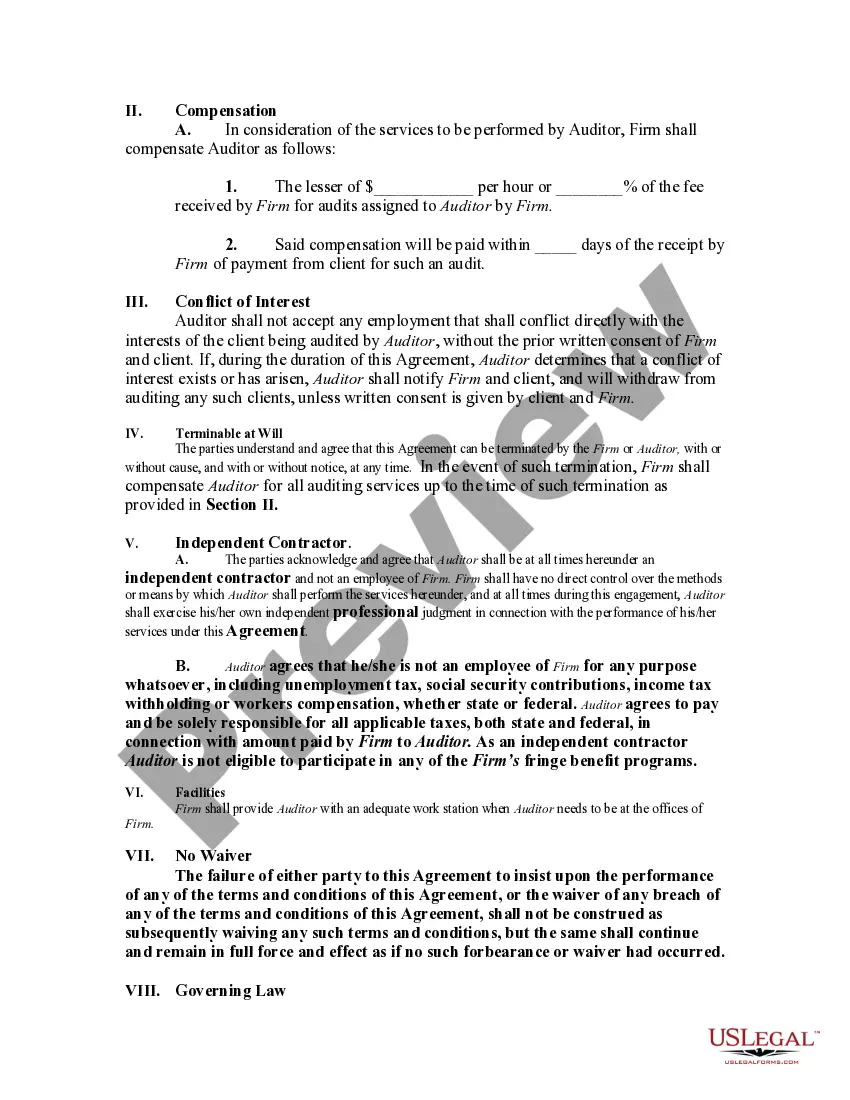

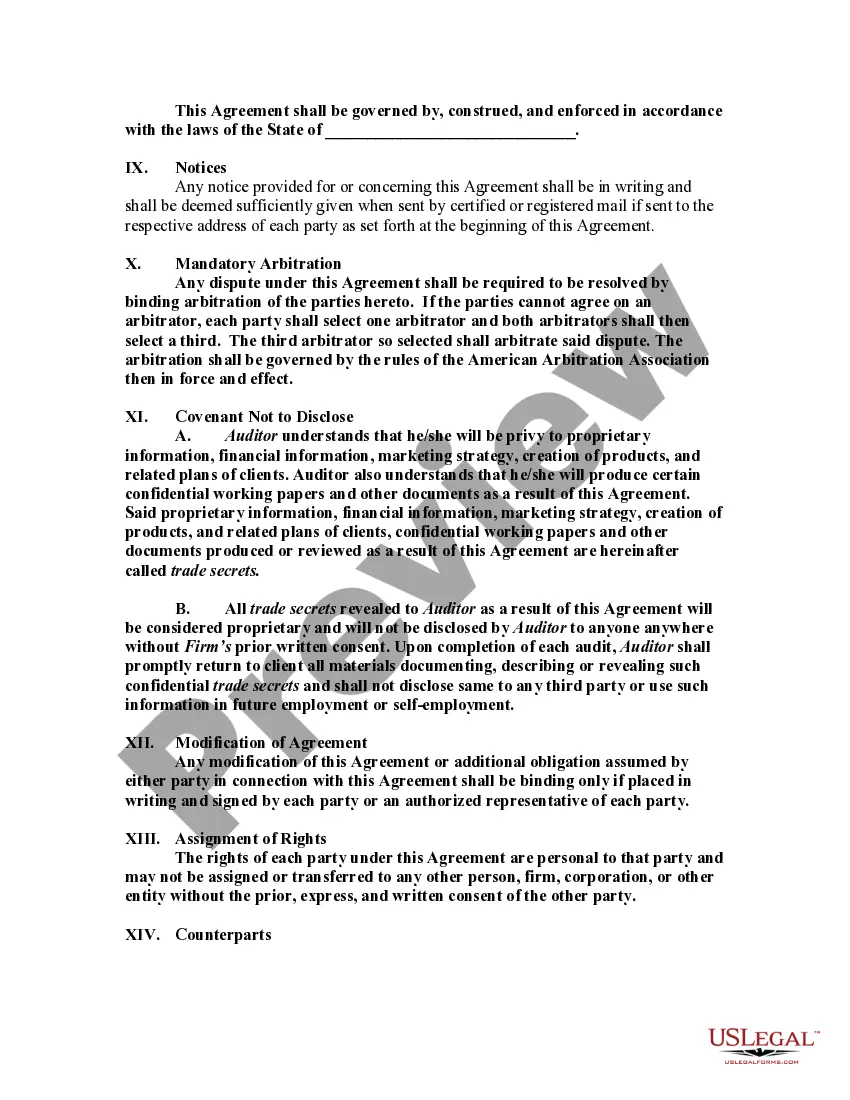

Although no definite rule exists for determining whether one is an independent contractor or an employee, certain indicia of the status of an independent contractor are recognized, and the insertion of provisions embodying these indicia in the contract will help to insure that the relationship reflects the intention of the parties. These indicia generally relate to the basic issue of control. The general test of what constitutes an independent contractor relationship involves which party has the right to direct what is to be done, and how and when. Another important test involves the method of payment of the contractor.

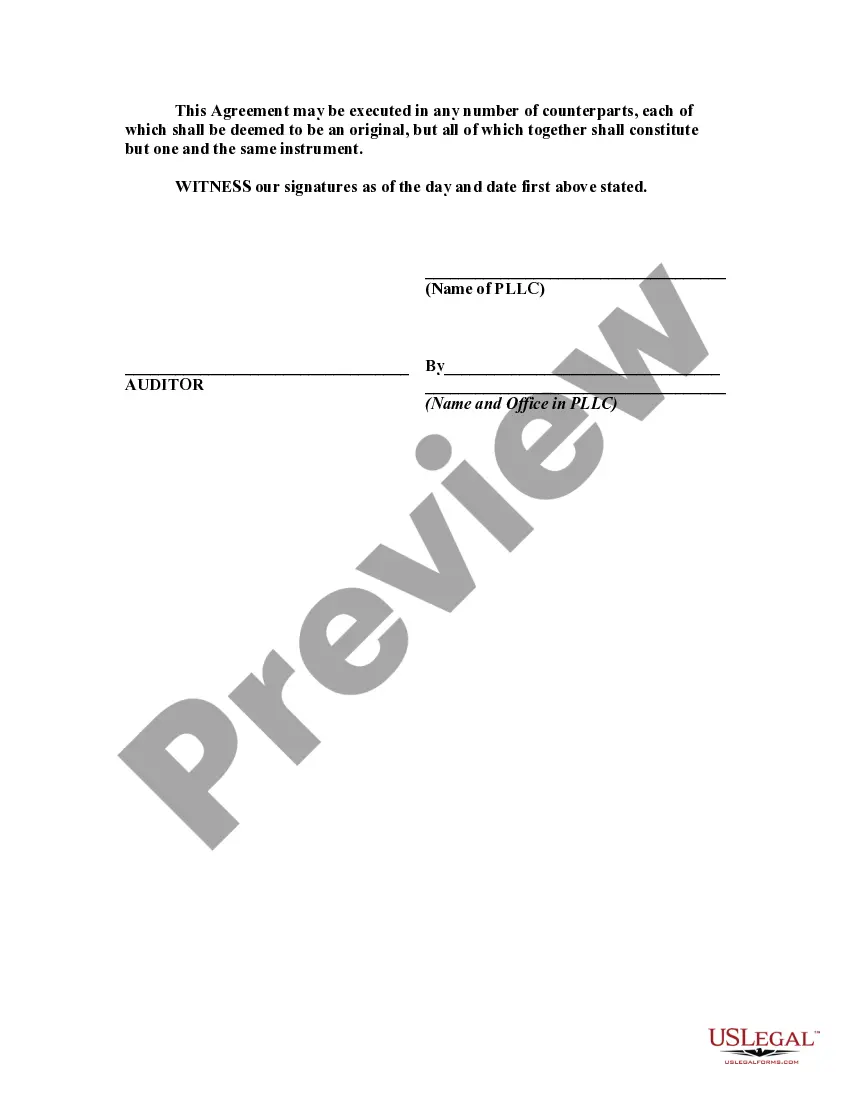

Rhode Island Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is a legal document that establishes a professional relationship between an accounting firm and an auditor, who will work as a self-employed independent contractor. This agreement outlines the specific terms and conditions under which the auditor will provide their services to the accounting firm. In Rhode Island, there are various types of agreements that accounting firms can use to employ auditors as self-employed independent contractors. Some common variations include: 1. Full-time Auditor Agreement: This type of agreement is used when an accounting firm hires an auditor on a full-time basis to work exclusively for their firm. It details the responsibilities, compensation, and work schedule of the auditor. 2. Part-time Auditor Agreement: When an accounting firm requires an auditor to work on a part-time basis, this type of agreement is utilized. It outlines the hours and days the auditor will work, along with their compensation and scope of responsibilities. 3. Project-Based Auditor Agreement: In situations where an accounting firm needs an auditor for a specific project or engagement, this agreement is employed. It specifies the scope of work, duration of the project, deliverables, and compensation structure. 4. Remote Auditor Agreement: Accounting firms might engage auditors who are not located within their office premises. This type of agreement covers the terms for auditors working remotely, including communication channels, reporting requirements, and compensation arrangements. Regardless of the specific type of agreement, certain key elements should be covered within the Rhode Island Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: 1. Identification of Parties: The agreement should clearly identify both the accounting firm and the auditor, including their legal names and addresses. 