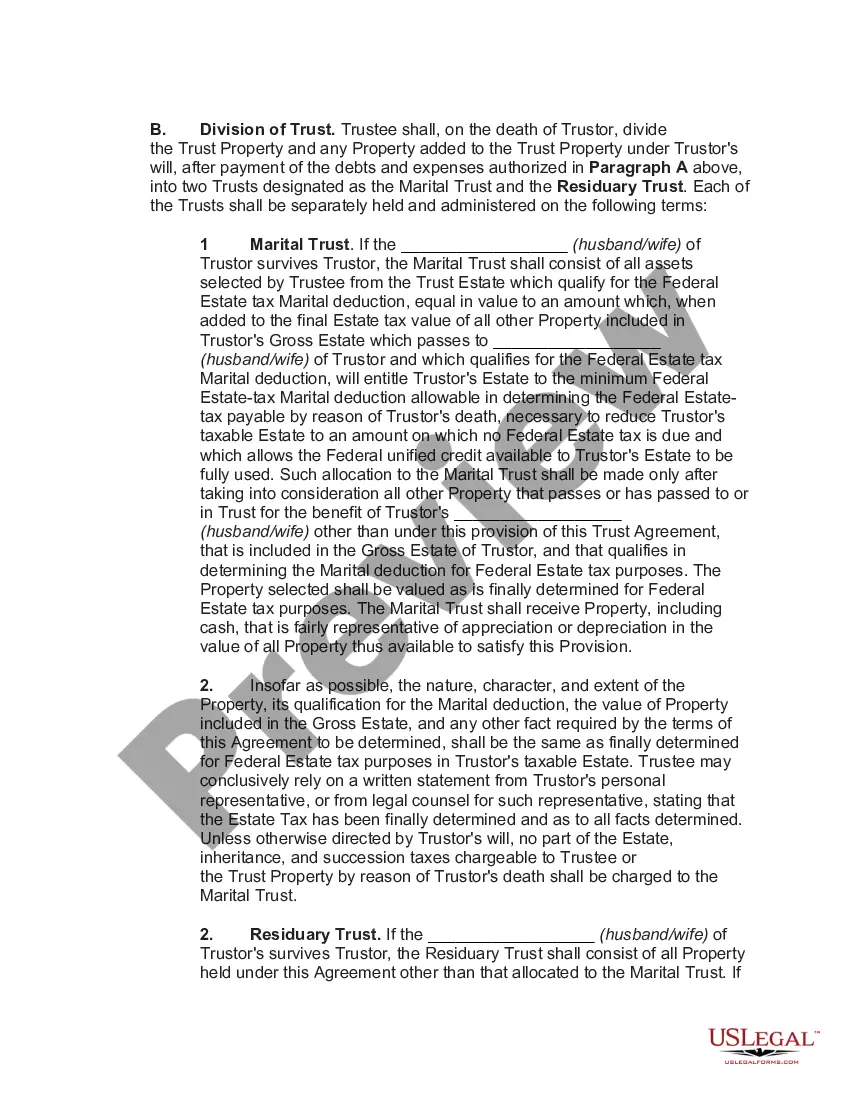

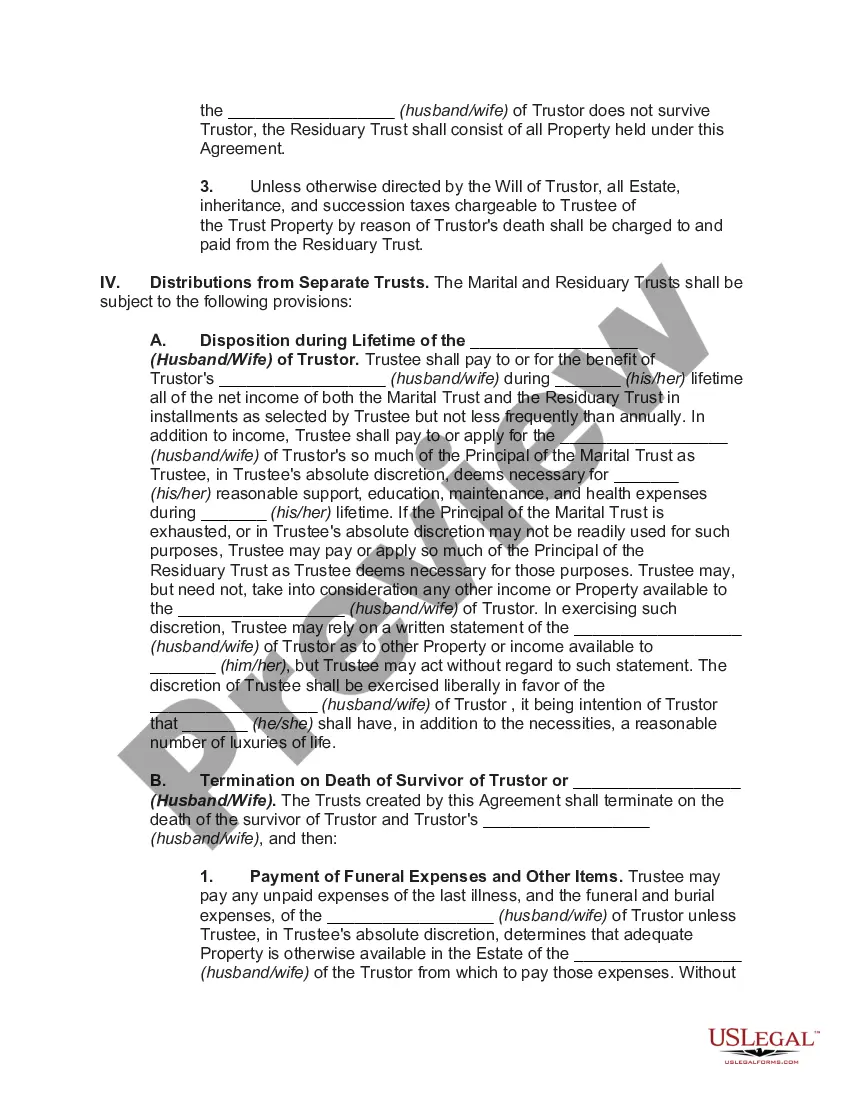

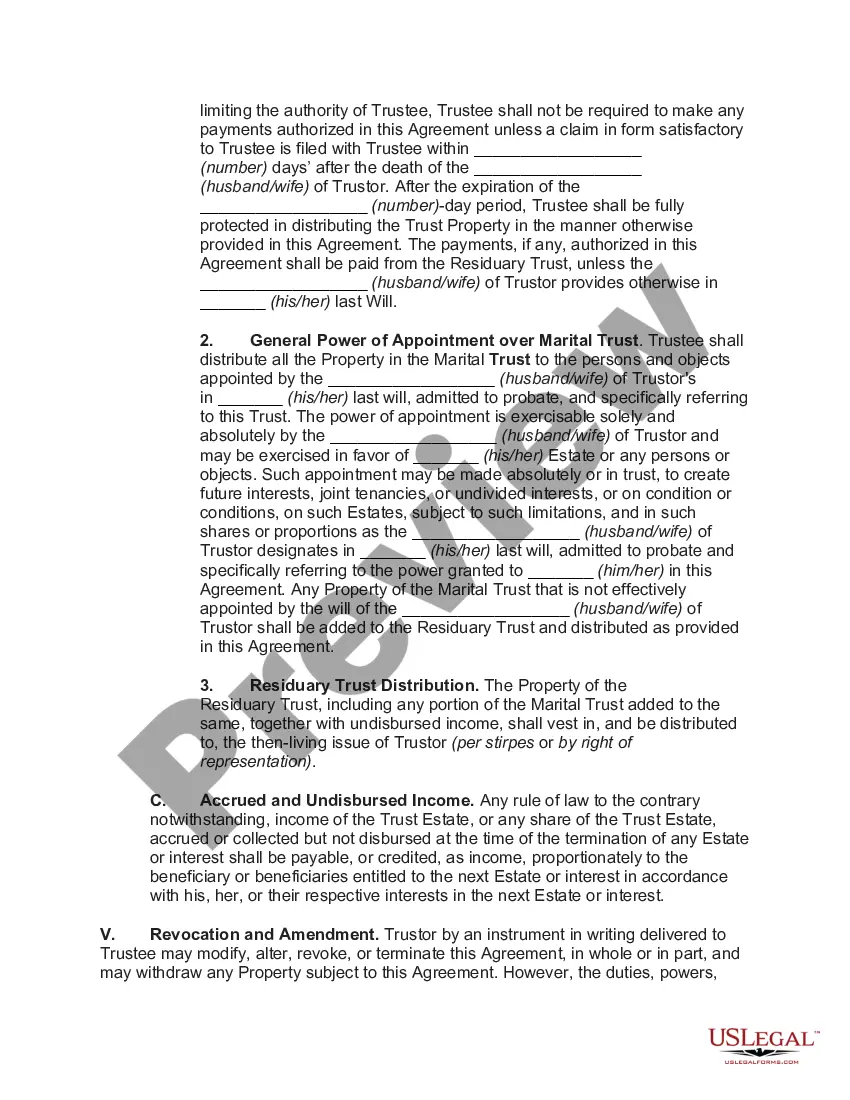

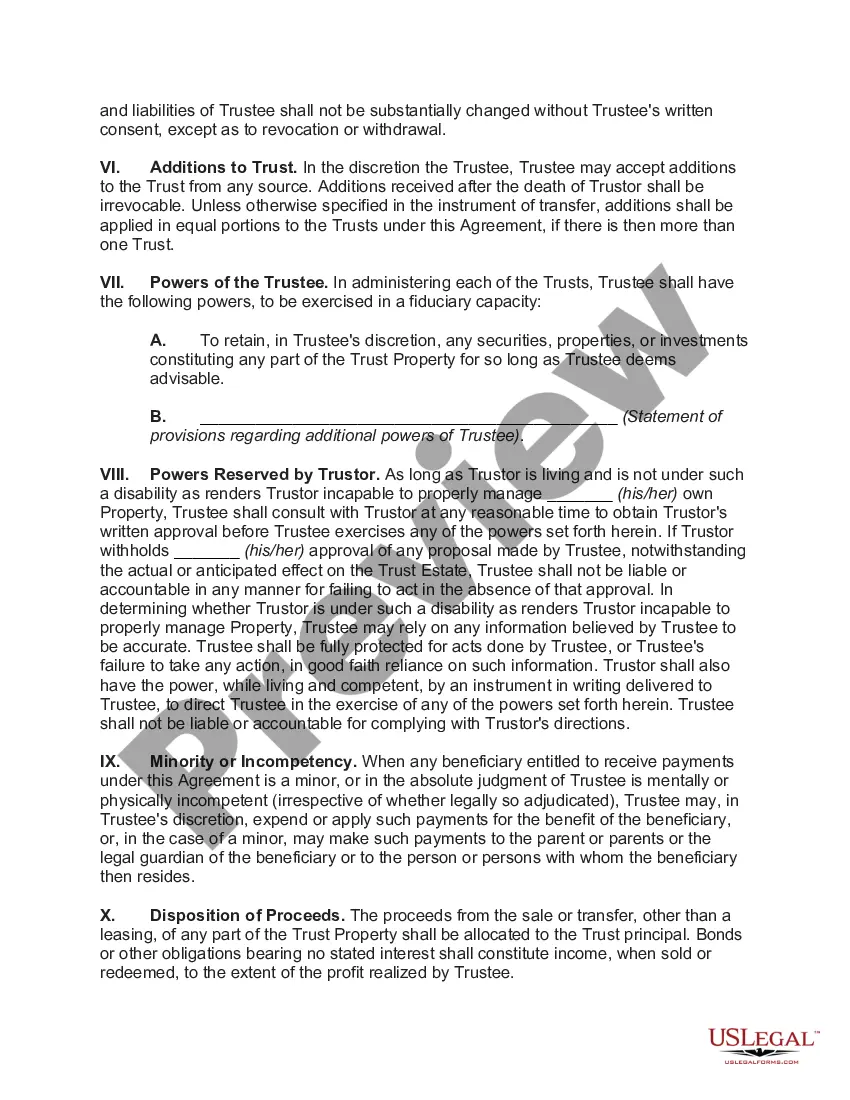

Puerto Rico Marital-deduction Residuary Trust with a Single Trust or and Lifetime Income and Power of Appointment in Beneficiary Spouse is a type of trust structure that is utilized in estate planning in Puerto Rico. This specific trust arrangement allows an individual, known as the trust or, to transfer their remaining assets to a trust, thereby ensuring the financial well-being of their spouse. In this trust, the trust or designates their spouse as the beneficiary, granting them the right to receive income generated by the trust assets throughout their lifetime. The trust or can allocate different types of assets, such as real estate, investments, or businesses, into the trust's residuary assets. These assets will be managed by a trustee appointed by the trust or. One critical feature of the Puerto Rico Marital-deduction Residuary Trust is the power of appointment given to the beneficiary spouse. This power allows the beneficiary spouse to designate who will inherit the trust's remaining assets upon their passing. This provision enables flexibility and control over the distribution of assets, ensuring that the trust's intentions align with the beneficiary spouse's wishes. Different variations of the Puerto Rico Marital-deduction Residuary Trust with a Single Trust or and Lifetime Income and