Gift taxes are taxes that supplement the Estate Tax. Gift taxes are placed on gifts given away to any person while you are still living, so that you may not avoid estate taxes by making gifts of your estate. You may give up to $12,000 a year in cash or assets to an unlimited number of people each year without incurring gift tax liability, but the gifts must have no conditions attached. Married couples can give, as a couple, a $24,000 gift per year to as many people as they want. Under federal tax law, gifts totaling more than $12,000 to one person in one year are considered a taxable gift and generate a potential gift tax. It does not matter if you give one $13,000 gift or 13 gifts of $1,000 each, or one gift of $12,000 and a "birthday gift" of $1,000.

Gifts beyond the $12,000 limit (there is an exception for gifts that are directly paid by the gift giver for tuition and medical expenses) are considered "taxable gifts." Taxable gifts create liability for a gift tax. But gift tax is not due to be paid until you give away over $1,000,000 in your lifetime.

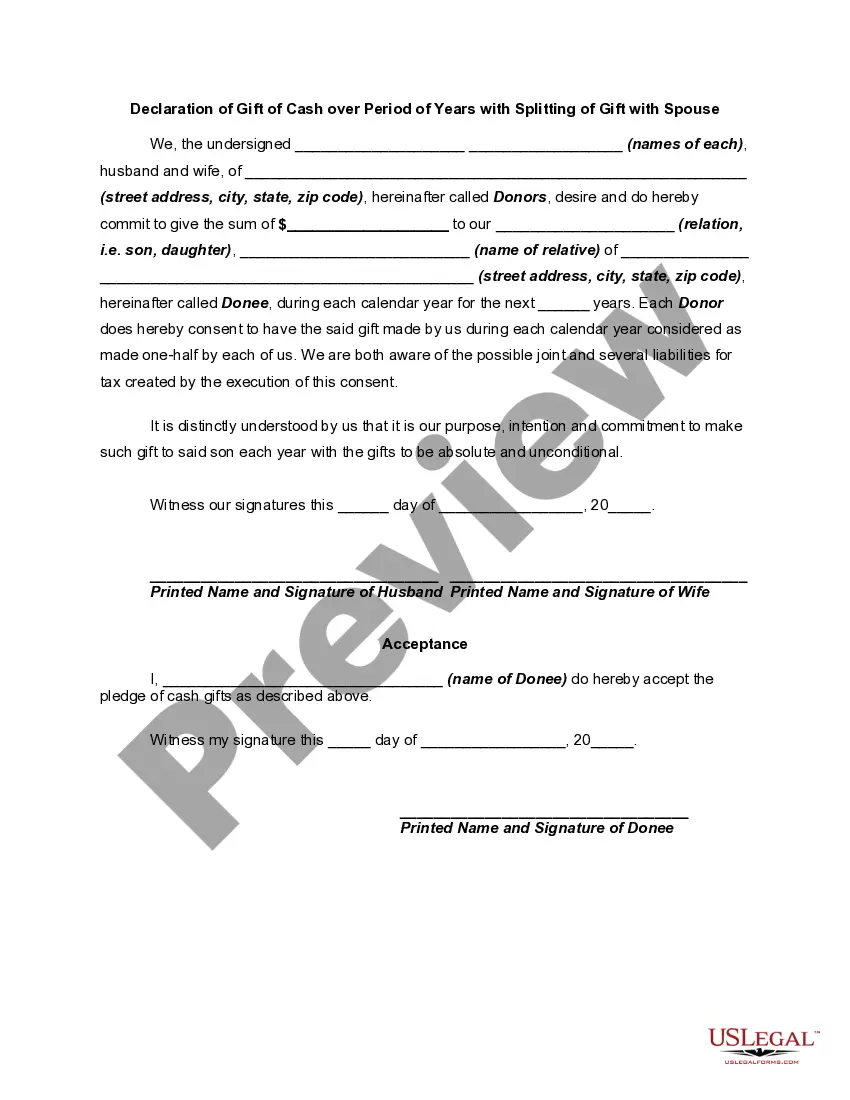

The Rhode Island Declaration of Gift of Cash over a Period of Years with Splitting of Gift with Spouse is a legal document that outlines the process of gifting cash to another individual or organization over a specified time period while also including provisions for splitting the gift with a spouse. This declaration is especially useful for individuals or couples who wish to make charitable donations or financial gifts while also taking advantage of potential tax benefits. By splitting the gift with a spouse, both individuals can maximize their tax deductions and ultimately reduce their overall tax liability. There are several types of Rhode Island Declaration of Gift of Cash over a Period of Years with Splitting of Gift with Spouse, including: 1. Charitable Gift Annuity: This type of declaration involves making a gift of cash to a qualified charitable organization while receiving regular fixed payments for the rest of the donor's life or a specified period. The remaining value of the gift goes to the charitable organization upon the donor's passing. 2. Charitable Remainder Trust: With this declaration, the donor transfers cash or other assets into a trust, receiving income from the trust for a set number of years or for their lifetime. Afterward, the remaining assets are distributed to the designated charitable organization. 3. Donor-Advised Fund: In this case, the donor contributes a cash gift to a mutual fund or sponsoring organization, which then manages the funds and provides recommendations upon the donor's request. The donor can make charitable recommendations over a period of years while still enjoying potential tax benefits. 4. Charitable Lead Trust: This type of declaration involves transferring cash or other assets into a trust that provides regular payments to a charitable organization for a specified time. Afterward, the remaining assets are typically passed on to the donor or their designated beneficiaries. These different types of declarations provide individuals with various options and structures for gifting cash over a period of years while splitting the gift with a spouse. It is crucial to consult with a qualified attorney or financial advisor to properly assess financial goals, tax implications, and available options when considering a Rhode Island Declaration of Gift of Cash over a Period of Years with Splitting of Gift with Spouse.The Rhode Island Declaration of Gift of Cash over a Period of Years with Splitting of Gift with Spouse is a legal document that outlines the process of gifting cash to another individual or organization over a specified time period while also including provisions for splitting the gift with a spouse. This declaration is especially useful for individuals or couples who wish to make charitable donations or financial gifts while also taking advantage of potential tax benefits. By splitting the gift with a spouse, both individuals can maximize their tax deductions and ultimately reduce their overall tax liability. There are several types of Rhode Island Declaration of Gift of Cash over a Period of Years with Splitting of Gift with Spouse, including: 1. Charitable Gift Annuity: This type of declaration involves making a gift of cash to a qualified charitable organization while receiving regular fixed payments for the rest of the donor's life or a specified period. The remaining value of the gift goes to the charitable organization upon the donor's passing. 2. Charitable Remainder Trust: With this declaration, the donor transfers cash or other assets into a trust, receiving income from the trust for a set number of years or for their lifetime. Afterward, the remaining assets are distributed to the designated charitable organization. 3. Donor-Advised Fund: In this case, the donor contributes a cash gift to a mutual fund or sponsoring organization, which then manages the funds and provides recommendations upon the donor's request. The donor can make charitable recommendations over a period of years while still enjoying potential tax benefits. 4. Charitable Lead Trust: This type of declaration involves transferring cash or other assets into a trust that provides regular payments to a charitable organization for a specified time. Afterward, the remaining assets are typically passed on to the donor or their designated beneficiaries. These different types of declarations provide individuals with various options and structures for gifting cash over a period of years while splitting the gift with a spouse. It is crucial to consult with a qualified attorney or financial advisor to properly assess financial goals, tax implications, and available options when considering a Rhode Island Declaration of Gift of Cash over a Period of Years with Splitting of Gift with Spouse.