2. Services to be Provided: It is important to outline the specific services the auditor will be responsible for providing. This can include financial statement audits, internal control reviews, tax preparation, or any other accounting related tasks. 3. Payment Terms: The compensation structure, payment frequency, and any additional expenses to be reimbursed should be clearly defined in the agreement. 4. Duration and Termination: The agreement should specify the start and end date, or alternatively, outline the conditions under which either party can terminate the agreement. 5. Confidentiality and Non-Disclosure: To protect sensitive client information, clauses related to confidentiality and non-disclosure should be included in the agreement. 6. Independent Contractor Status: It is crucial for the agreement to establish the auditor's status as a self-employed independent contractor, clarifying that they are responsible for their taxes, insurance, and any legal liabilities. 7. Dispute Resolution: In case of any disputes, a clause outlining the preferred method of dispute resolution, such as mediation or arbitration, should be included. It is essential for accounting firms and auditors in Rhode Island to carefully draft and review their agreement to ensure compliance with state regulations and to establish a mutually beneficial working relationship. Consulting with legal professionals experienced in employment and contract law is highly recommended when creating a Rhode Island Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor.Rhode Island Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is a legal document that establishes a professional relationship between an accounting firm and an auditor, who will work as a self-employed independent contractor. This agreement outlines the specific terms and conditions under which the auditor will provide their services to the accounting firm. In Rhode Island, there are various types of agreements that accounting firms can use to employ auditors as self-employed independent contractors. Some common variations include: 1. Full-time Auditor Agreement: This type of agreement is used when an accounting firm hires an auditor on a full-time basis to work exclusively for their firm. It details the responsibilities, compensation, and work schedule of the auditor. 