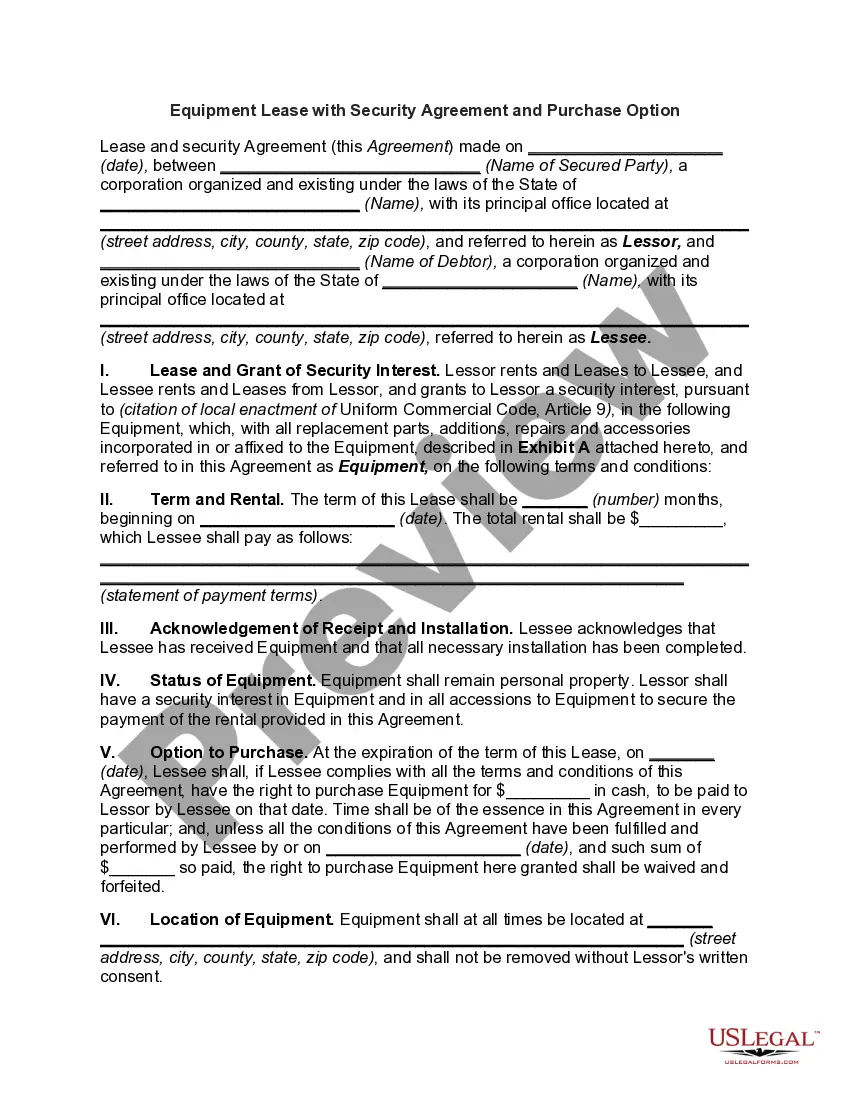

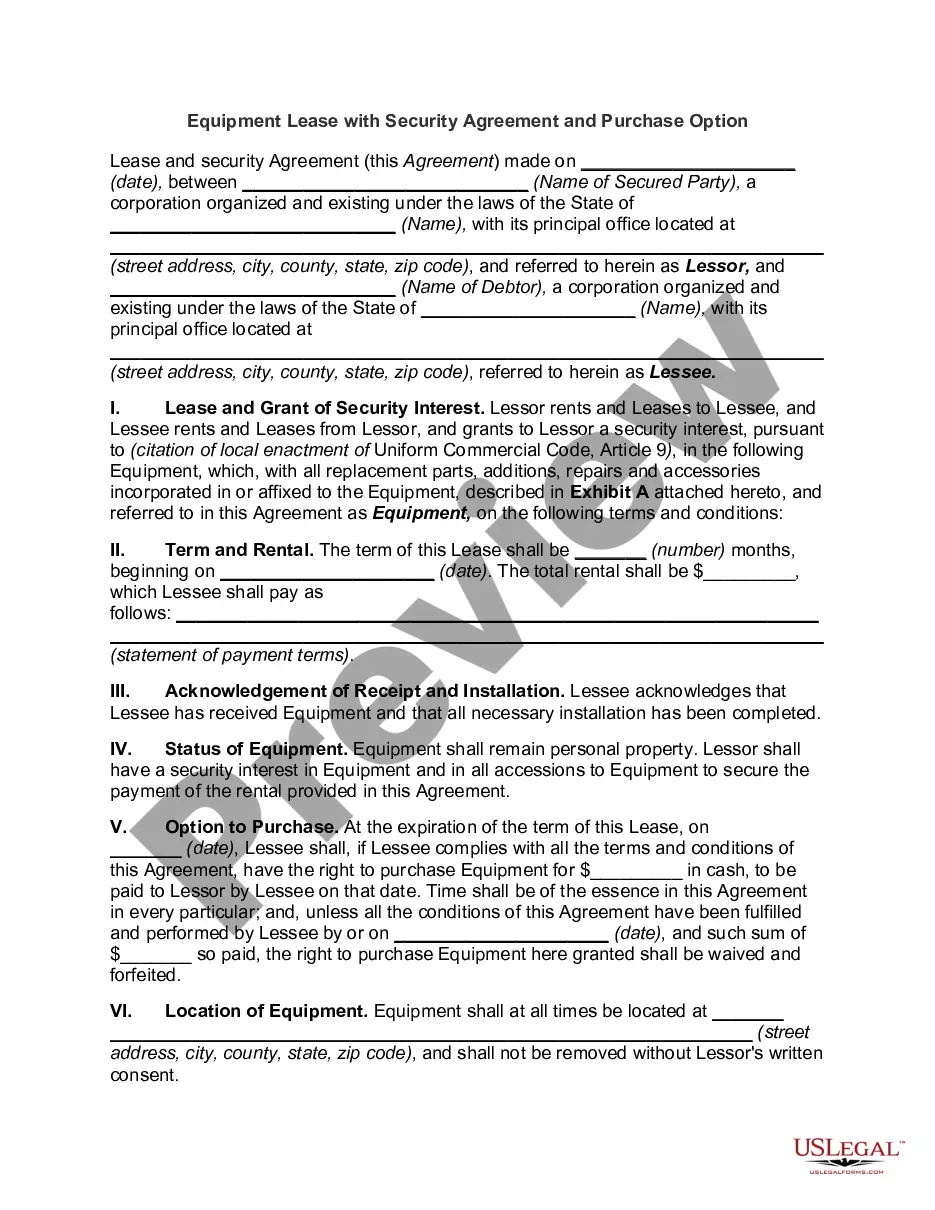

Rhode Island Lease Purchase Agreement for Equipment

Description

How to fill out Lease Purchase Agreement For Equipment?

In case you desire to finalize, retrieve, or produce valid document templates, utilize US Legal Forms, the largest selection of valid forms that is accessible online.

Take advantage of the website's straightforward and user-friendly search to acquire the paperwork you need.

A variety of templates for business and personal purposes are sorted by categories and states, or keywords.

Step 5. Complete the transaction. You may use your credit card or PayPal account to finish the purchase.

Step 6. Locate the format of the legal form and download it to your device.

- Use US Legal Forms to obtain the Rhode Island Lease Purchase Agreement for Equipment with just a few clicks.

- If you are already a US Legal Forms member, Log In to your account and click on the Download button to retrieve the Rhode Island Lease Purchase Agreement for Equipment.

- You can also access forms you have previously saved in the My documents section of your account.

- For first-time users of US Legal Forms, adhere to the following instructions.

- Step 1. Ensure you have selected the form pertaining to the correct region/country.

- Step 2. Utilize the Preview option to review the form's content. Be sure to read the description.

- Step 3. If you are dissatisfied with the form, use the Search section at the top of the page to discover other forms in the legal form database.

- Step 4. After locating the form you need, click the Purchase now button. Select the pricing plan you prefer and enter your details to register for an account.

Form popularity

FAQ

What is equipment leasing? Equipment leasing is a type of financing in which you rent equipment rather than purchase it outright. You can lease expensive equipment for your business, such as machinery, vehicles or computers.

The three most common types of leases are gross leases, net leases, and modified gross leases.The Gross Lease. The gross lease tends to favor the tenant.The Net Lease. The net lease, however, tends to favor the landlord.The Modified Gross Lease.

