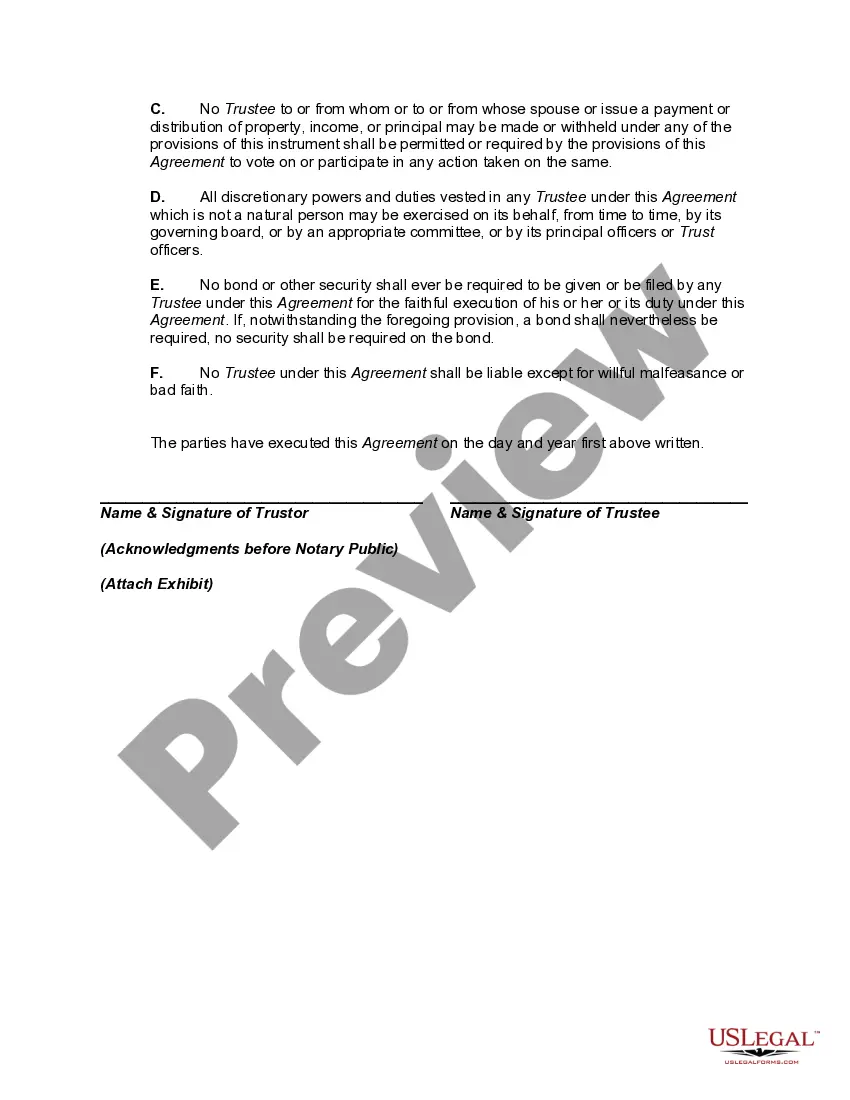

An irrevocable trust is an arrangement in which the grantor departs with ownership and control of property. Usually this involves a gift of the property to the trust. The trust then stands as a separate taxable entity and pays tax on its accumulated income.

A discretionary trust is a trust where the beneficiaries and/or their entitlements to the trust fund are not fixed, but are determined by the criteria set out in the trust instrument by trustor. Discretionary trusts can be discretionary in two respects. First, the trustees usually have the power to determine which beneficiaries (from within the class) will receive payments from the trust. Second, trustees can select the amount of trust property that the beneficiary receives. Although most discretionary trusts allow both types of discretion, either can be allowed on its own. It is permissible in most legal systems for a trust to have a fixed number of beneficiaries and for the trustees to have discretion as to how much each beneficiary receives.

A Rhode Island Irrevocable Trust Agreement for the Benefit of Trust or's Children with Discretionary Distributions of Income and Principal is a legal document that outlines the establishment and terms of a trust created by a trust or (the person creating the trust) for the benefit of their children. In this type of trust agreement, the trust or designates specific individuals or entities as trustees to manage the assets held within the trust on behalf of the children. The primary feature of this trust is the discretionary distributions of income and principal. This means that the trustees have the authority to determine when and how much income or principal should be distributed to the children. This discretion allows the trustees to make informed decisions based on the specific needs and circumstances of each beneficiary. It also provides flexibility, ensuring that the trust assets can be utilized effectively to support the children's education, health, maintenance, and other essential needs. It's important to note that there may be variations or alternative types of Rhode Island Irrevocable Trust Agreements for the Benefit of Trust or's Children with Discretionary Distributions of Income and Principal, tailored to specific situations or objectives. Some of these variations include: 1. Educational Trust: This type of trust agreement focuses primarily on using the trust assets for the educational needs of the beneficiaries. Trustees have the discretion to distribute income and principal to cover tuition fees, expenses related to education, or vocational training. 2. Special Needs Trust: Designed for beneficiaries with disabilities or unique circumstances, a special needs trust ensures that distributions from the trust do not disqualify the beneficiary from government assistance programs. Trustees carefully manage distributions to enhance the beneficiary's quality of life while preserving eligibility for support. 3. Spendthrift Trust: A spendthrift trust restricts the beneficiaries from accessing the principal or income of the trust for their own use or creditors until certain conditions are met, such as reaching a particular age or achieving specific goals. This structure protects the trust assets from potential financial mismanagement or external claims. 4. Family Trust: In a family trust, the trust or establishes the trust to benefit multiple generations of their family. While the primary beneficiaries are typically the trust or's children, the trust's duration can extend beyond their lifetimes, providing for grandchildren or future descendants. The trust may include provisions for discretionary distributions of income and principal to address various family members' financial needs. Rhode Island Irrevocable Trust Agreements for the Benefit of Trust or's Children with Discretionary Distributions of Income and Principal provide a versatile and effective vehicle for preserving and managing assets for the benefit of beneficiaries. These trusts ensure that the trustee has flexibility in making distributions while safeguarding the trust estate for long-term financial support and security.