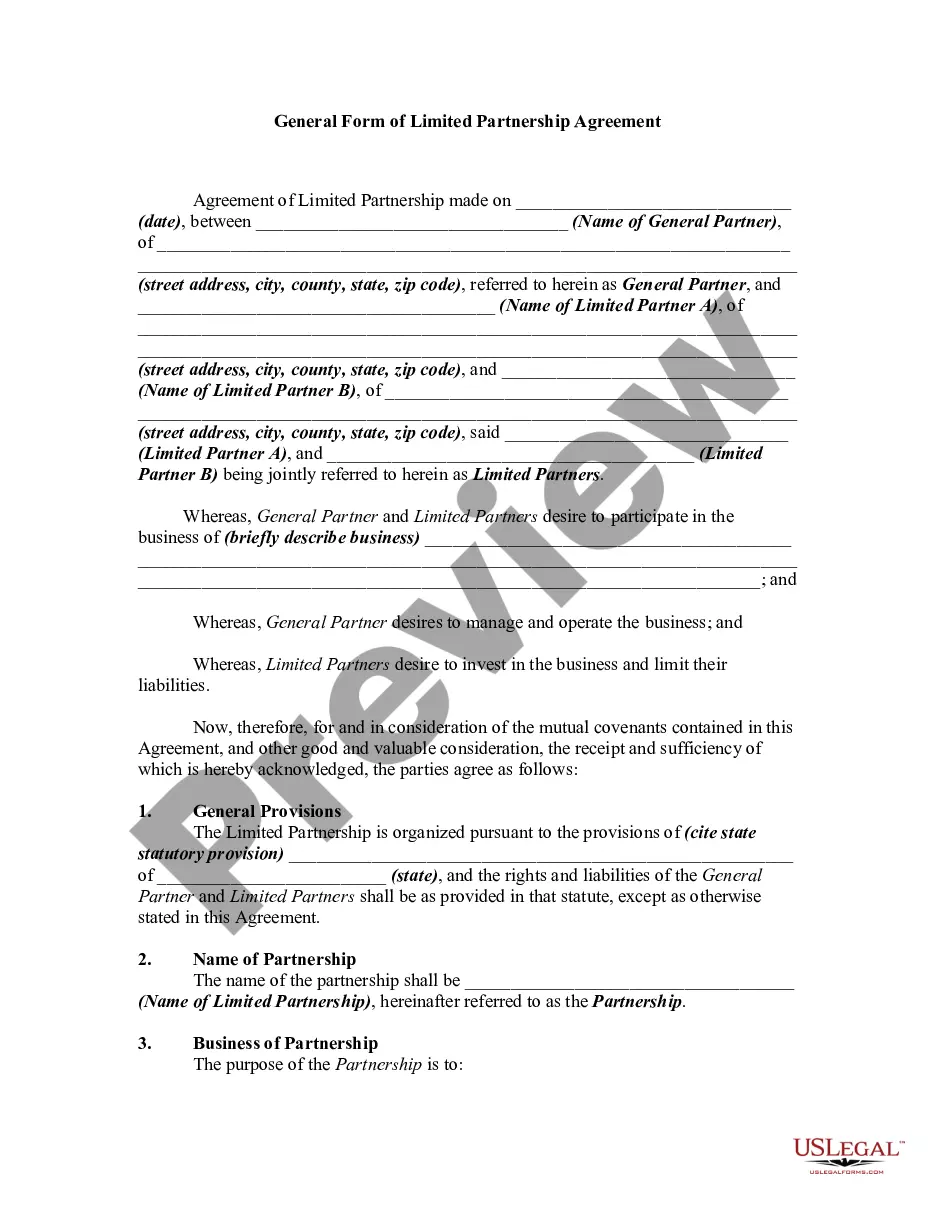

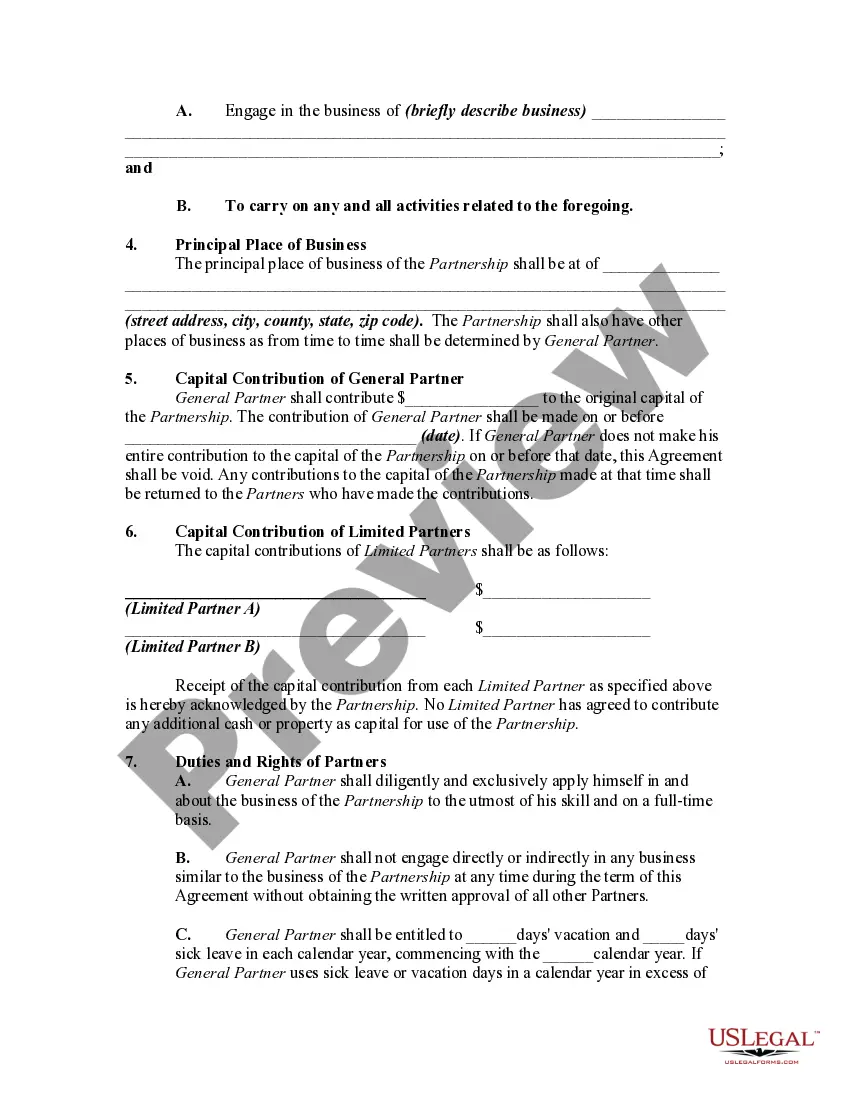

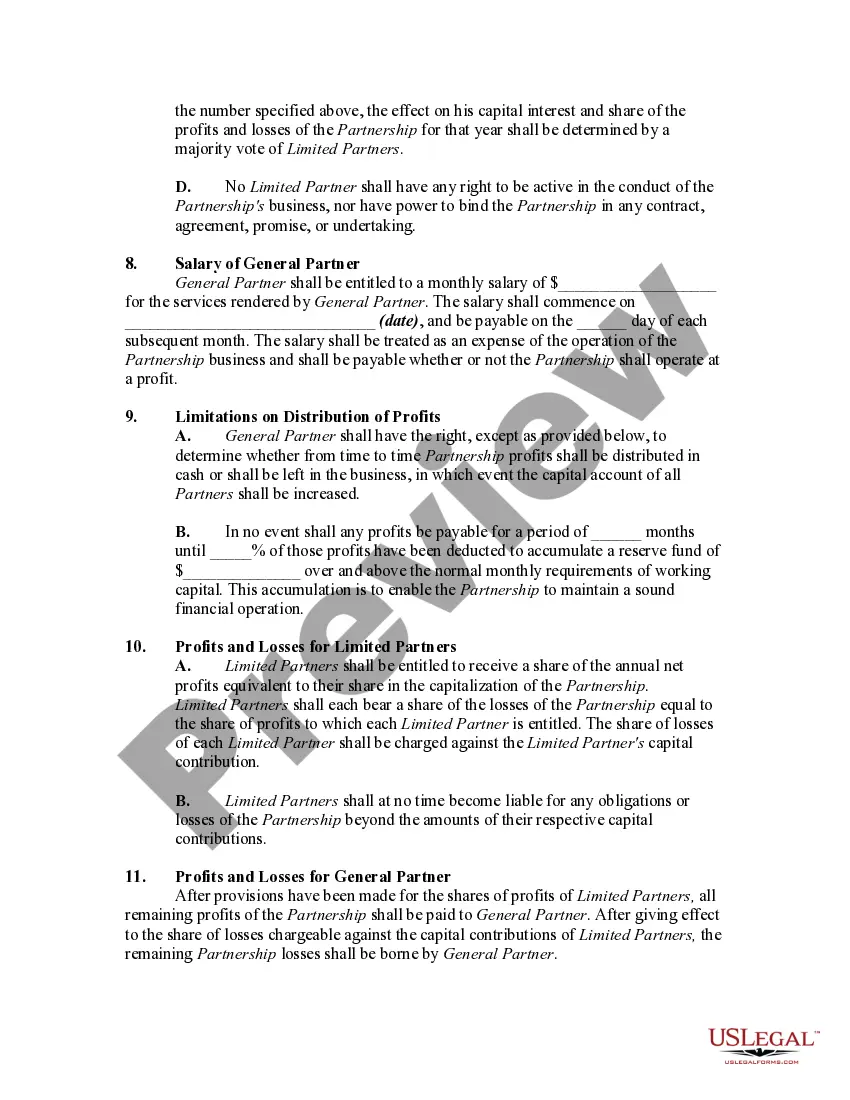

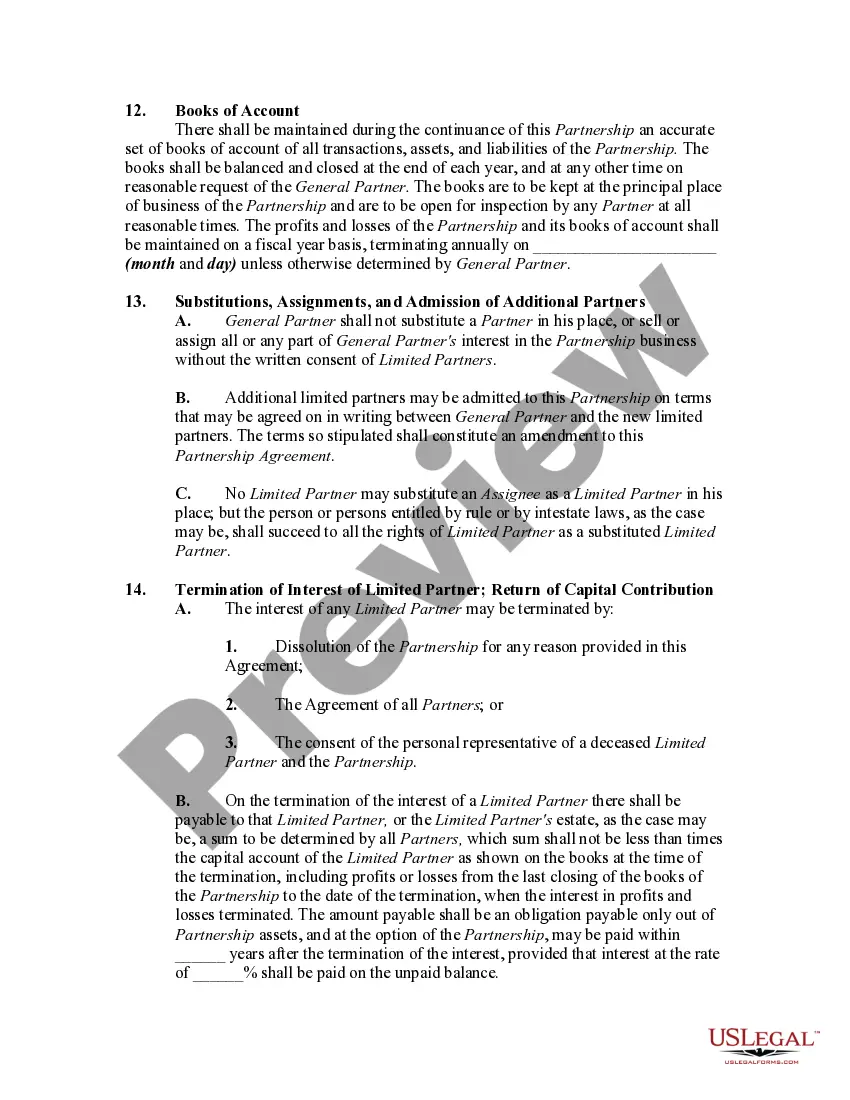

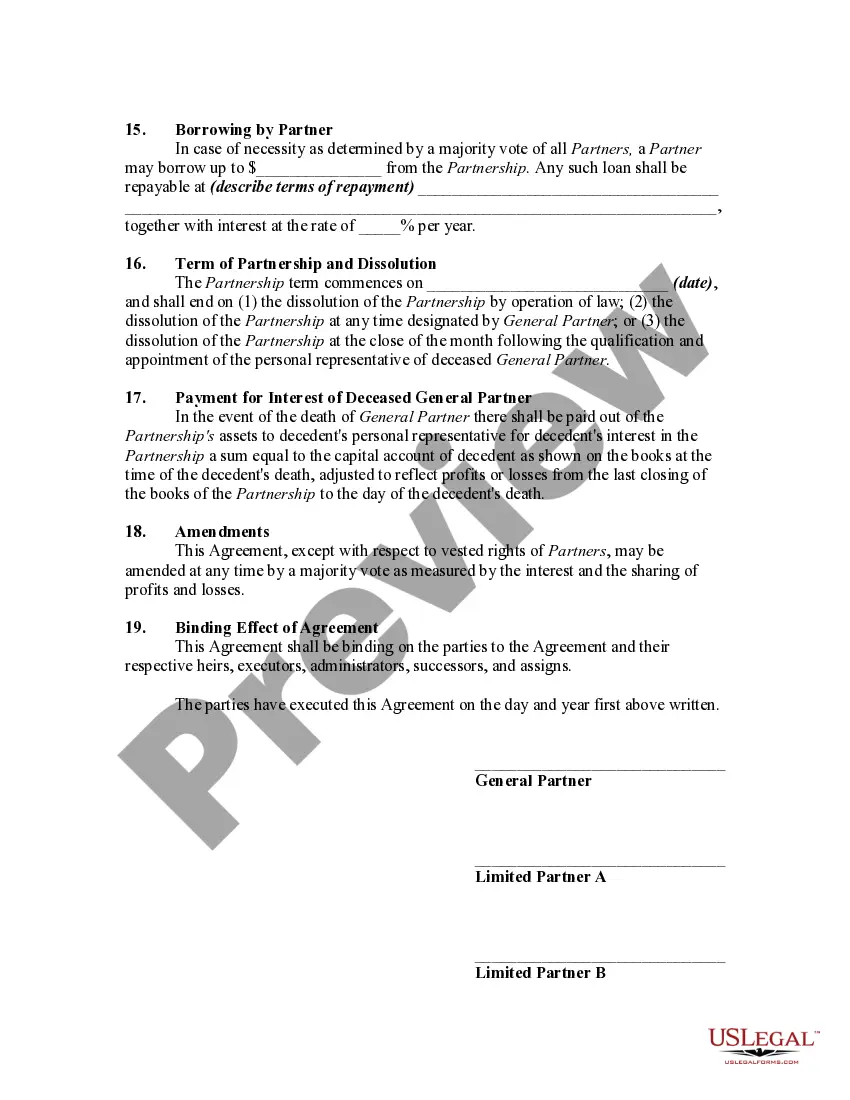

A limited partnership is a modified partnership and is a creature of State statutes. Most States have either adopted the Uniform Limited Partnership Act (ULPA) or the Revised Uniform Limited Partnership Act (RULPA). In a limited partnership, certain members contribute capital, but do not have liability for the debts of the partnership beyond the amount of their investment. These members are known as limited partners. The partners who manage the business and who are personally liable for the debts of the business are the general partners. A limited partnership can have one or more general partners and one or more limited partners.