Various Types of Lease: Finance, Operating, Direct, LeveragedVarious Types of Lease.(1) Finance lease :(2) Operating lease :(3) Sale and lease back :(4) Direct lease :(5) Single investor lease :(6) Leveraged lease :(7) Domestic Lease :More items...

The three main types of leasing are finance leasing, operating leasing and contract hire.

Learn more about Equipment Leasing!Sale/Leaseback: (allows you to use your equipment to get working capital)True Lease or Operating Equipment Leases: (Also known as fair market value leases)The P.U.T. Option Lease (Purchase upon Termination)TRAC Equipment Leases.More items...

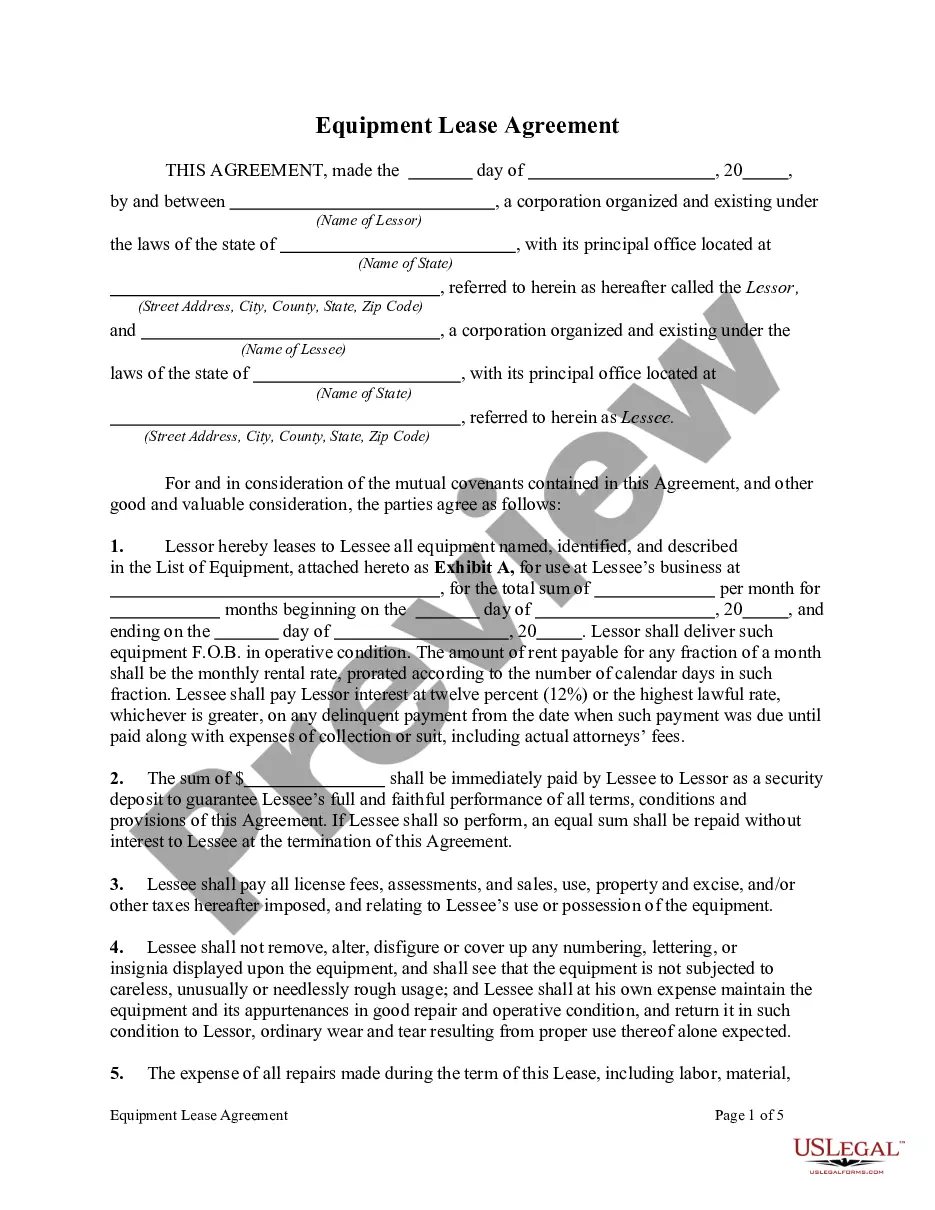

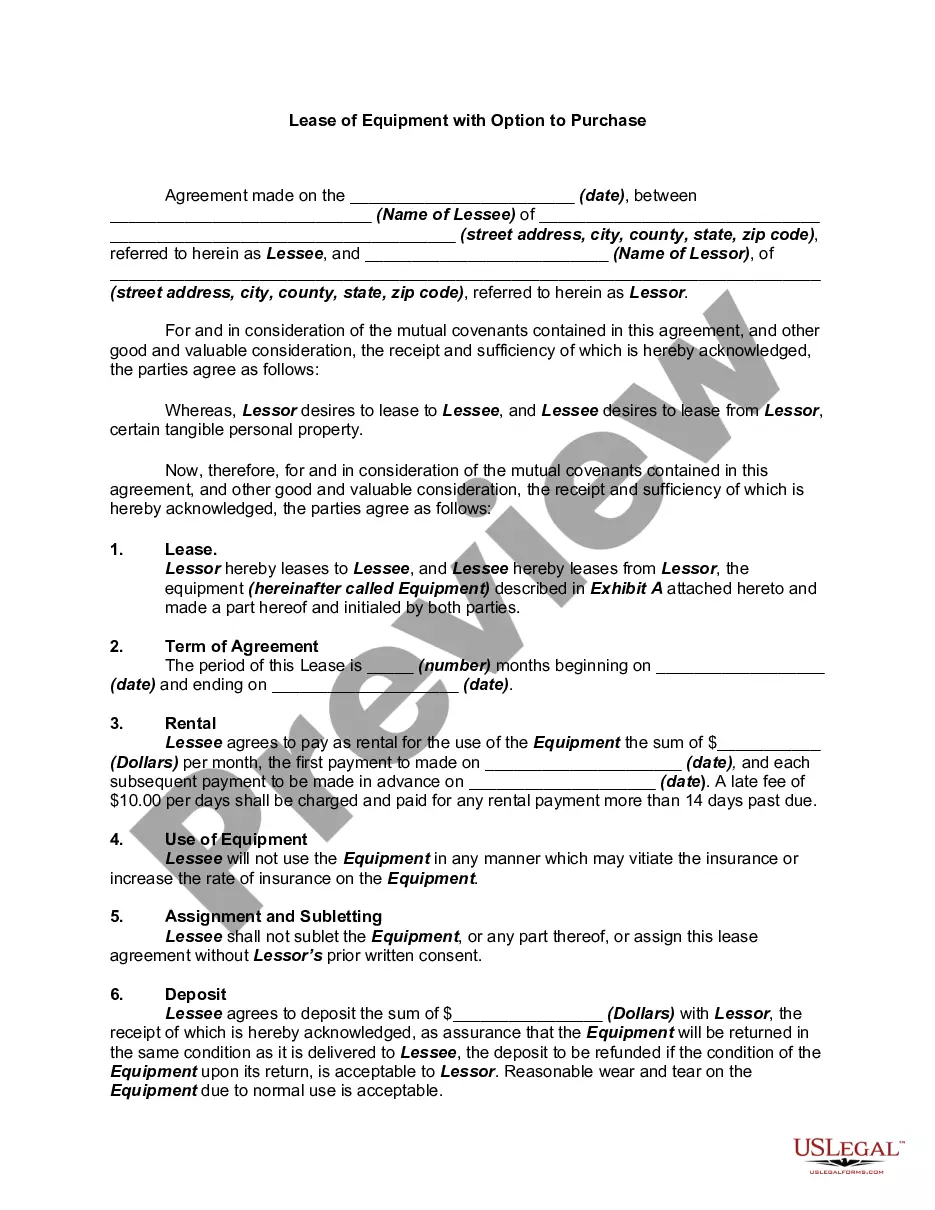

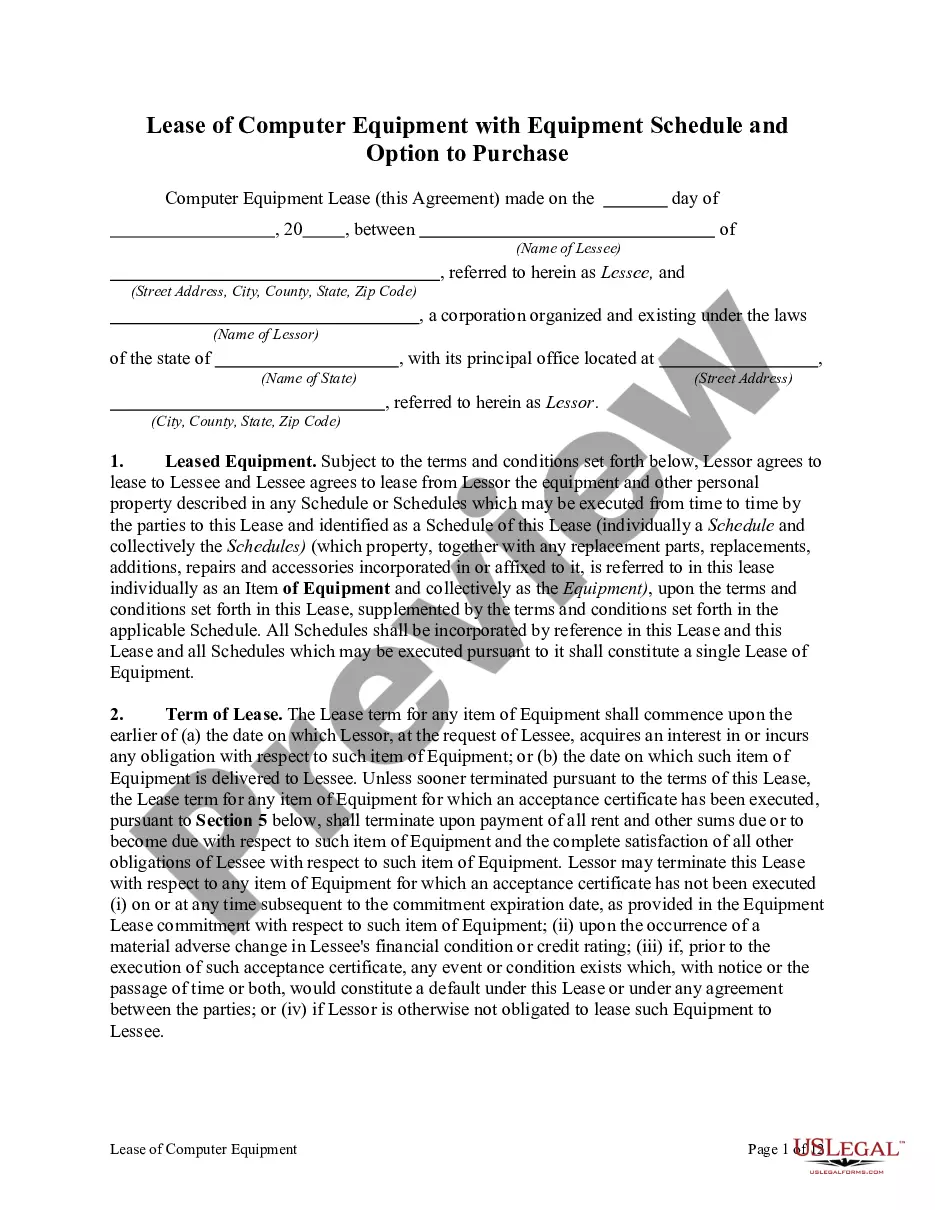

An equipment lease agreement is a contractual agreement where the lessor, who is the owner of the equipment, allows the lessee to use the equipment for a specified period in exchange for periodic payments. The subject of the lease may be vehicles, factory machines, or any other equipment.

What is equipment leasing? Equipment leasing is a type of financing in which you rent equipment rather than purchase it outright. You can lease expensive equipment for your business, such as machinery, vehicles or computers.

Also known as a lease agreement, the rent agreement is a written contract between the owner of a property (the landlord) and the tenant who takes it on rent.

Lessor's Agreement means that certain Lease Estoppel Certificate, Amendment of Lease and Agreement among Landlord, Borrower and Lender or any reliance letter or similar arrangement among Landlord, Borrower and Lender.

Definition. An equipment rental agreement (also known as an equipment rental form or an equipment rental contract) is a legally binding document that is used to rent equipment from one party to another for a fixed period of time.