Power of Appointment in Beneficiary Spouse may include: 1. Irrevocable Marital-deduction Residuary Trust: This trust structure is considered irrevocable, meaning any assets placed in the trust cannot be reclaimed or altered by the trust or once transferred. This provides added protection against potential disputes or changes in circumstances. 2. Testamentary Marital-deduction Residuary Trust: This type of trust is established through the trust or's last will and testament and only becomes effective upon the trust or's death. It allows the trust or to control the distribution of assets while providing the surviving spouse with lifetime income and the power of appointment. 3. Granter Retained Income Trust (GRIT): A GRIT is a variation of the Puerto Rico Marital-deduction Residuary Trust where the trust or retains the right to receive income from the trust for a specified period, with the remaining assets passing to the beneficiary spouse. It can be an effective estate planning tool for minimizing estate taxes. 4. Credit Shelter Trust (CST): Although not specifically mentioned in the query, it is worth noting that a CST is a common type of trust employed in conjunction with a Puerto Rico Marital-deduction Residuary Trust. A CST allows the trust or to maximize the use of their estate tax exemption, ensuring that the assets transferred to the trust are not subject to estate taxes upon their death. In conclusion, the Puerto Rico Marital-deduction Residuary Trust with a Single Trust or and Lifetime Income and Power of Appointment in Beneficiary Spouse provides a comprehensive estate planning solution. It safeguards the financial security of the surviving spouse while allowing for flexibility through the power of appointment. Different variations of this trust structure cater to specific individual needs and objectives, making it a valuable tool in Puerto Rico's estate planning arsenal.

Puerto Rico Marital-deduction Residuary Trust with a Single Trustor and Lifetime Income and Power of Appointment in Beneficiary Spouse

Description

How to fill out Puerto Rico Marital-deduction Residuary Trust With A Single Trustor And Lifetime Income And Power Of Appointment In Beneficiary Spouse?

Are you currently within a placement that you require files for possibly company or individual purposes just about every day time? There are tons of legitimate papers templates accessible on the Internet, but finding types you can rely isn`t straightforward. US Legal Forms offers 1000s of form templates, just like the Puerto Rico Marital-deduction Residuary Trust with a Single Trustor and Lifetime Income and Power of Appointment in Beneficiary Spouse, which are composed in order to meet state and federal requirements.

If you are presently knowledgeable about US Legal Forms site and get a merchant account, simply log in. Afterward, you may obtain the Puerto Rico Marital-deduction Residuary Trust with a Single Trustor and Lifetime Income and Power of Appointment in Beneficiary Spouse design.

If you do not provide an profile and wish to begin to use US Legal Forms, follow these steps:

- Get the form you need and make sure it is to the proper city/state.

- Use the Preview button to analyze the shape.

- Look at the information to ensure that you have selected the right form.

- In the event the form isn`t what you are searching for, make use of the Research field to obtain the form that fits your needs and requirements.

- When you find the proper form, simply click Purchase now.

- Choose the pricing program you need, complete the necessary details to create your account, and purchase the transaction making use of your PayPal or credit card.

- Pick a convenient paper format and obtain your duplicate.

Find all of the papers templates you might have purchased in the My Forms menu. You can aquire a additional duplicate of Puerto Rico Marital-deduction Residuary Trust with a Single Trustor and Lifetime Income and Power of Appointment in Beneficiary Spouse whenever, if needed. Just go through the necessary form to obtain or printing the papers design.

Use US Legal Forms, one of the most considerable selection of legitimate types, to conserve efforts and stay away from mistakes. The services offers expertly manufactured legitimate papers templates that can be used for a range of purposes. Generate a merchant account on US Legal Forms and commence creating your way of life a little easier.