The general partners manage the business of the partnership and are personally liable for its debts. Limited partners have the right to share in the profits of the business and, if the partnership is dissolved, will be entitled to a percentage of the assets of the partnership. A limited partner may lose his limited liability status if he participates in the control of the business.

Rhode Island General Form of Limited Partnership Agreement is a legal document that outlines the terms and conditions governing the partnership relationship between a general partner(s) and limited partner(s) in the state of Rhode Island. This agreement provides a framework for the operation, management, and decision-making processes of a limited partnership. In Rhode Island, there are several types of General Form of Limited Partnership Agreements catered to different business needs and requirements: 1. Traditional General Partnership Agreement: This type of agreement follows the standard rules and regulations set forth by the Rhode Island Revised Uniform Partnership Act (IPA). It establishes the roles and responsibilities of general partners, who have unlimited liability and control over the partnership's day-to-day operations. 2. Limited Liability Partnership (LLP) Agreement: This agreement offers limited liability protection to general partners, shielding them from personal liability for the partnership's debts and obligations. Laps are commonly chosen by professional service providers, such as law firms or accounting practices. 3. Family Limited Partnership (FLP) Agreement: Specifically designed for family-owned businesses, this agreement allows family members to collectively manage and own assets while providing limited liability protection. Alps are often utilized for estate planning, asset protection, and generational wealth transfer purposes. 4. Limited Partnership Agreement with a Certificate of Limited Partnership: This agreement involves filing a Certificate of Limited Partnership with the Rhode Island Secretary of State's office. It provides the partnership with legal recognition and allows limited partners to maintain limited liability status, by prohibiting their active involvement in the partnership's management. The Rhode Island General Form of Limited Partnership Agreement covers essential aspects such as the partnership's name and purpose, capital contributions from partners, profit and loss sharing, distribution of assets, decision-making authority, partner meetings, admission and withdrawal of partners, dispute resolution mechanisms, dissolution procedures, and any additional provisions agreed upon by the partners. It is crucial for partners entering into a Rhode Island General Form of Limited Partnership Agreement to seek legal counsel to ensure compliance with the state's regulations and to tailor the agreement to their specific business needs. This will help protect the interests of all parties involved and ensure a smooth functioning of the partnership.Rhode Island General Form of Limited Partnership Agreement is a legal document that outlines the terms and conditions governing the partnership relationship between a general partner(s) and limited partner(s) in the state of Rhode Island. This agreement provides a framework for the operation, management, and decision-making processes of a limited partnership. In Rhode Island, there are several types of General Form of Limited Partnership Agreements catered to different business needs and requirements: 1. Traditional General Partnership Agreement: This type of agreement follows the standard rules and regulations set forth by the Rhode Island Revised Uniform Partnership Act (IPA). It establishes the roles and responsibilities of general partners, who have unlimited liability and control over the partnership's day-to-day operations. 2. Limited Liability Partnership (LLP) Agreement: This agreement offers limited liability protection to general partners, shielding them from personal liability for the partnership's debts and obligations. Laps are commonly chosen by professional service providers, such as law firms or accounting practices. 3. Family Limited Partnership (FLP) Agreement: Specifically designed for family-owned businesses, this agreement allows family members to collectively manage and own assets while providing limited liability protection. Alps are often utilized for estate planning, asset protection, and generational wealth transfer purposes. 4. Limited Partnership Agreement with a Certificate of Limited Partnership: This agreement involves filing a Certificate of Limited Partnership with the Rhode Island Secretary of State's office. It provides the partnership with legal recognition and allows limited partners to maintain limited liability status, by prohibiting their active involvement in the partnership's management. The Rhode Island General Form of Limited Partnership Agreement covers essential aspects such as the partnership's name and purpose, capital contributions from partners, profit and loss sharing, distribution of assets, decision-making authority, partner meetings, admission and withdrawal of partners, dispute resolution mechanisms, dissolution procedures, and any additional provisions agreed upon by the partners. It is crucial for partners entering into a Rhode Island General Form of Limited Partnership Agreement to seek legal counsel to ensure compliance with the state's regulations and to tailor the agreement to their specific business needs. This will help protect the interests of all parties involved and ensure a smooth functioning of the partnership.