can also be held responsible for the penalty.

§ 6672 ? Failure to Collect and Pay Over Tax, or Attempt to Evade or Defeat Tax. Also Referred to as Internal Revenue Code Section 6672; I.R.C. § 6672; Section 6672; Trust Fund Recovery PenaltyBackground.

A willful failure to collect and remit trust fund taxes is punishable by up to a $10,000 fine, five years in prison, or both. However, the IRS typically reserves criminal charges for the most extreme cases.

Any person required to collect, truthfully account for, and pay over any tax imposed by this title who willfully fails to collect such tax, or truthfully account for and pay over such tax, or willfully attempts in any manner to evade or defeat any such tax or the payment thereof, shall, in addition to other penalties ...

If a business has failed to collect or pay over income and employment taxes, or has failed to pay over collected excise taxes, the trust fund recovery penalty may be asserted against those determined to have been responsible and willful in failing to pay over the tax.

If the IRS assesses a penalty, it has up to 10 years to collect it. During that time, the IRS will take your assets if you are responsible. However, the IRS only has 3 years to assess the penalty. This clock starts ticking on April 15 after the year the trust fund taxes were due to be filed.