2. Part-time Auditor Agreement: When an accounting firm requires an auditor to work on a part-time basis, this type of agreement is utilized. It outlines the hours and days the auditor will work, along with their compensation and scope of responsibilities. 3. Project-Based Auditor Agreement: In situations where an accounting firm needs an auditor for a specific project or engagement, this agreement is employed. It specifies the scope of work, duration of the project, deliverables, and compensation structure. 4. Remote Auditor Agreement: Accounting firms might engage auditors who are not located within their office premises. This type of agreement covers the terms for auditors working remotely, including communication channels, reporting requirements, and compensation arrangements. Regardless of the specific type of agreement, certain key elements should be covered within the Rhode Island Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: 1. Identification of Parties: The agreement should clearly identify both the accounting firm and the auditor, including their legal names and addresses. 2. Services to be Provided: It is important to outline the specific services the auditor will be responsible for providing. This can include financial statement audits, internal control reviews, tax preparation, or any other accounting related tasks. 3. Payment Terms: The compensation structure, payment frequency, and any additional expenses to be reimbursed should be clearly defined in the agreement. 4. Duration and Termination: The agreement should specify the start and end date, or alternatively, outline the conditions under which either party can terminate the agreement. 5. Confidentiality and Non-Disclosure: To protect sensitive client information, clauses related to confidentiality and non-disclosure should be included in the agreement. 6. Independent Contractor Status: It is crucial for the agreement to establish the auditor's status as a self-employed independent contractor, clarifying that they are responsible for their taxes, insurance, and any legal liabilities. 7. Dispute Resolution: In case of any disputes, a clause outlining the preferred method of dispute resolution, such as mediation or arbitration, should be included. It is essential for accounting firms and auditors in Rhode Island to carefully draft and review their agreement to ensure compliance with state regulations and to establish a mutually beneficial working relationship. Consulting with legal professionals experienced in employment and contract law is highly recommended when creating a Rhode Island Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor.